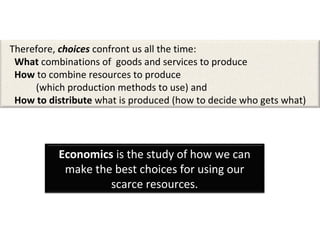

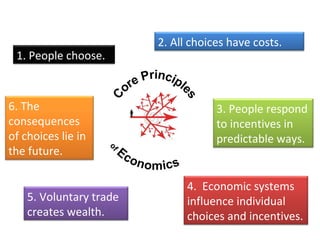

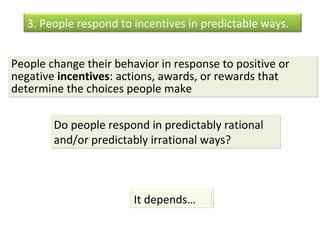

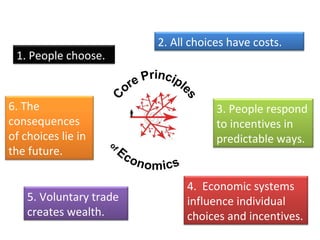

This document provides an overview of key concepts in economics. It discusses how economics is the study of choices given scarce resources and unlimited wants. It explains that individuals, businesses, and governments make choices to maximize well-being, profits, and societal welfare. It also outlines how all choices have costs, people respond to incentives, economic systems influence choices, voluntary trade creates wealth, and the consequences of choices lie in the future.

![People choose - continued

Businesses choose what and how much to

produce and sell in order to maximize profit

(revenue minus cost).

Governments choose what combinations of

goods and services (as determined by local,

state, and federal government budgets)

will maximize society’s well being

(as measured by Gross Domestic Product

[GDP], number of jobs, purchasing power,

happiness, …?)

Anyone – choose to behave in a

way that will increase the

world’s well being?](https://image.slidesharecdn.com/economics-140930134124-phpapp02/85/Economics-11-320.jpg)

![What Is Blockchain Technology A Simple Beginner’s Guide [2026]](https://cdn.slidesharecdn.com/ss_thumbnails/whatisblockchaintechnologyasimplebeginnersguide2026-260101112141-cf432b44-thumbnail.jpg?width=640&height=640&fit=bounds)