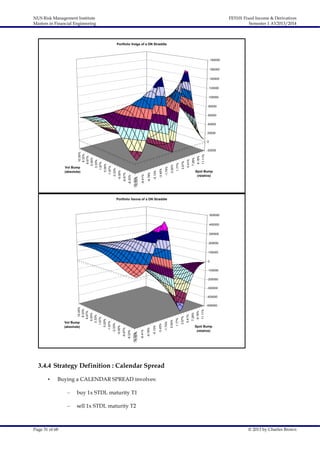

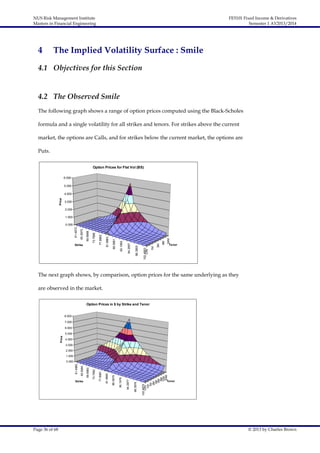

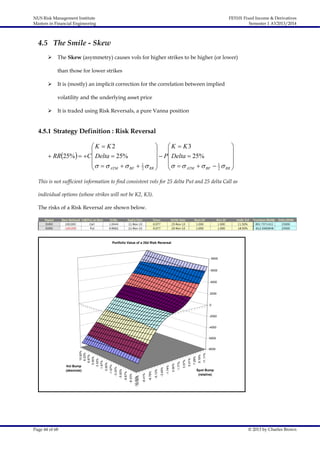

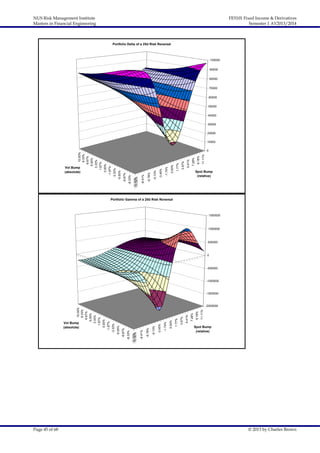

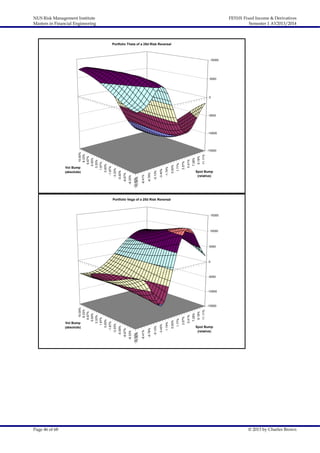

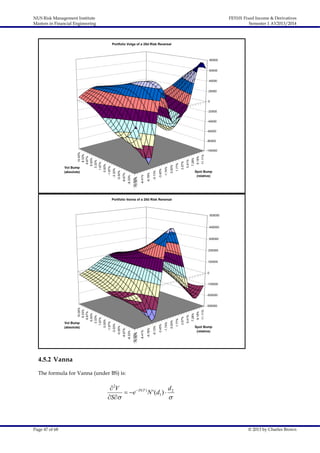

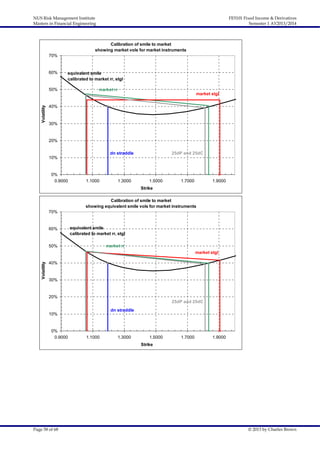

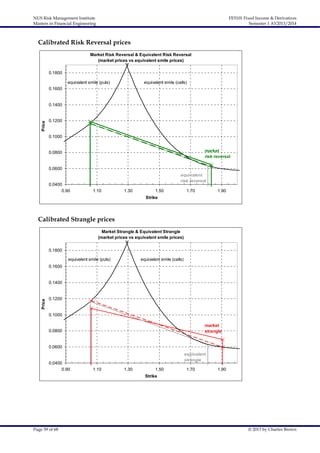

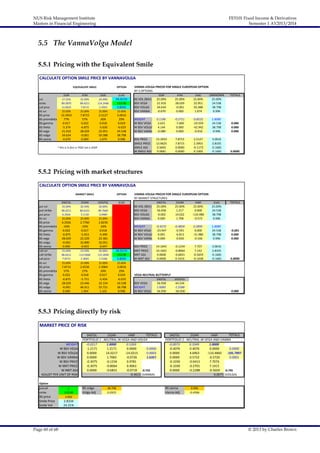

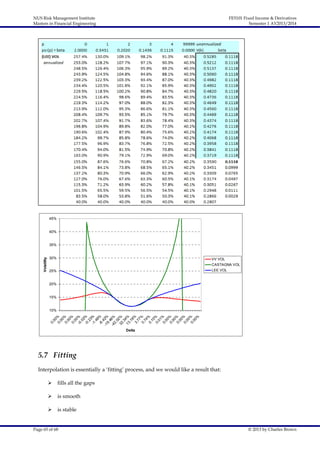

This document is a course outline for a Master's in Financial Engineering program, specifically focusing on fixed income and derivatives. It includes detailed sections on estimating volatility, implied volatility surfaces, and various models used in financial calculations such as GARCH. Additionally, it covers the course structure, reading materials, and expectations for students.