Recommended

Recommended

More Related Content

Similar to Exercises1. Classification of activitiesClassify each of the.docx

Similar to Exercises1. Classification of activitiesClassify each of the.docx (17)

More from SANSKAR20

More from SANSKAR20 (20)

Recently uploaded

Recently uploaded (20)

Exercises1. Classification of activitiesClassify each of the.docx

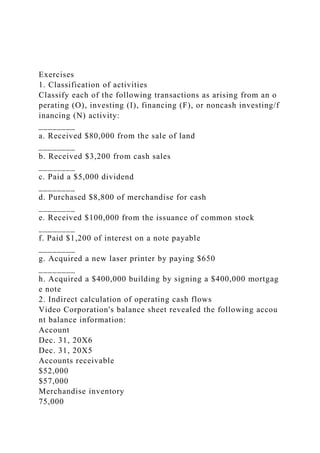

- 1. Exercises 1. Classification of activities Classify each of the following transactions as arising from an o perating (O), investing (I), financing (F), or noncash investing/f inancing (N) activity: ________ a. Received $80,000 from the sale of land ________ b. Received $3,200 from cash sales ________ c. Paid a $5,000 dividend ________ d. Purchased $8,800 of merchandise for cash ________ e. Received $100,000 from the issuance of common stock ________ f. Paid $1,200 of interest on a note payable ________ g. Acquired a new laser printer by paying $650 ________ h. Acquired a $400,000 building by signing a $400,000 mortgag e note 2. Indirect calculation of operating cash flows Video Corporation's balance sheet revealed the following accou nt balance information: Account Dec. 31, 20X6 Dec. 31, 20X5 Accounts receivable $52,000 $57,000 Merchandise inventory 75,000

- 2. 68,000 Accounts payable 21,000 19,500 The accrual- basis net income was $107,000. In computing net income, the co mpany recorded $12,600 of depreciation expense; there were no gains or losses from investing and financing activities. On the basis of the preceding information, calculate Video's cas h flows from operating activities by using the indirect method. 3. Indirect calculation of operating cash flows Specialty Services Inc. reported a net income of $110,000 for th e year just ended, which includes an $18,000 gain on the sale of long- term investments. The following data were obtained from compa rative balance sheets: Oct. 31, 20X2 Oct. 31, 20X1 Trade accounts receivable $245,000 $203,000 Merchandise inventory 230,000 308,000 Accumulated depreciation: equipment 120,000 65,000 Accounts payable 190,000 124,000 Accrued liabilities 38,000 73,000 There were no purchases or disposals of equipment during the y ear. The long-

- 3. term investment had a carrying (book) value of $77,000 and was sold for cash on June 15. On the basis of the preceding information, determine the cash pr ovided by operating activities from November 1, 20X1 through October 31, 20X2. The firm uses the indirect method of stateme nt preparation. 4. Overview of direct and indirect methods Evaluate the comments that follow as being true or false. If the comment is false, briefly explain why. a. Both the direct method and the indirect method will produce the same cash flow from operating activities. b. Depreciation expense is added back to net income when the indi rect method is used. c. One of the advantages of using the direct method rather than the indirect method is that larger cash flows from financing activiti es will be reported. d. The cash paid to suppliers is normally disclosed on the statemen t of cash flows when the indirect method of statement preparatio n is employed. e. The dollar change in the Merchandise Inventory account appears on the statement of cash flows only when the direct method of s tatement preparation is used. 5. Statement preparation: Direct method The comparative balance sheets of Village Company follow: VILLAGE COMPANY Comparative Balance Sheets December 31, 20X2 and 20X1 Dec. 31, 20X2 Dec. 31, 20X1 Cash

- 4. $ 5,000 $ 7,000 Accounts receivable (net) 12,000 18,000 Merchandise inventory 35,000 28,000 Property, plant, & equipment 40,000 30,000 Less: Accumulated depreciation (17,000) (10,000) Total assets $ 75,000 $ 73,000 Accounts payable* $ 25,000 $ 21,000 Income taxes payable 4,000 1,000 Common stock 24,000 24,000 Retained earnings 22,000 27,000 Total liabilities & stock, equity $ 75,000 $ 73,000 *Relate to purchases of merchandise The firm's accrual- basis income statement revealed the following data: sales, $120,

- 5. 000; cost of goods sold, $80,000; selling and administrative exp enses, $25,000; depreciation expense, $7,000; and income taxes, $3,000. (There was no interest expense.) Dividends declared an d paid during 20X2 totaled $10,000. Finally, Village purchased $10,000 of equipment for cash on August 14. a. Determine the increase or decrease in cash during 20X2. b. Prepare a statement of cash flows by using the direct method. 6. Equipment transaction and cash flow reporting The property, plant, and equipment section of ProComp Inc.'s c omparative balance sheet follows: Dec. 31, 20X4 Dec. 31, 20X3 Property, plant, & equipment Land $ 94,000 $ 94,000 Equipment 652,000 527,000 Less: Accumulated depreciation (316,000) (341,000) New equipment purchased during 20X4 totaled $280,000. The 2 0X4 income statement disclosed equipment depreciation expens e of $41,000 and a $9,000 loss on the sale of equipment. a. Determine the cost and accumulated depreciation of the equipm ent sold during 20X4. b. Determine the selling price of the equipment sold. c. Show how the sale of equipment would appear on a statement of cash flows prepared by using the indirect method. 7. Evaluation of cash flows The following statement of cash flows was prepared for Yellows tone Company:

- 6. YELLOWSTONE COMPANY Statement of Cash Flows for the Year Ended December 31, 20X2 Cash flows from operating activities Cash received from customers $240,000 Less cash payments for: Purchases of merchandise $180,000 Selling & administrative expenses 75,000 Interest 20,000 275,000 Net cash used by operating activities $ (35,000) Cash flows from investing activities Sale of equipment $ 20,000 Sale of vehicles 10,000 Sale of long-term investments 40,000 Net cash provided by investing act 70,000 Cash flows from financing activities Retirement of long-term debt

- 7. (50,000) Net increase (decrease) in cash $ (15,000) Cash balance, January 1, 20X2 54,000 Cash balance, December 31, 20X2 $ 39,000 Evaluate the nature of the decrease in cash. Does your analysis i ndicate any potential problems for Yellowstone? Problems 1. Transaction analysis: Operating, investing, and financing activit ies The management of Maui Corporation desires to know the natur e of each of the following transactions and events: 1. Collected cash from customers for cash sales. 2. Purchased a short-term investment for cash. 3. Secured a mortgage note to finance the acquisition of a building . 4. Issued 10-year bonds for cash. 5. Paid a short-term nonoperating note. 6. Sold equipment having a book value of $30,000 for $30,000 cas h. 7. Sold a parcel of land at cost; received a long-term note. 8. Received dividends on a long-term stock investment. 9. Paid income taxes. 10. Issued preferred stock in exchange for a valuable patent. 11. Reacquired treasury stock for cash. 12. Paid previously declared cash dividends. Instructions

- 8. a. Briefly explain the difference between investing and financing a ctivities and noncash investing/financing activities. a. Design a table with the following columnar headings: operating activity, investing activity, financing activity, and noncash inve sting/financing activity. Classify the 12 transactions listed by us ing these headings. For all classifications except noncash invest ing/financing, indicate whether the transaction causes a cash inf low (+) or a cash outflow (−). 1. Operating activities: Direct and indirect methods The 20X5 income statement of Office Products Inc. follows: OFFICE PRODUCTS INC. Income Statement for the Year Ended December 31, 20X5 Net sales $980,000 Cost of goods sold Beginning inventory $235,000 Net purchases 720,000 Goods available for sale $955,000 Less: Ending inventory 260,000 Cost of goods sold 695,000 Gross profit

- 9. $285,000 Expenses Selling & administrative $149,000 Depreciation 54,000 203,000 $ 82,000 Other revenue (expense) Interest expense $ (18,000) Gain on sale of equipment 26,000 8,000 Income before income taxes $ 90,000 Income taxes 27,000 Net income $ 63,000 1. The following additional information was obtained from the gen eral ledger and management personnel: 3. Accounts payable related to the purchases of merchandise decre ased during 20X5 by $32,800. In contrast, accounts receivable i ncreased by $23,700. 3. Prepaid expenses and wages payable increased throughout 20X5

- 10. by $2,400 and $5,600, respectively. 3. The balance in the income taxes payable account on January 1 w as $4,900; the December 31 balance was $4,100. 3. The company financed a $78,000 equipment purchase by signing a note payable that is due in 20X8. Instructions c. Prepare the operating activities section of the statement of cash flows by using the direct method. c. Prepare the operating activities section of the statement of cash flows by using the indirect method. 1. Cash flow information: Direct and indirect methods The comparative year- end balance sheets of Sign Graphics Inc. revealed the following activity in the company's current accounts: 20X5 20X4 Increase (decrease) Current assets Cash $ 55,400 $ 35,200 $ 20,200 Accounts receivable (net) 83,800 88,000 (4,200) Inventory 243,400 233,800 9,600

- 11. Prepaid expenses 25,400 24,200 1,200 Current liabilities Accounts payable $ 123,600 $140,600 $(17,000) Taxes payable 43,600 49,200 (5,600) Interest payable 9,000 6,400 2,600 Accrued liabilities 38,800 60,400 (21,600) Note payable 44,000 — 44,000 1. The accounts payable were for the purchase of merchandise. Pre paid expenses and accrued liabilities relate to the firm's selling and administrative expenses. The company's condensed income statement follows: SIGN GRAPHICS INC. Income Statement for the Year Ended December 31, 20X5 Sales $713,800

- 12. Less: Cost of goods sold 323,000 Gross profit $390,800 Less: Selling & administrative expenses $186,000 Depreciation expense 17,000 Interest expense 27,000 230,000 Add: Gain on sale of land $160,800 21,800 Income before taxes $182,600 Income taxes 36,800 Net income $145,800 1. Other data: 6. Long- term investments were purchased for cash at a cost of $74,600. 6. Cash proceeds from the sale of land totaled $76,200. 6. Store equipment of $44,000 was purchased by signing a short-

- 13. term note payable. Also, a $150,000 telecommunications system was acquired by issuing 3,000 shares of preferred stock. 6. A long-term note of $49,400 was repaid. 6. Twenty thousand shares of common stock were issued at $5.19 per share. 6. The company paid cash dividends amounting to $128,600. Instructions f. Prepare the operating activities section of the company's statem ent of cash flows, assuming use of 1) the direct method. 2) the indirect method. f. Prepare the investing and financing activities sections of the sta tement of cash flows. Student Guidance ReportAshford University ACC206Guidance ReportWeek OneLISTEN TO AUDIO/VIDEO EXPLAINING THE GUIDANCE REPORTYELLOW INDICATES ACCOUNT AMOUNTS CHANGEDChange Account to:Based Upon Course Start DateExercise/ ProblemAccount to be changedOriginal AmountJan-FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 1 Ex 2Net income107000$ 109,000$ 111,000$ 113,000$ 115,000$ 120,000$ 121,000Depreciation12600$ 13,000$ 15,000$ 16,000$ 18,000$ 20,000$ 21,000Accounts payable 21000$ 22,000$ 23,000$ 24,000$ 25,000$ 26,000$ 27,000QuestionsYOUR ANSWERS BASED UPON COURSE START DATENet IncomeAccounts receivableInventoryAccounts payableDepreciationCash Flow from Operating ActivitiesAccount to be changedOriginal AmountJan-FebMar-AprMay-JunJul-AugSept-OctNov-DecCh 1

- 14. Ex 3Net Income110000$ 112,000$ 114,000$ 116,000$ 117,000$ 118,000$ 120,000Trade accounts receivable 245000$ 246,000$ 248,000$ 249,000$ 250,000$ 255,000$ 256,000Merchandise inventory 230000$ 231,000$ 232,000$ 232,000$ 235,000$ 240,000$ 241,000Accumulated depreciation: equipment 120000$ 121,000$ 122,000$ 124,000$ 125,000$ 130,000$ 141,000Accounts payable 190000$ 191,000$ 193,000$ 194,000$ 195,000$ 200,000$ 201,000Accrued liabilities 38000$ 39,000$ 40,000$ 41,000$ 45,000$ 45,000$ 46,000Gain on sale of investments18000$ 18,000$ 18,000$ 18,000$ 18,000$ 18,000$ 18,000YOUR ANSWERS BASED UPON COURSE START DATENet Income Trade accounts receivable Merchandise inventory Accumulated depreciation: equipment Accounts payable Accrued liabilities Gain on sale of investmentsCash Flow from Operating ActivitiesCh 1 Ex 6Account to be changedOriginal AmountJan-FebMar-AprMay-JunJul-AugSept-OctNov-DecDec. 31, 20X4 New equipment purchased280000$ 290,000$ 295,000$ 296,000$ 297,000$ 298,000$ 299,000Depreciation expense41000$ 42,000$ 43,000$ 44,000$ 45,000$ 46,000$ 47,000YOUR ANSWERS BASED UPON COURSE START DATECost of equipment soldAccumulated depreciation of sold equipmentSelling price of equipment soldSale of equipment on cash flow statementCh 1 Pb 2Account to be changedOriginal AmountJan-FebMar-AprMay-JunJul-AugSept-OctNov- DecAccounts payable decreased32800$ 33,800$ 34,800$ 35,800$ 36,800$ 37,800$ 38,800Accounts receivable increased23700$ 24,275$ 24,850$ 25,425$ 26,000$ 26,575$ 27,150Prepaid expenses increased2400$ 2,975$ 3,550$ 4,125$ 4,700$ 5,275$ 5,850wages payable increased5600$ 6,175$ 6,750$ 7,325$ 7,900$ 8,475$ 9,050Income taxes payable decreased800$ 1,375$ 1,950$

- 15. 2,525$ 3,100$ 3,675$ 4,250YOUR ANSWERS BASED UPON COURSE START DATEDirect MethodCash collectedLess cash paid for:Inventory Selling & administrative Interest expense Income taxes Net cash provided by operating activitiesIndirect MethodNet incomeAccounts payable decreasedAccounts receivable increasedPrepaid expenses increasedwages payable increasedInventoryIncome taxes payable decreased Depreciation Gain on sale of equipment Net cash provided by operating activitiesCH 1 Pb 3 Account to be changedOriginal AmountJan-FebMar-AprMay-JunJul-AugSept-OctNov- DecAccounts receivable (net) 83800$ 84,800$ 85,800$ 86,800$ 87,800$ 88,800$ 89,800Inventory 243400$ 244,400$ 245,400$ 246,400$ 247,400$ 248,400$ 249,400Accounts payable 123600$ 124,600$ 125,600$ 126,600$ 127,600$ 128,600$ 129,600Taxes payable 43600$ 44,600$ 45,600$ 46,600$ 47,600$ 43,600$ 43,600Sales 713800$ 718,000$ 723,000$ 728,000$ 733,000$ 738,000$ 748,000Net income 145800$ 150,000$ 155,000$ 160,000$ 165,000$ 170,000$ 180,000Long tem investments purchased74600$ 75,600$ 76,600$ 77,600$ 78,600$ 79,600$ 80,600Sale of land cash proceeds76200$ 77,200$ 78,200$ 79,200$ 80,200$ 81,200$ 82,200Store equipment purchased - short term note44000$ 45,000$ 46,000$ 47,000$ 48,000$ 49,000$ 50,000Purchased equipment issue 3000 pref shares150000$ 151,000$ 152,000$ 153,000$ 154,000$ 155,000$ 156,000Long term note repaid49400$ 49,900$ 50,400$ 50,900$ 51,400$ 51,900$ 52,400Common stock issued - shares20000205002100021500220002250023000YOUR ANSWERS BASED UPON COURSE START DATEPrepare the operating activities section of the statement of cash flows by using the direct method.Cash collectedLess cash paid for:Inventory Selling & administrative Interest expense Income taxes Net cash provided by operating activitiesPrepare

- 16. the operating activities section of the statement of cash flows by using the indirect method.Net incomeAccounts receivable InventoryPrepaid expenses Accounts payable Taxes payable Interest payable Accrued liabilities Gain on sale of landDepreciationNet cash provided by operating activitiesPrepare the investing and financing activities sections of the statement of cash flows.Cash flows from investing activitiesPurchase of long-term investmentsProceeds from sale of landNet cash provided by investing act.Cash flows from financing activitiesRepayment of long-term noteIssuance of common stock*Dividends paidNet cash used by financing activities* 20,000 shares X $5.19 = $103,800Note: The store equipment and telecommunications system transactions would be reported as noncash investing/ financing activities../../cpabi_000/Documents/ACC205%20Chapters/Produ ced%20videos/Guidance%20Report/Guidance%20Report.mp4