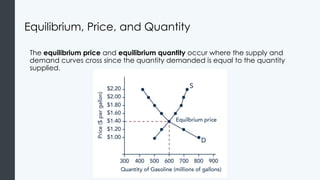

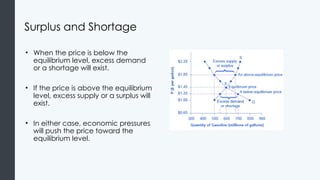

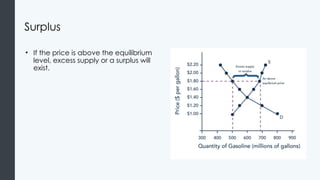

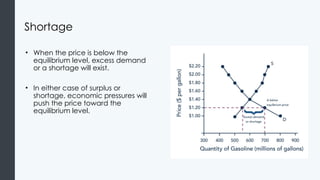

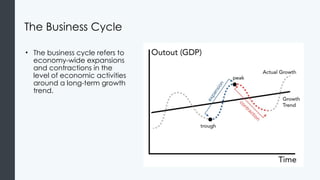

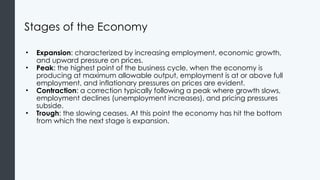

This document provides an overview of economic principles and their impact on business environments, covering topics such as the definition of economics, the law of demand and supply, market equilibrium, and economic systems. It explains key concepts like scarcity, opportunity cost, division of labor, and the importance of economic indicators such as GDP and unemployment rates in evaluating economic health. Additionally, it highlights the business cycle's stages: expansion, peak, contraction, and trough, and their implications for business operations.