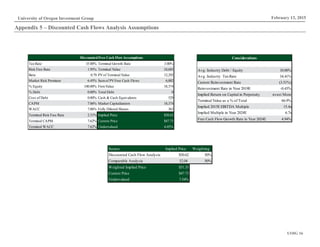

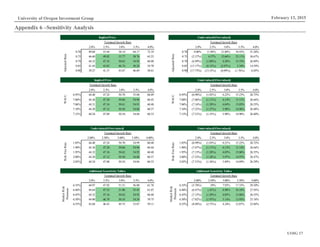

This document analyzes Paychex, Inc. as an investment opportunity. It finds that increasing US economic growth and small business growth will drive Paychex's revenue growth from its payroll and HR outsourcing services. Paychex is also developing new products that capitalize on growing demand for outsourcing. The analyst recommends Paychex as an "outperform" investment and sets a price target above the current stock price due to Paychex's superior products and competitors facing difficulties.