Economic Outlook OECD November 2022

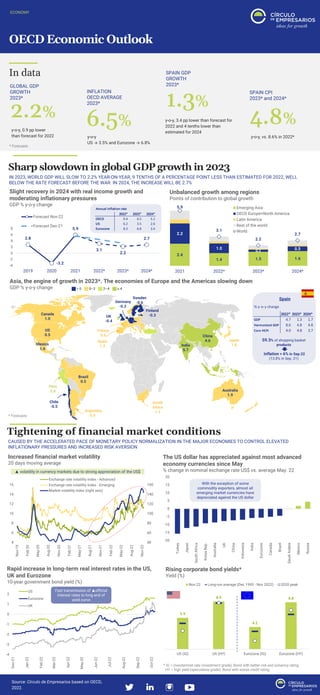

Sharp slowdown in global GDP growth in 2023 IN 2023, WORLD GDP WILL SLOW TO 2.2% YEAR-ON-YEAR, 9 TENTHS OF A PERCENTAGE POINT LESS THAN ESTIMATED FOR 2022, WELL BELOW THE RATE FORECAST BEFORE THE WAR. IN 2024, THE INCREASE WILL BE 2.7% Slight recovery in 2024 with real income growth and moderating inflationary pressures Unbalanced growth among regions Asia, the engine of growth in 2023*. The economies of Europe and the Americas slowing down Tightening of financial market conditions CAUSED BY THE ACCELERATED PACE OF MONETARY POLICY NORMALIZATION IN THE MAJOR ECONOMIES TO CONTROL ELEVATED INFLATIONARY PRESSURES AND INCREASED RISK AVERSION Increased financial market volatility The US dollar has appreciated against most advanced economy currencies since May Rapid increase in long-term real interest rates in the US, UK and Eurozone Rising corporate bond yields

Recommended

Recommended

More Related Content

Similar to Economic Outlook OECD November 2022

Similar to Economic Outlook OECD November 2022 (20)

More from Círculo de Empresarios

More from Círculo de Empresarios (20)

Recently uploaded

Recently uploaded (20)

Economic Outlook OECD November 2022

- 1. Annual inflation rate 2022* 2023* 2024* OECD 9.4 6.5 5.1 US 6.2 3.5 2.6 Eurozone 8.3 6.8 3.4 2.8 -3.2 5.9 3.1 2.2 2.7 -4 -2 0 2 4 6 8 2019 2020 2021 2022* 2023* 2024* Forecast Nov-22 Forecast Dec-21 -4 -3 -2 -1 0 1 2 Dec-21 Jan-22 Feb-22 Mar-22 Apr-22 May-22 Jun-22 Jul-22 Aug-22 Sep-22 Oct-22 US Eurozone UK OECD Economic Outlook ECONOMY In data Sharp slowdown in global GDP growth in 2023 Source: Círculo de Empresarios based on OECD, 2022. INFLATION OECD AVERAGE 2023* 6.5% y-o-y US → 3.5% and Eurozone → 6.8% 1.3% SPAIN GDP GROWTH 2023* y-o-y, 3.4 pp lower than forecast for 2022 and 4 tenths lower than estimated for 2024 SPAIN CPI 2023* and 2024* 4.8% y-o-y, vs. 8.6% in 2022* GLOBAL GDP GROWTH 2023* y-o-y, 0.9 pp lower than forecast for 2022 2.2% * Forecasts IN 2023, WORLD GDP WILL SLOW TO 2.2% YEAR-ON-YEAR, 9 TENTHS OF A PERCENTAGE POINT LESS THAN ESTIMATED FOR 2022, WELL BELOW THE RATE FORECAST BEFORE THE WAR. IN 2024, THE INCREASE WILL BE 2.7% * Forecasts Slight recovery in 2024 with real income growth and moderating inflationary pressures GDP % y-o-y change Unbalanced growth among regions Points of contribution to global growth 2.4 1.4 1.5 1.6 2.2 1.0 0.2 0.5 5.9 3.1 2.2 2.7 2021 2022* 2023* 2024* Emerging Asia OECD Europe+North America Latin America Rest of the world World Tightening of financial market conditions CAUSED BY THE ACCELERATED PACE OF MONETARY POLICY NORMALIZATION IN THE MAJOR ECONOMIES TO CONTROL ELEVATED INFLATIONARY PRESSURES AND INCREASED RISK AVERSION Increased financial market volatility 20 days moving average 40 60 80 100 120 140 160 4 6 8 10 12 14 16 Nov-19 Feb-20 May-20 Aug-20 Nov-20 Feb-21 May-21 Aug-21 Nov-21 Feb-22 May-22 Aug-22 Nov-22 Exchange rate volatility index - Advanced Exchange rate volatility index - Emerging Market volatility index (right axis) ▲ volatility in currency markets due to strong appreciation of the US$ Rising corporate bond yields* Yield (%) Asia, the engine of growth in 2023*. The economies of Europe and the Americas slowing down GDP % y-o-y change Fast transmission of ▲official interest rates to long end of yield curve Rapid increase in long-term real interest rates in the US, UK and Eurozone 10-year government bond yield (%) The US dollar has appreciated against most advanced economy currencies since May % change in nominal exchange rate US$ vs. average May. 22 -20 -15 -10 -5 0 5 10 15 20 Turkey Japan South Africa Korea Rep. Australia UK China Indonesia India Eurozone Canada Brazil Saudi Arabia Mexico Russia With the exception of some commodity exporters, almost all emerging market currencies have depreciated against the US dollar * IG = Investemnet rate (investment grade). Bond with better risk and solvency rating. HY = high yield (speculative grade). Bond with worse credit rating 5.9 8.9 4.2 8.8 US (IG) US (HY) Eurozone (IG) Eurozone (HY) Nov.22 Long-run average (Dec 1995 - Nov 2022) 2020 peak % y-o-y change 2022* 2023* 2024* GDP 4.7 1.3 1.7 Harmonized GDP 8.6 4.8 4.8 Core HCPI 4.0 4.8 3.7 59.3% of shopping basket products inflation > 6% in Sep.22 (13.8% in Sep. 21) Spain