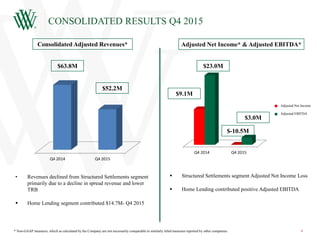

This document summarizes a fourth quarter and full year 2015 earnings call held by the company on March 8, 2016. It discusses key highlights from Q4 2015 including total receivable balances purchased, closed mortgage loans, adjusted EBITDA, and adjusted net loss. It also outlines cost savings initiatives for full year 2016 totaling $25-30 million from marketing efficiencies, personnel reductions, G&A spending reductions, and financing cost reductions. The document discusses early signs of improvement in the structured settlement payments business and priorities for 2016 including stabilizing that business, growing the home lending business, maintaining adequate liquidity, and improving the company's cash, capital, and funding positions.