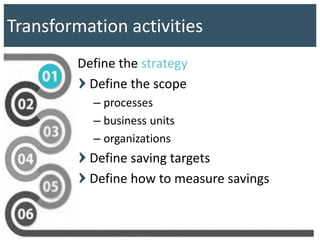

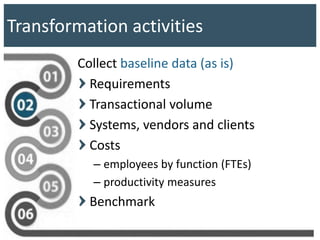

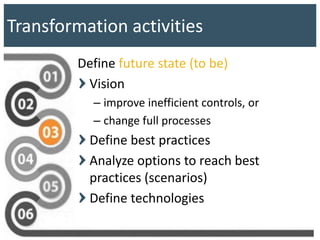

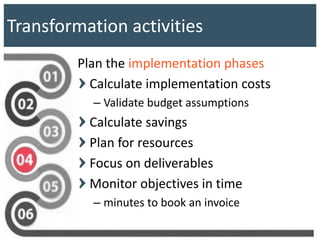

The document discusses strategies for finance transformation and lean accounting. It proposes reducing costs by standardizing processes, automating tasks, consolidating activities, and simplifying controls. This would allow the finance department to focus on analysis and advisory work. Specific recommendations include expediting financial reporting, simplifying accounts payable/receivable, centralizing bank accounts, and digitalizing documents to reduce errors. Transformation requires defining a strategy, collecting baseline data, planning implementation in phases, and reviewing results.

![[Webinar] From Tactical to Strategic: A Shift in the Understanding of Account...](https://cdn.slidesharecdn.com/ss_thumbnails/fromtacticaltostrategic-ashiftintheunderstandingofaccountspayable-131120124048-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)