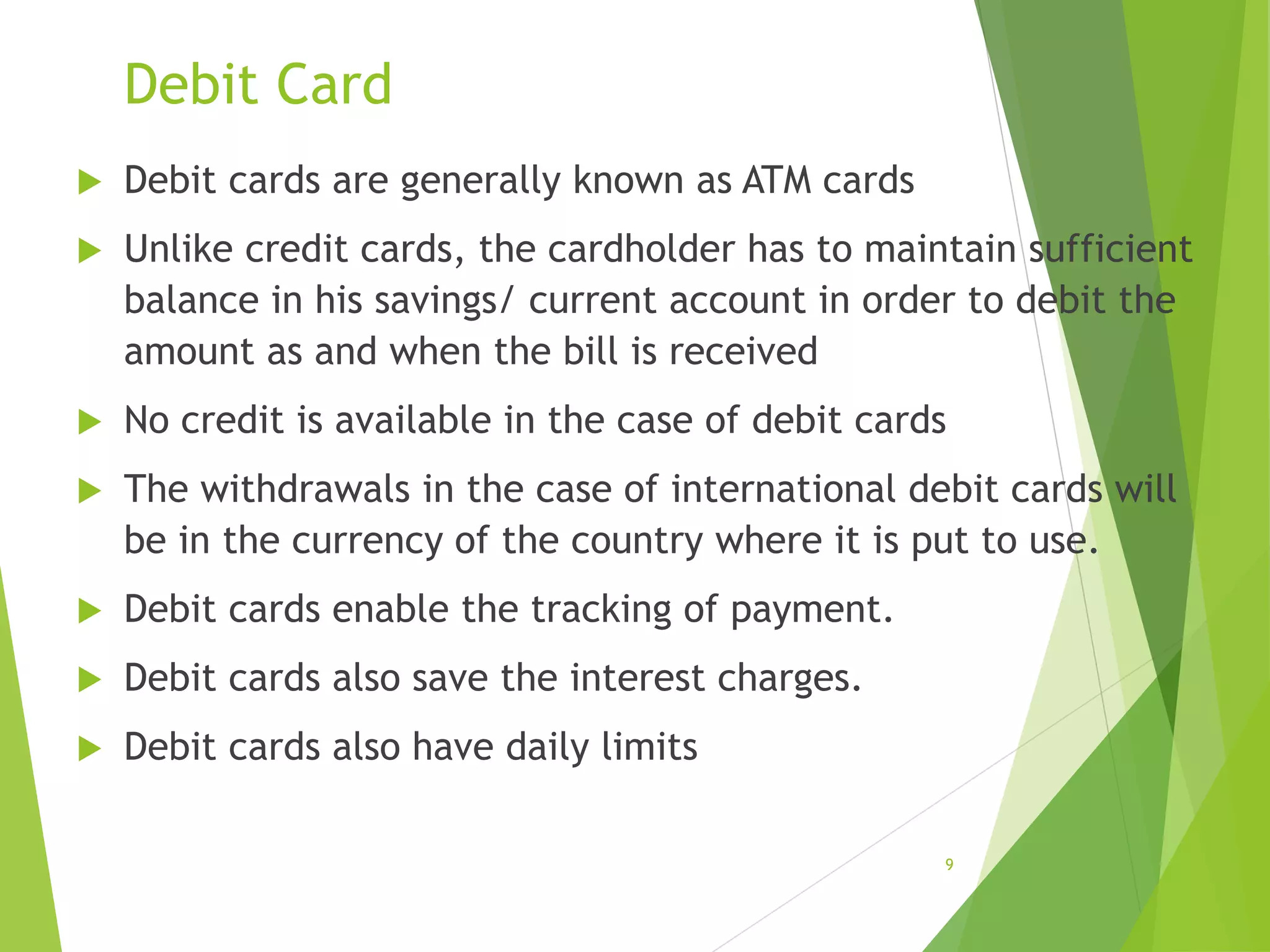

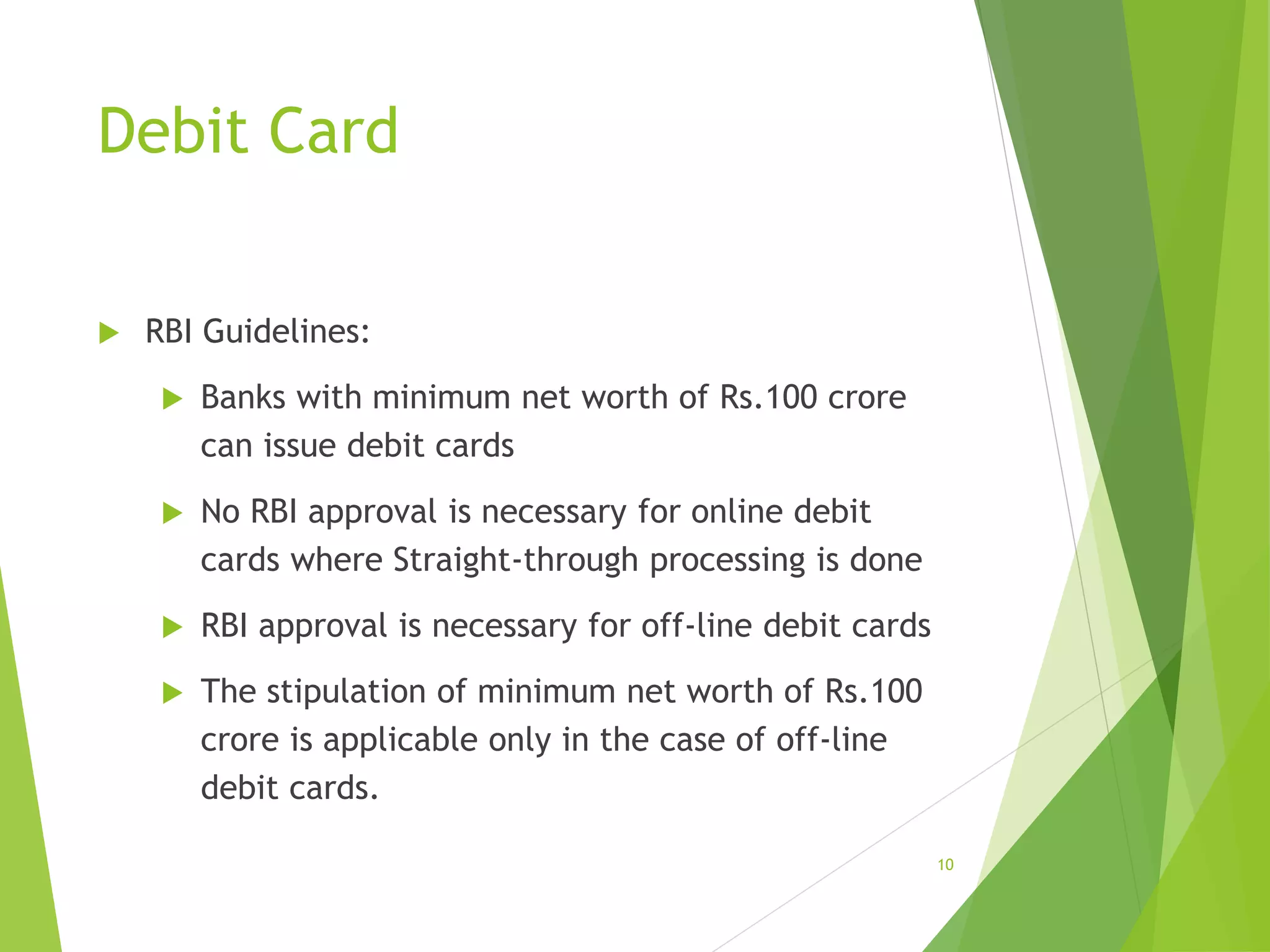

Fee-based retail financial services allow banks to derive income from fees rather than interest. They include services like tax counseling, credit/debit cards, ATMs, remittances, safe deposit lockers, and portfolio management. Banks facilitate these services and charge fees rather than providing loans and earning interest. Credit cards can be used to pay for goods, obtain cash, and access revolving credit. Debit cards directly debit funds from the linked bank account. ATMs provide convenient access to bank accounts anywhere. Safe deposit lockers and safe custody facilities securely store valuables for customers.