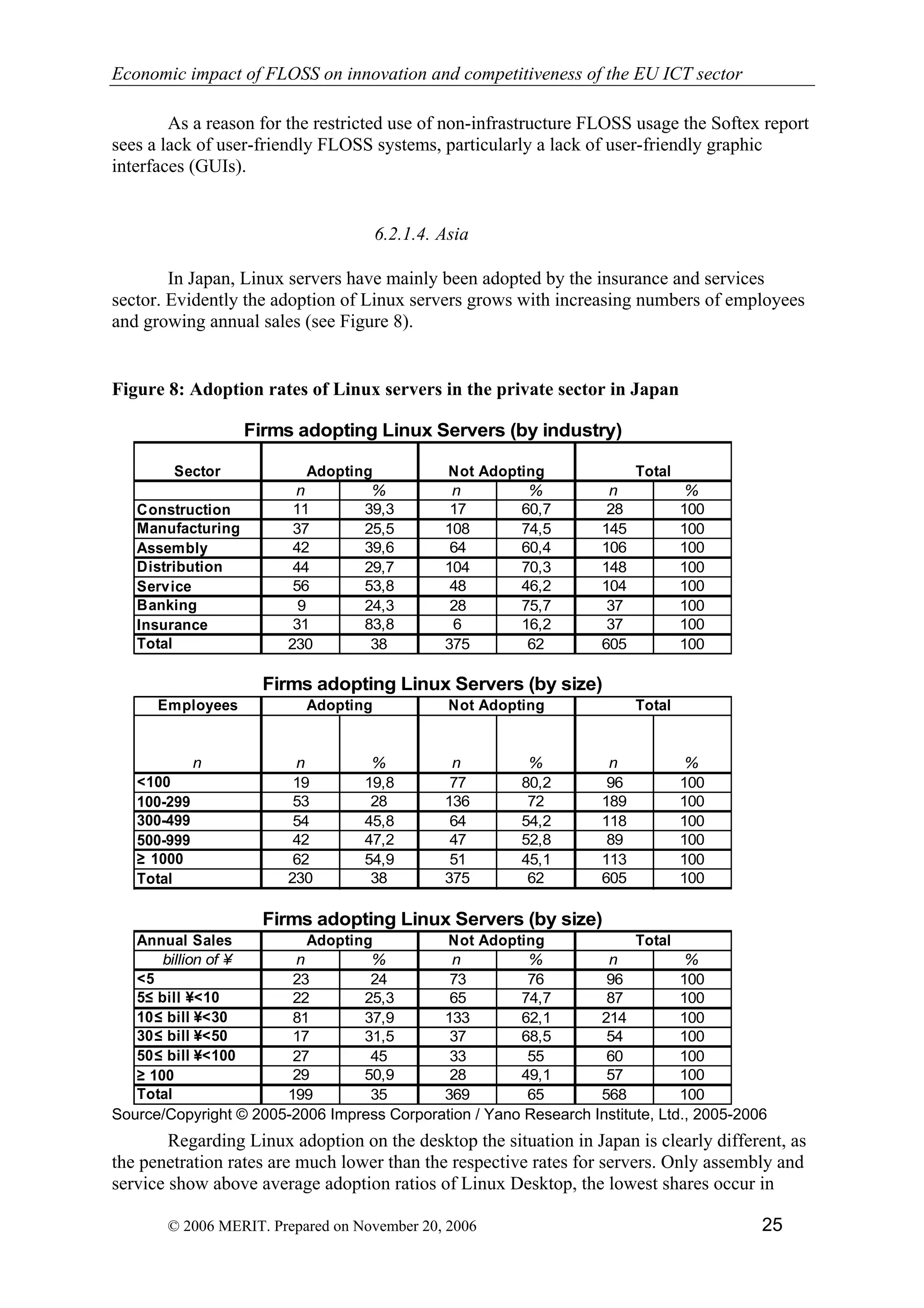

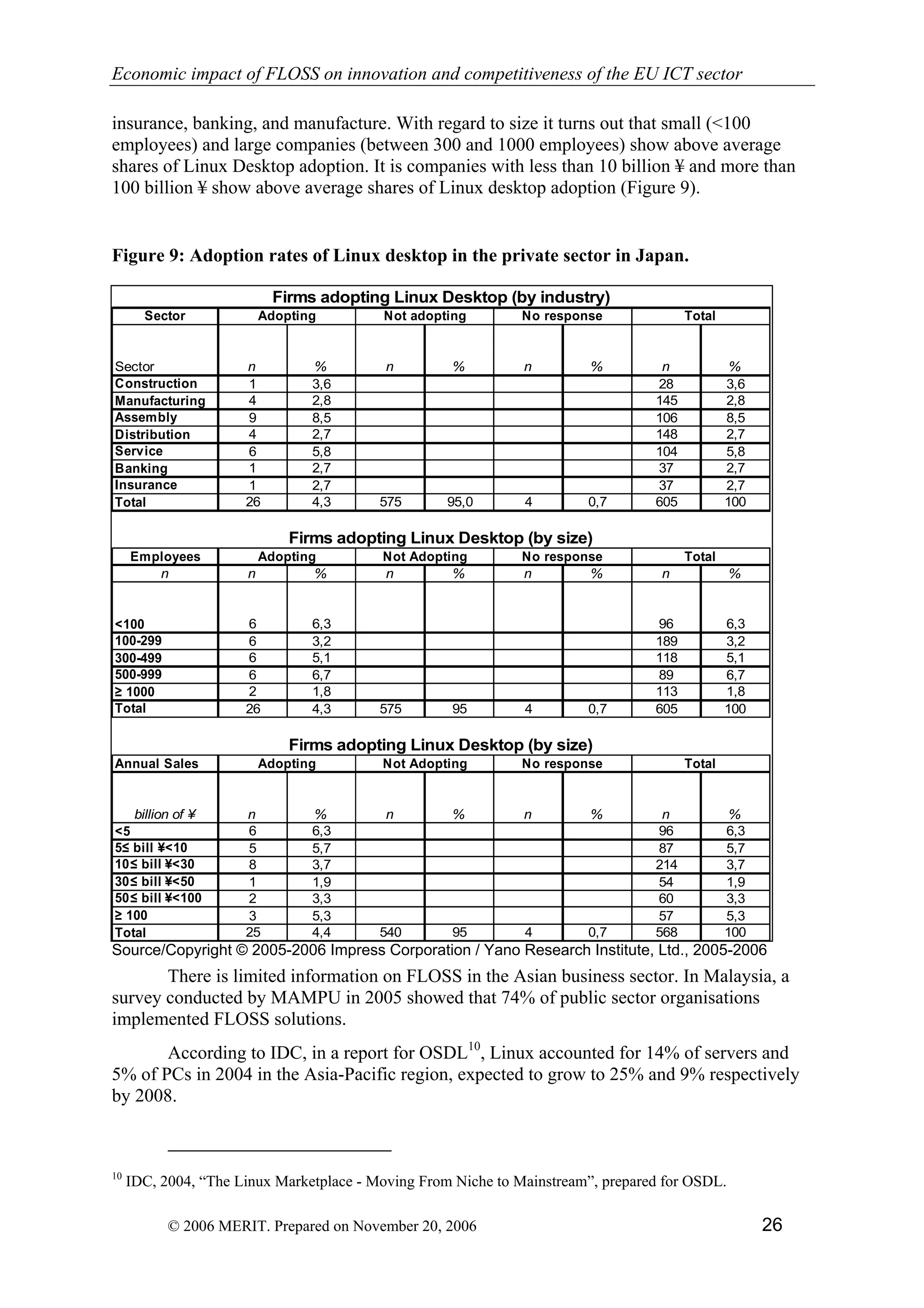

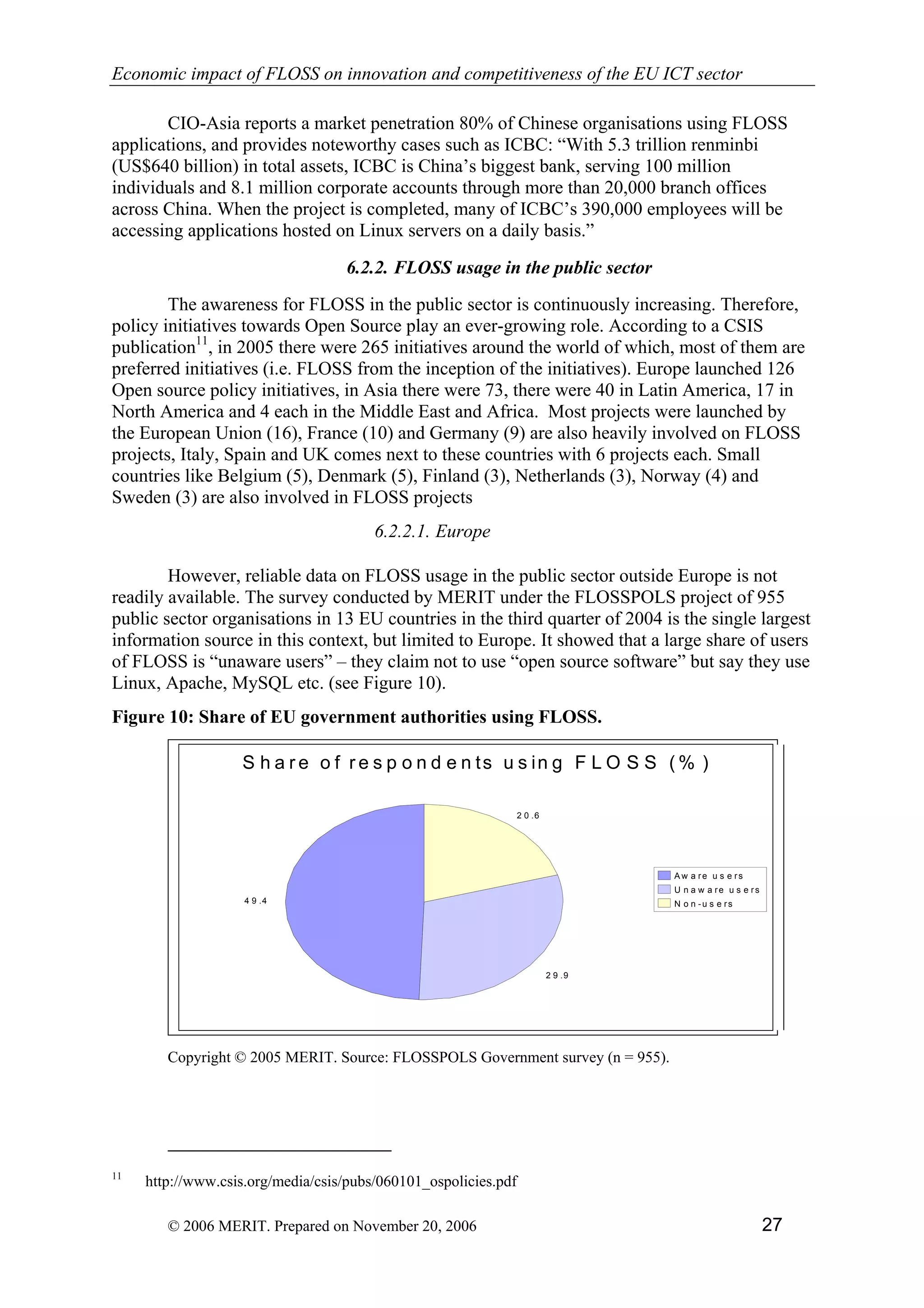

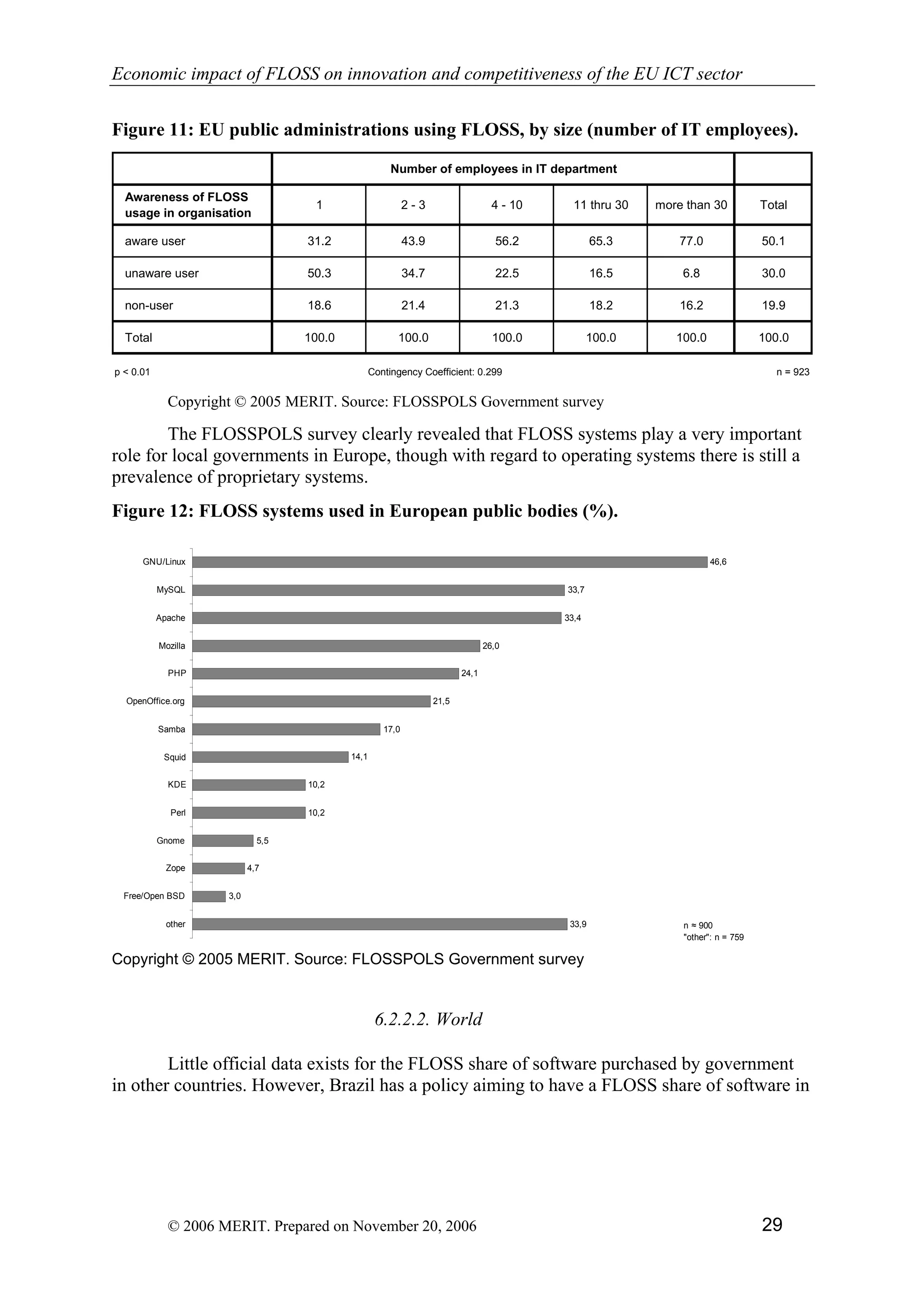

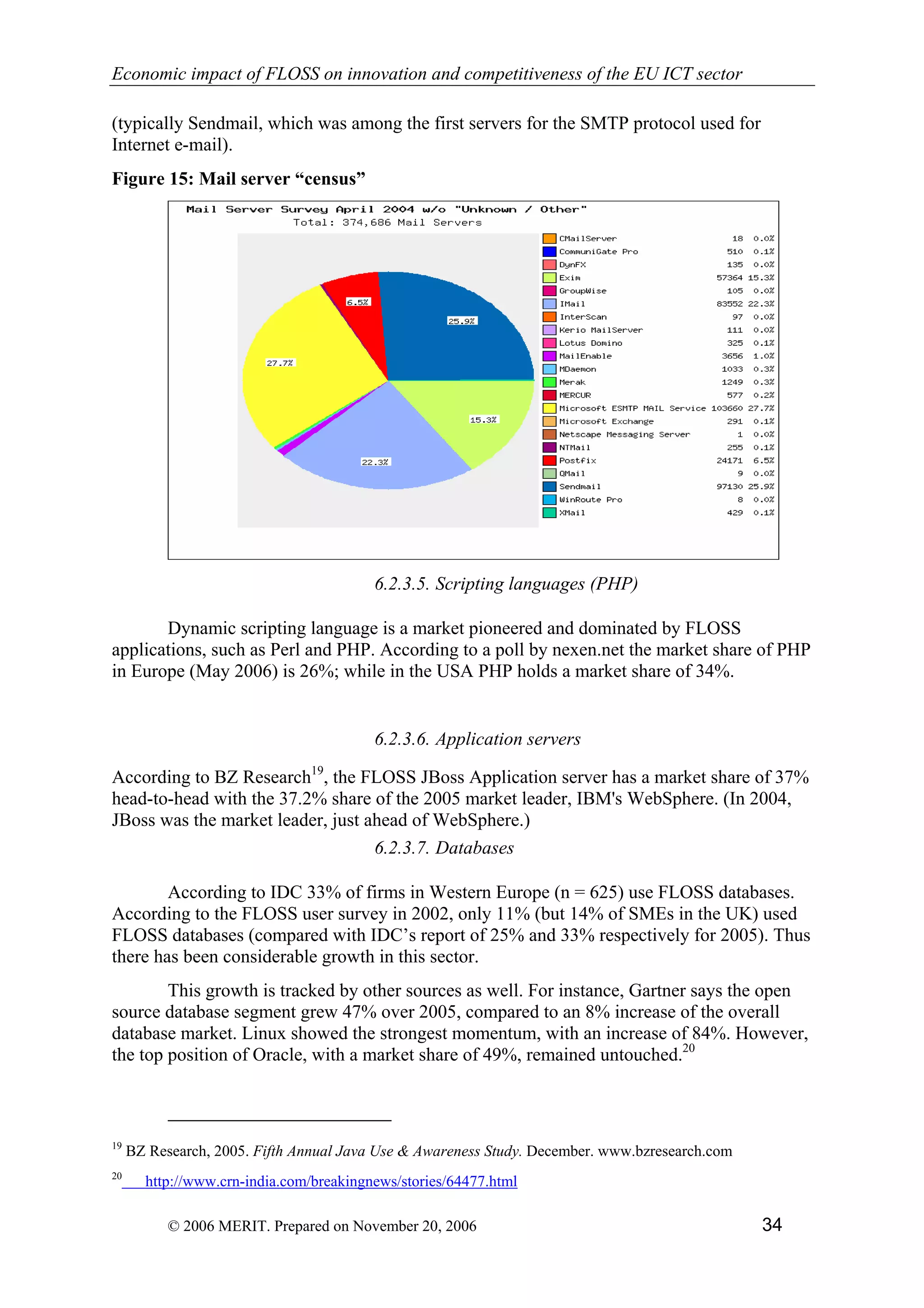

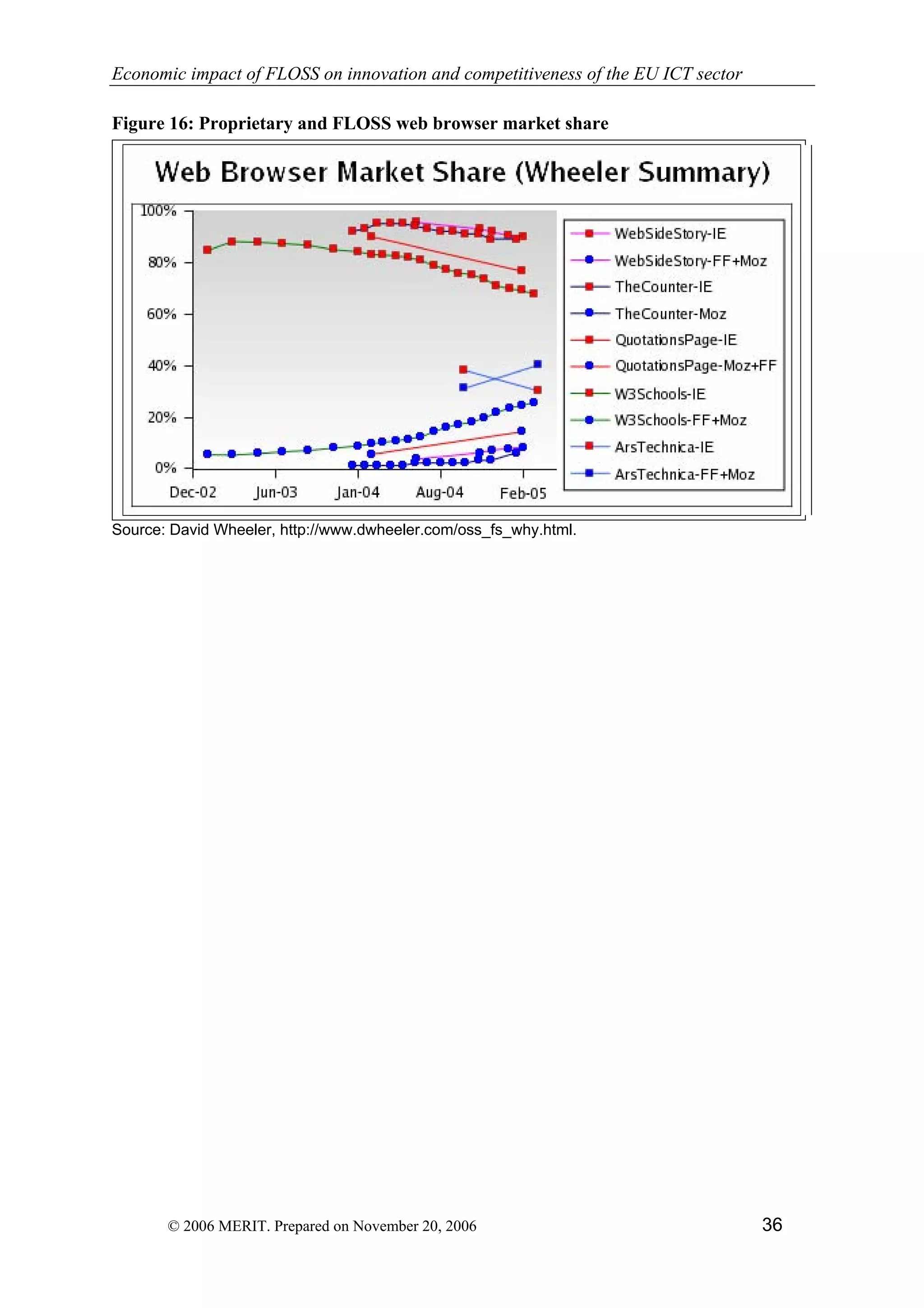

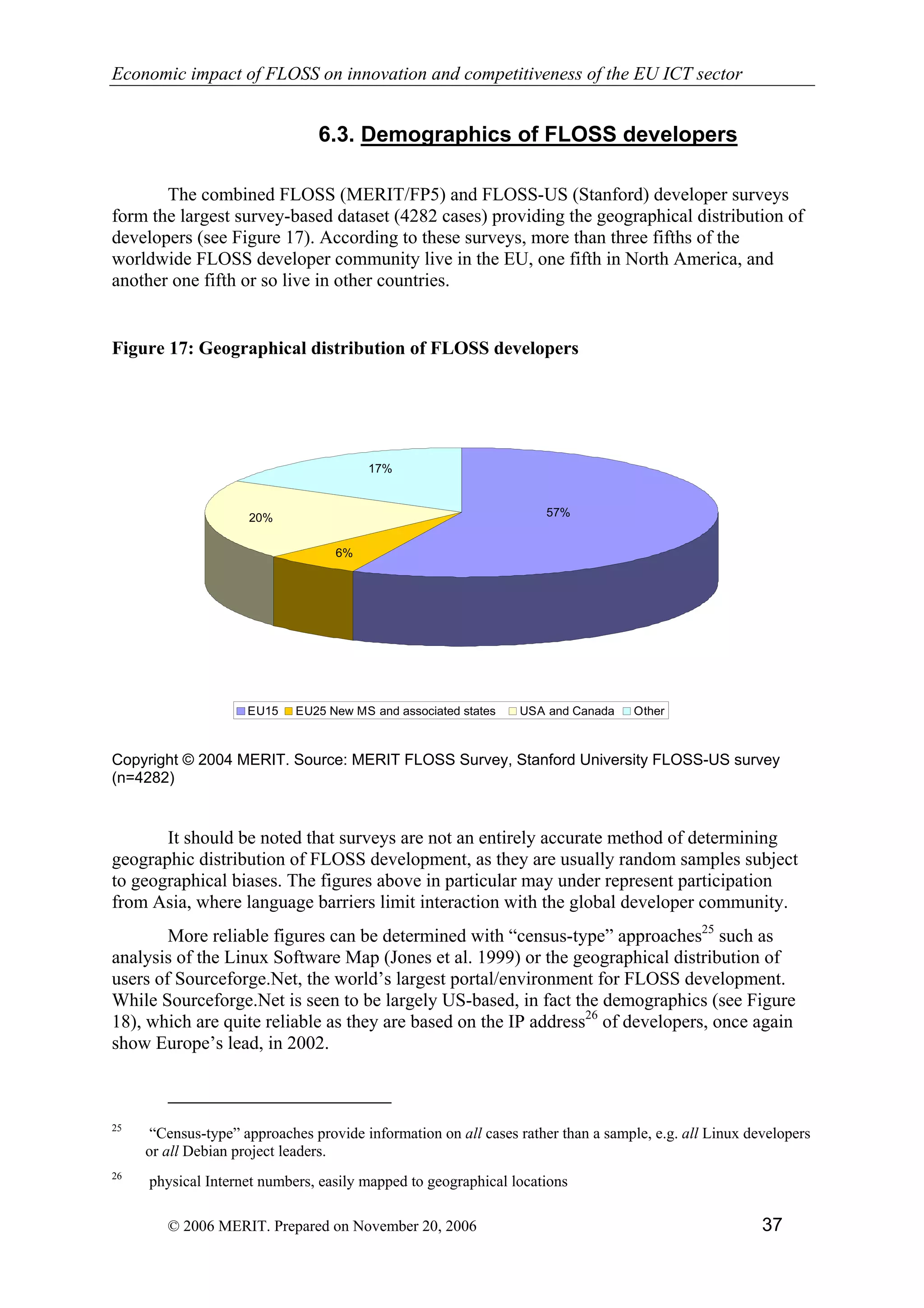

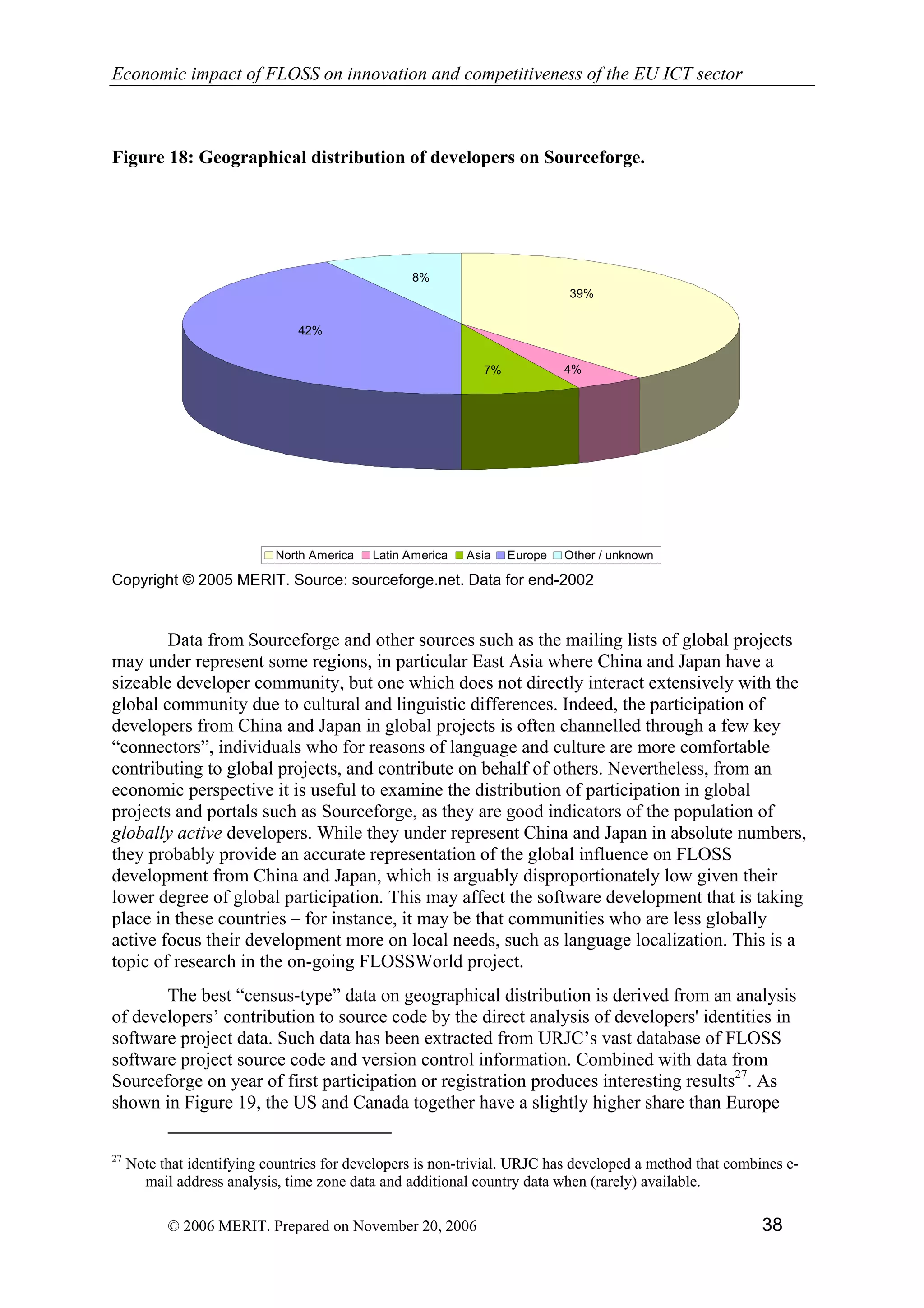

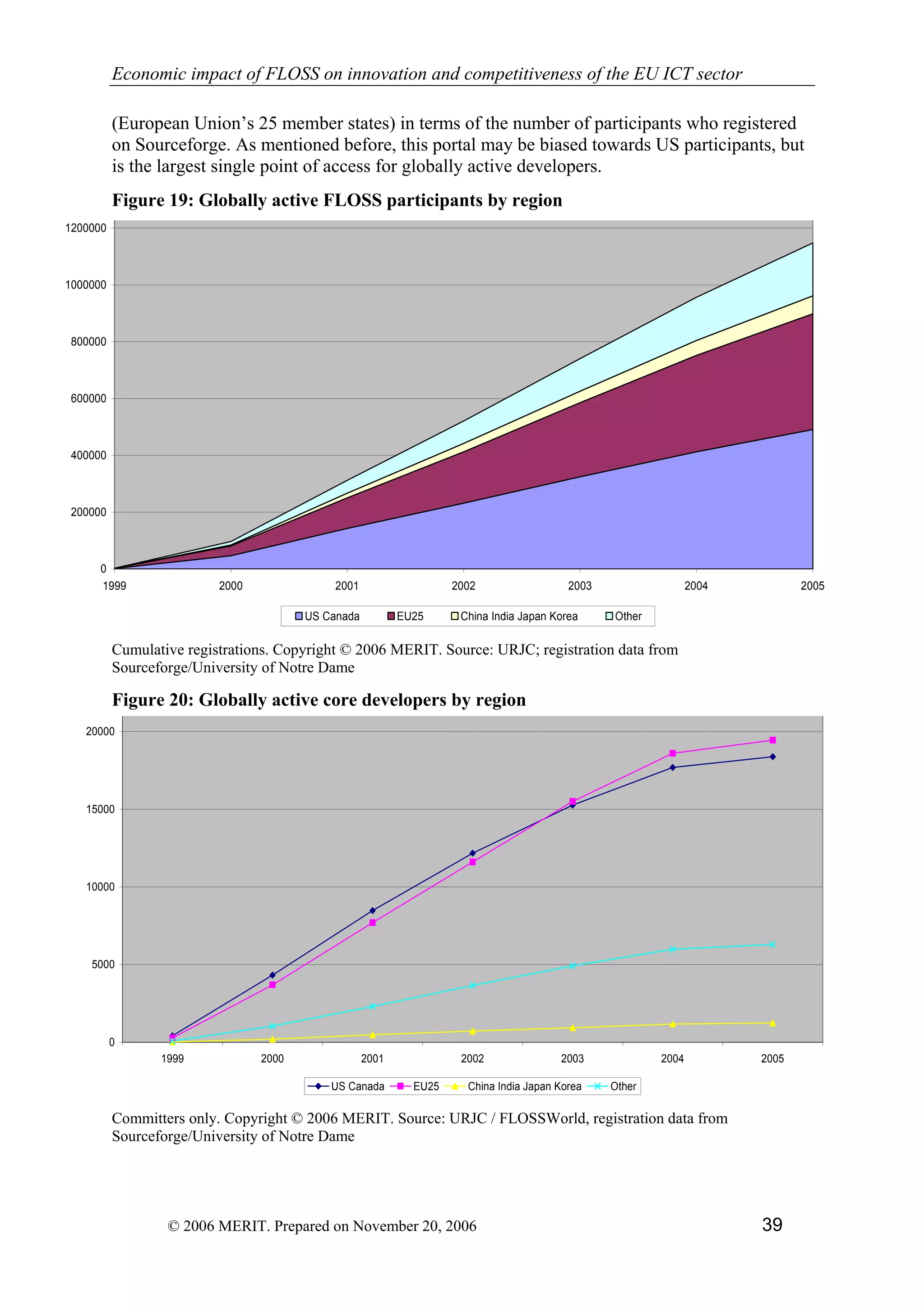

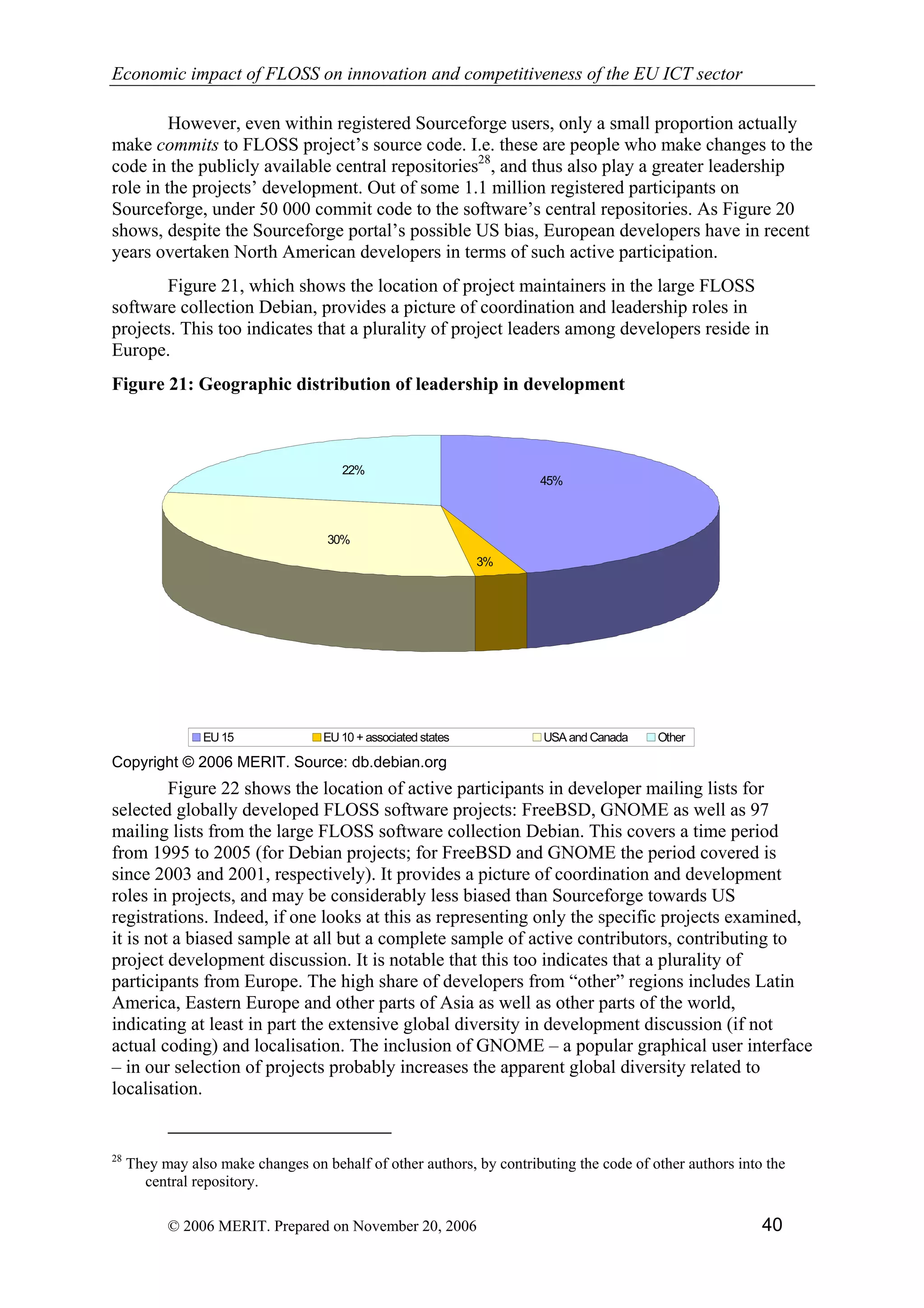

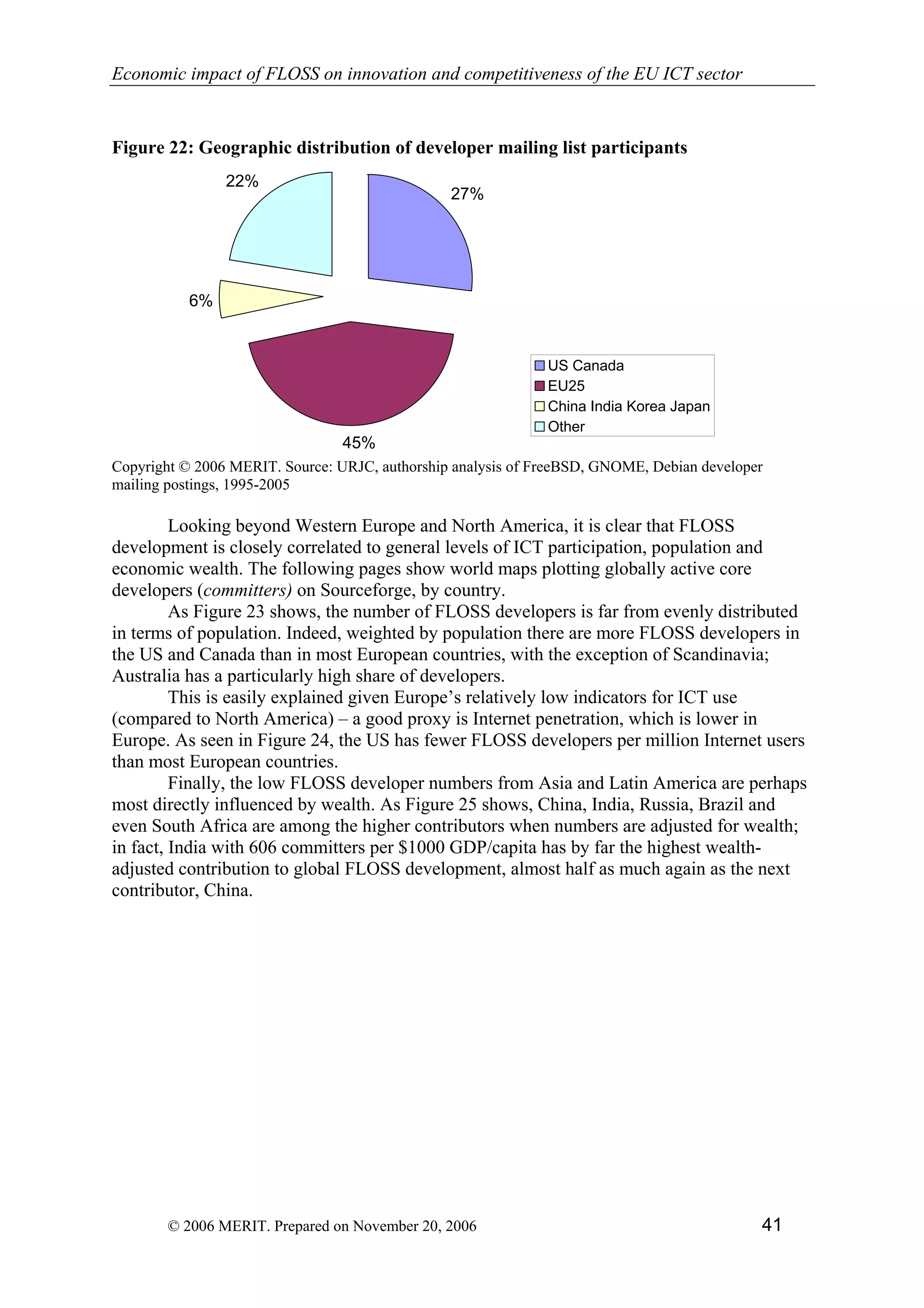

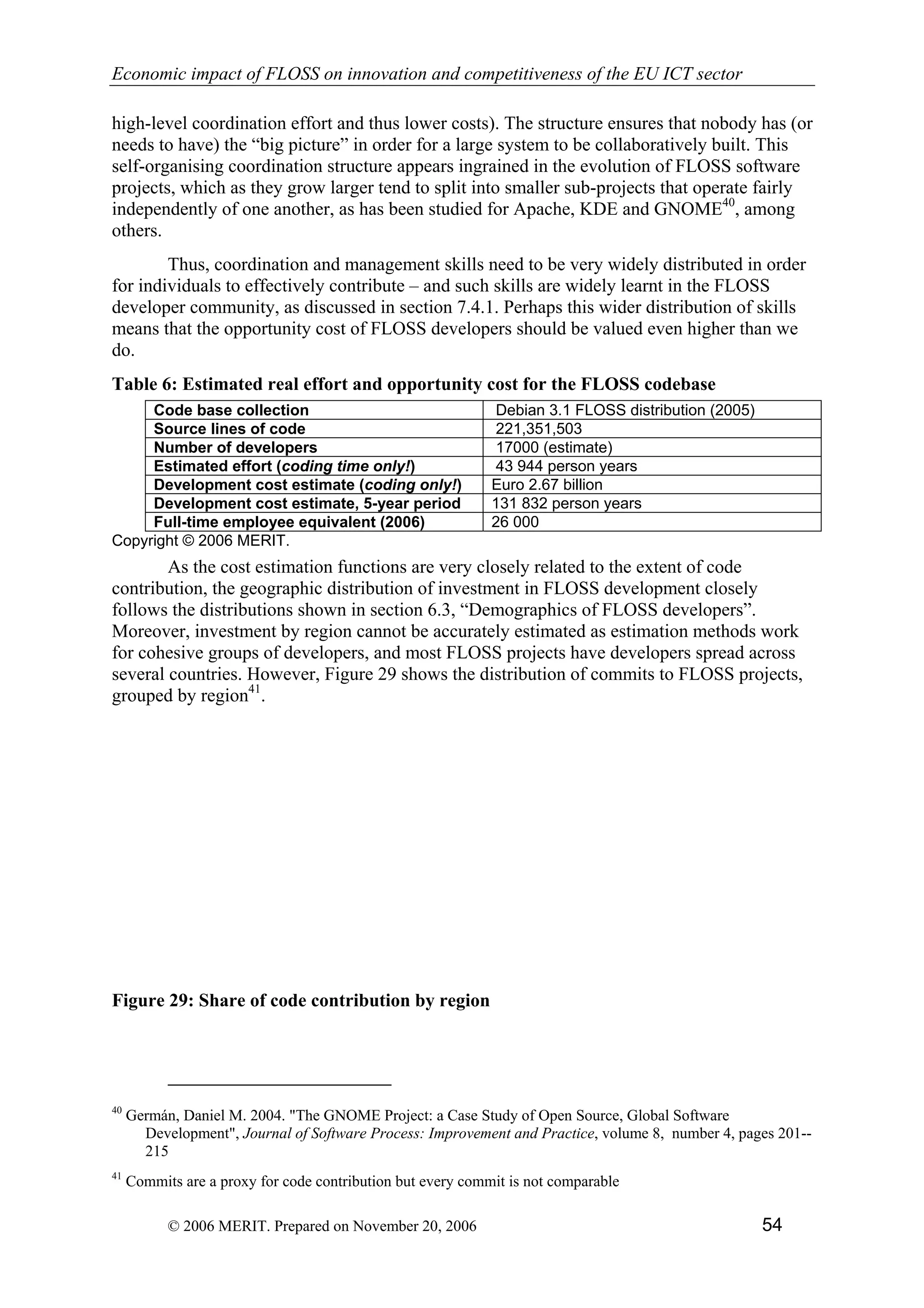

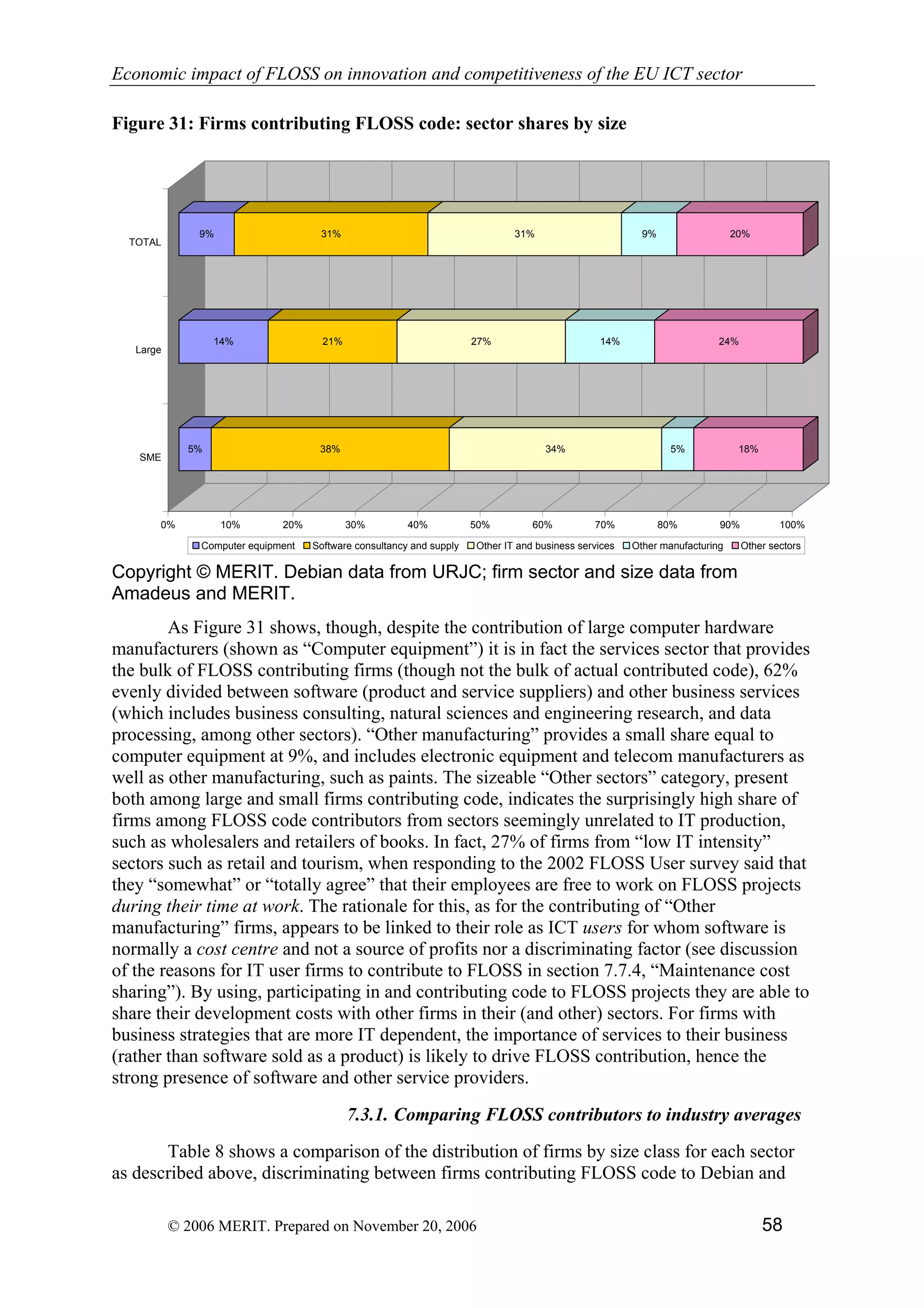

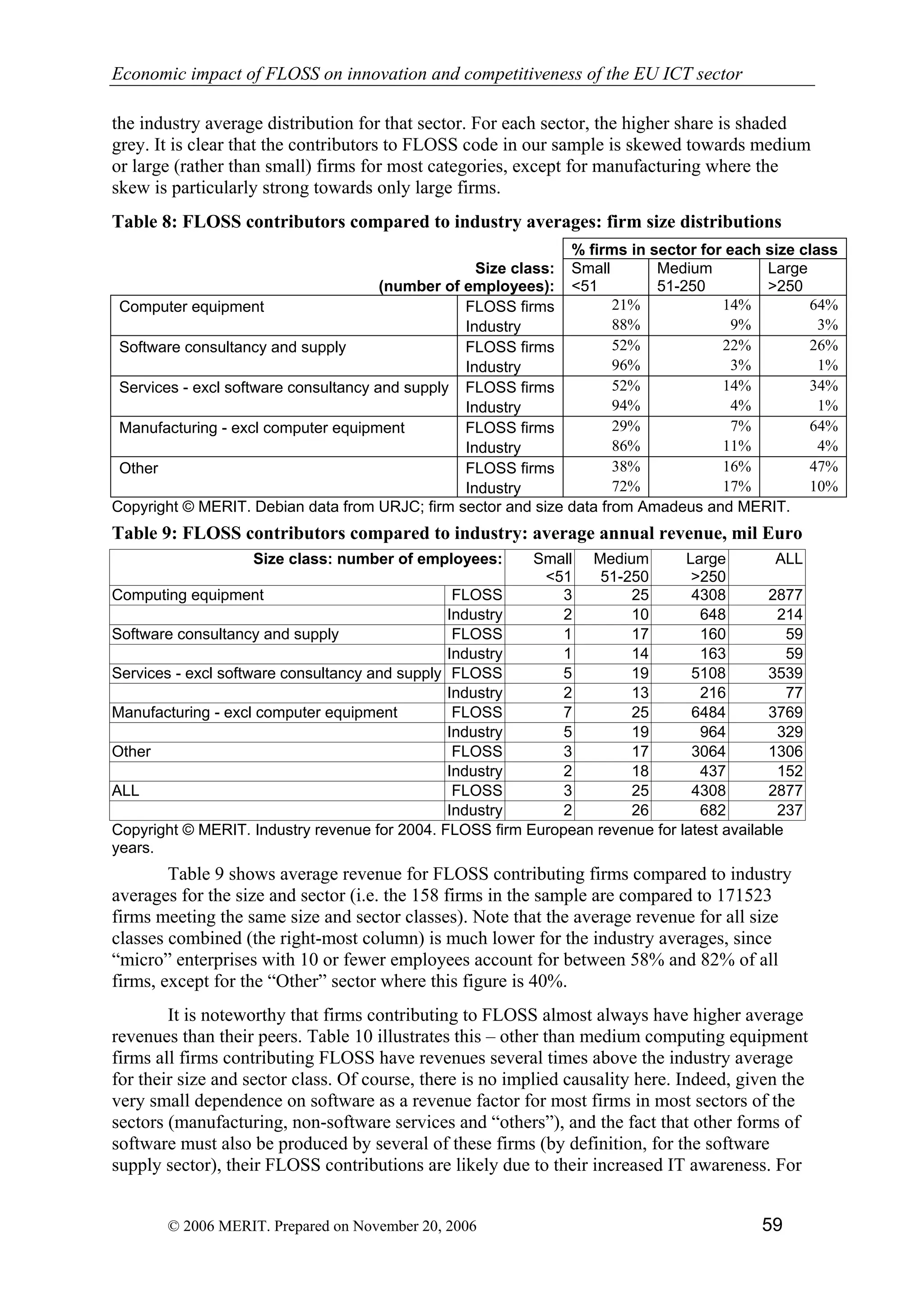

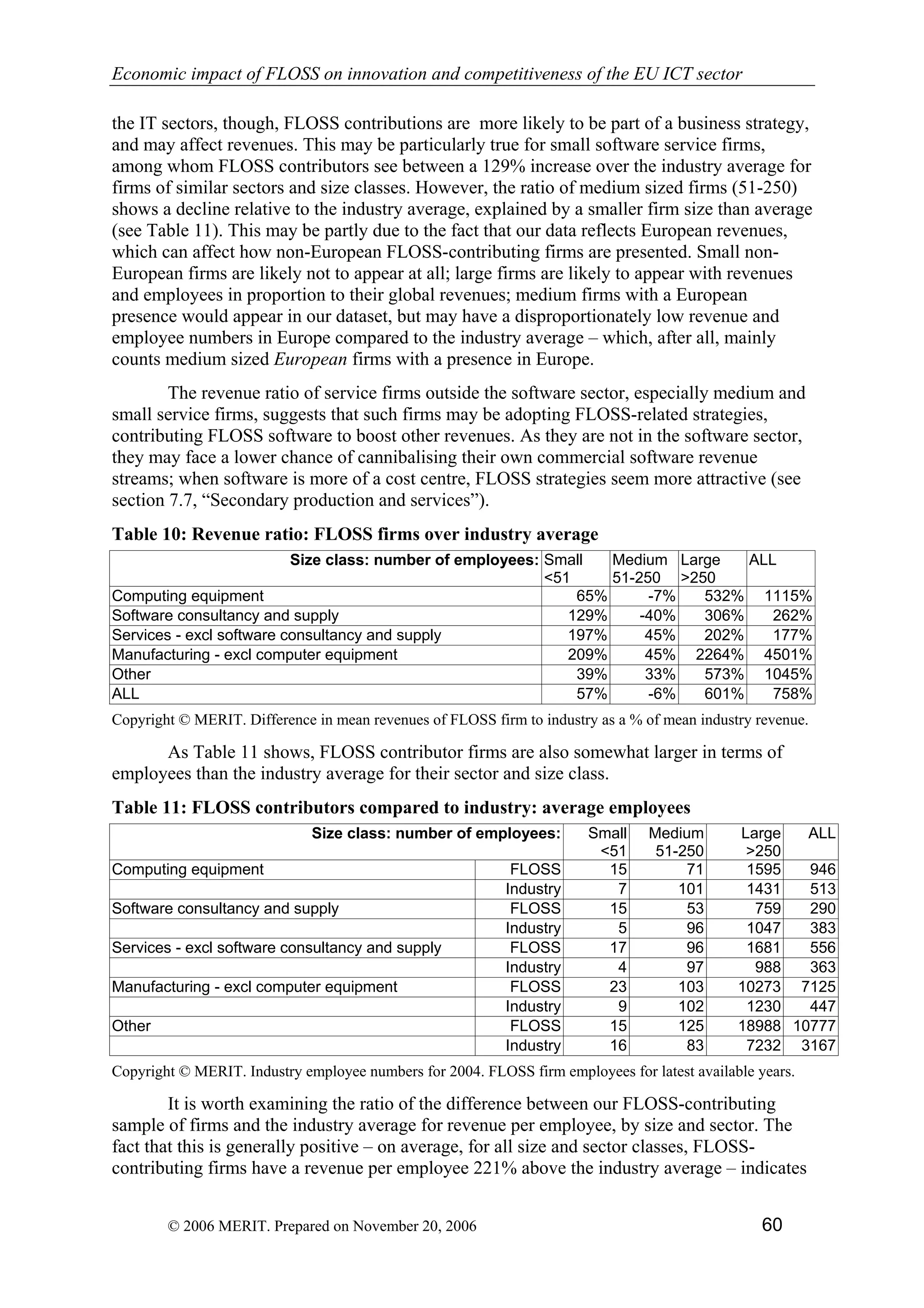

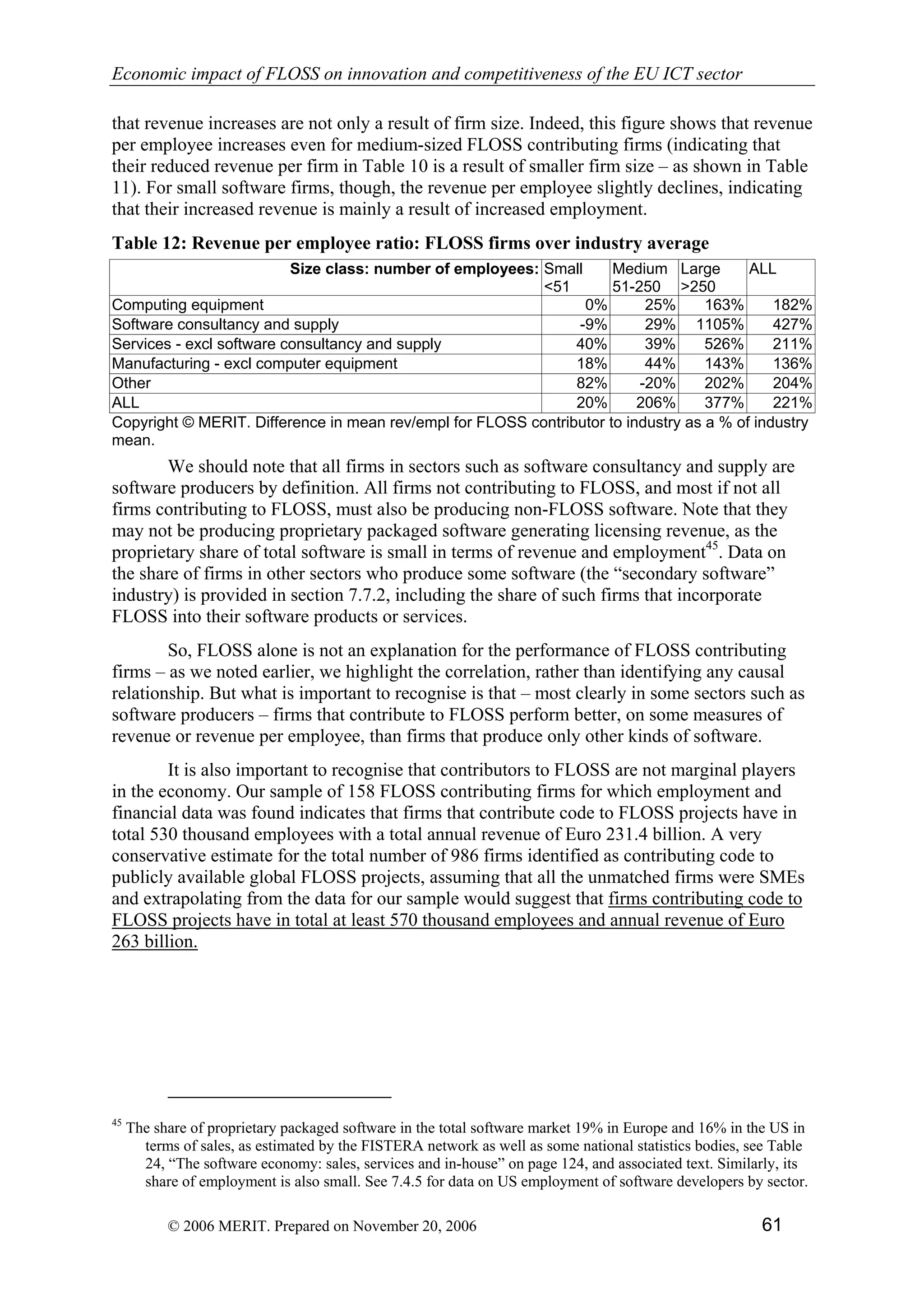

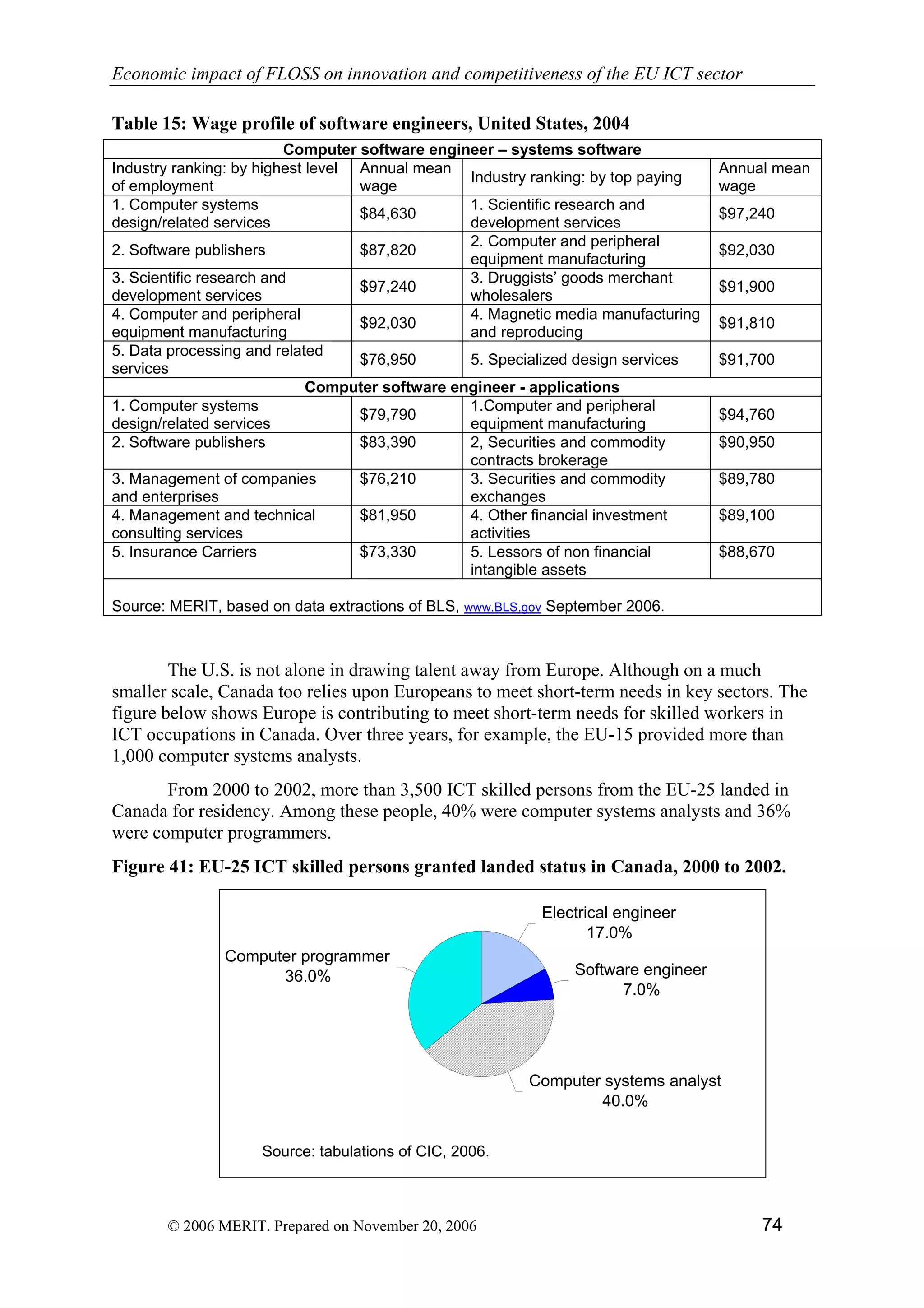

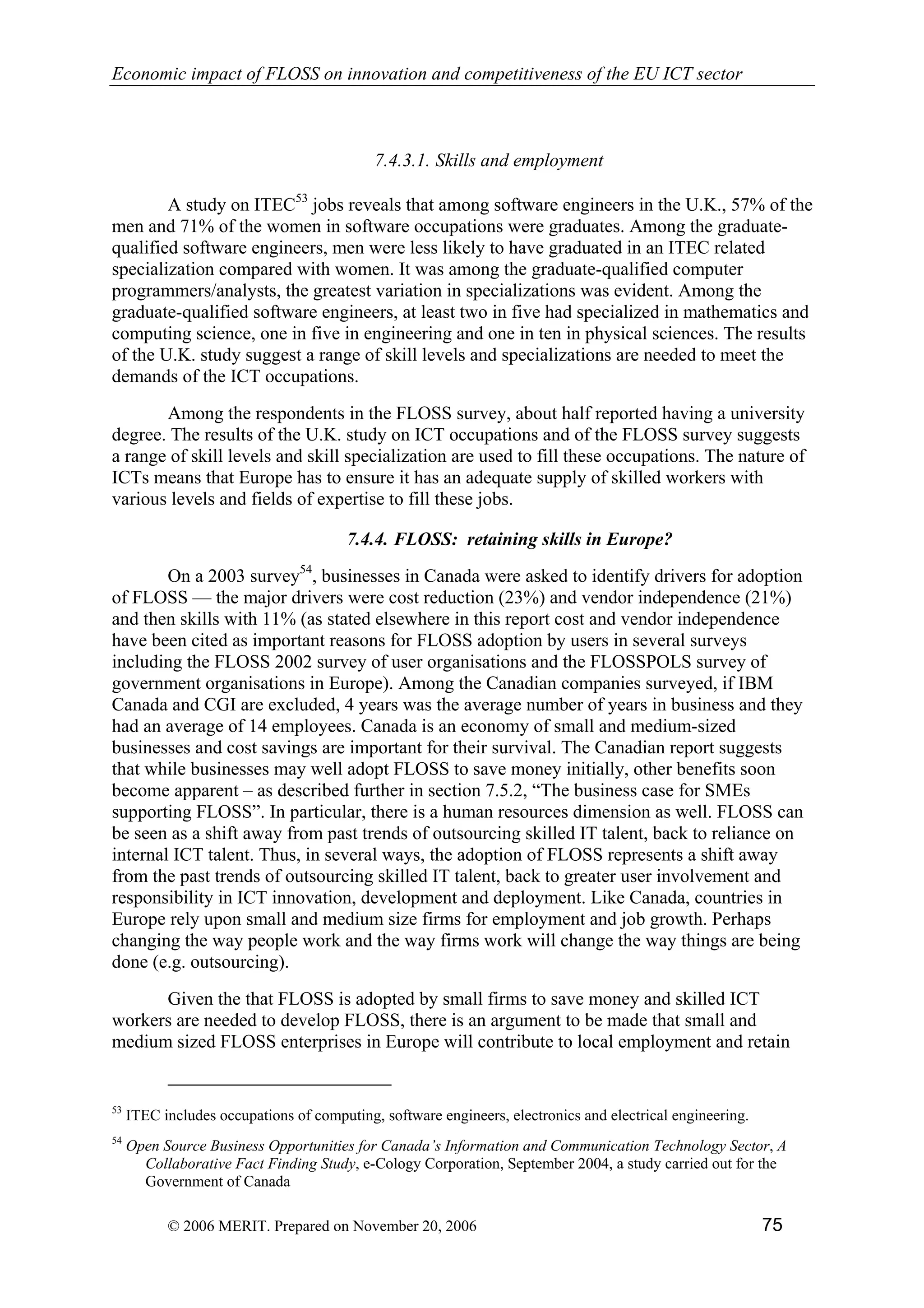

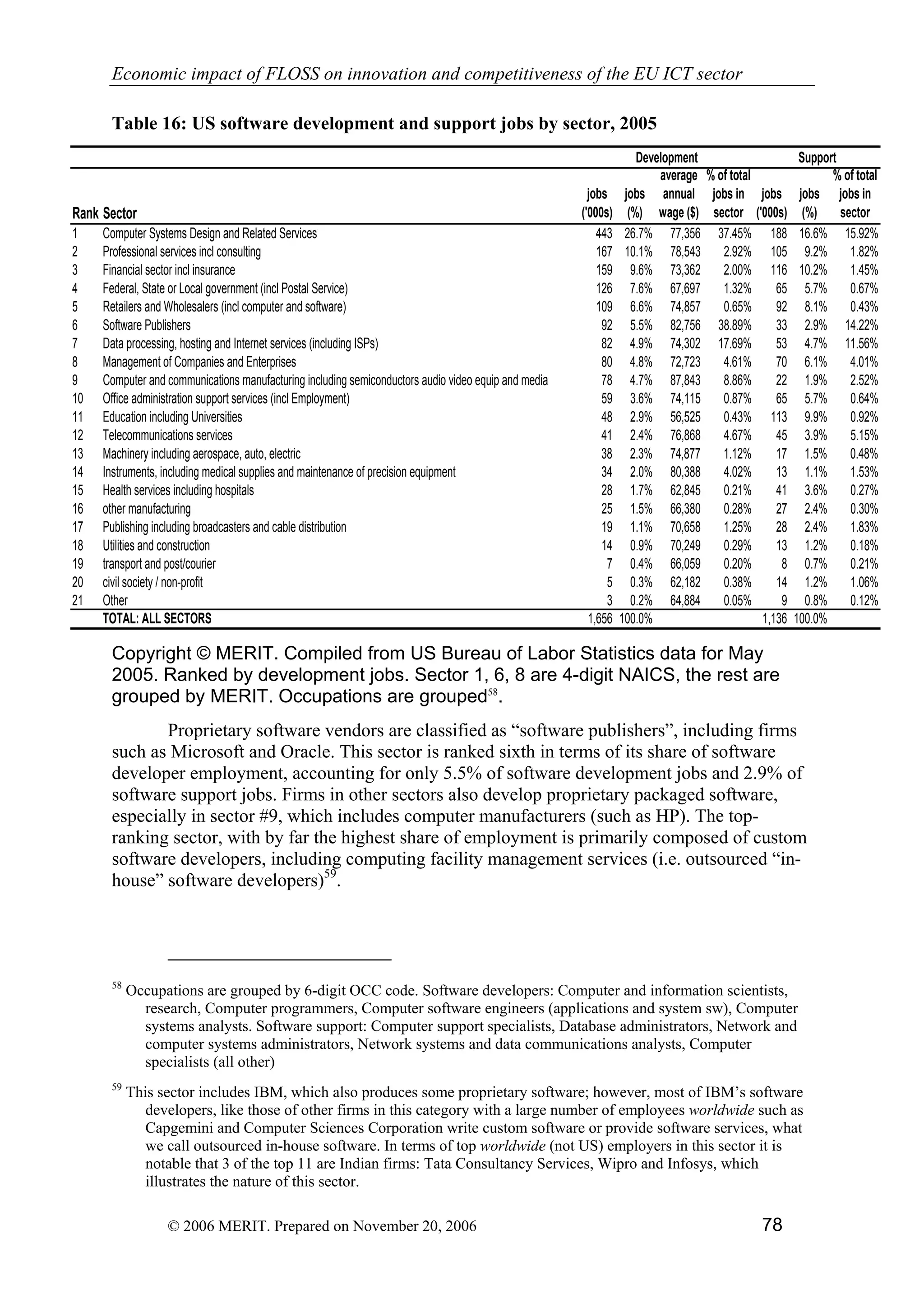

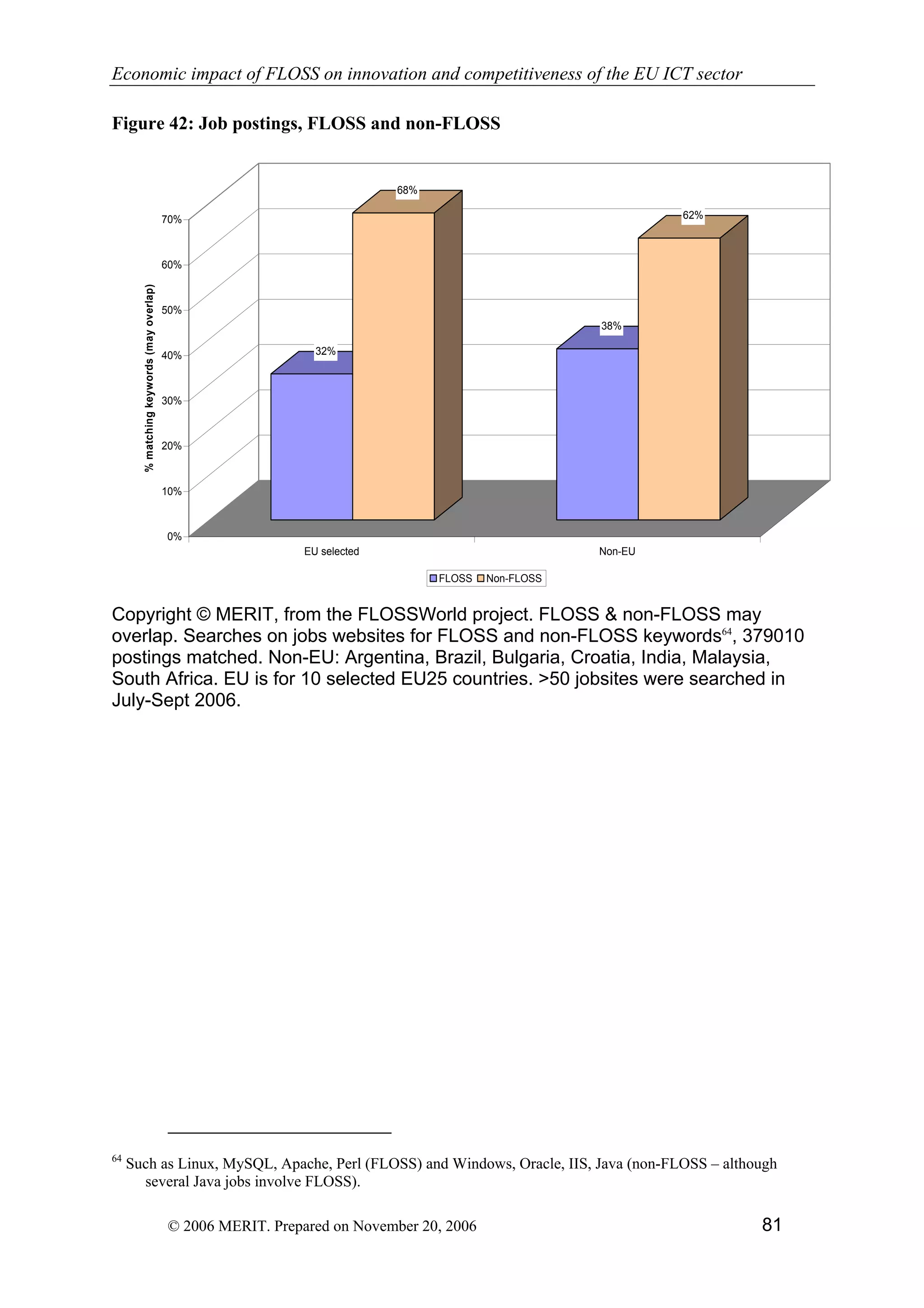

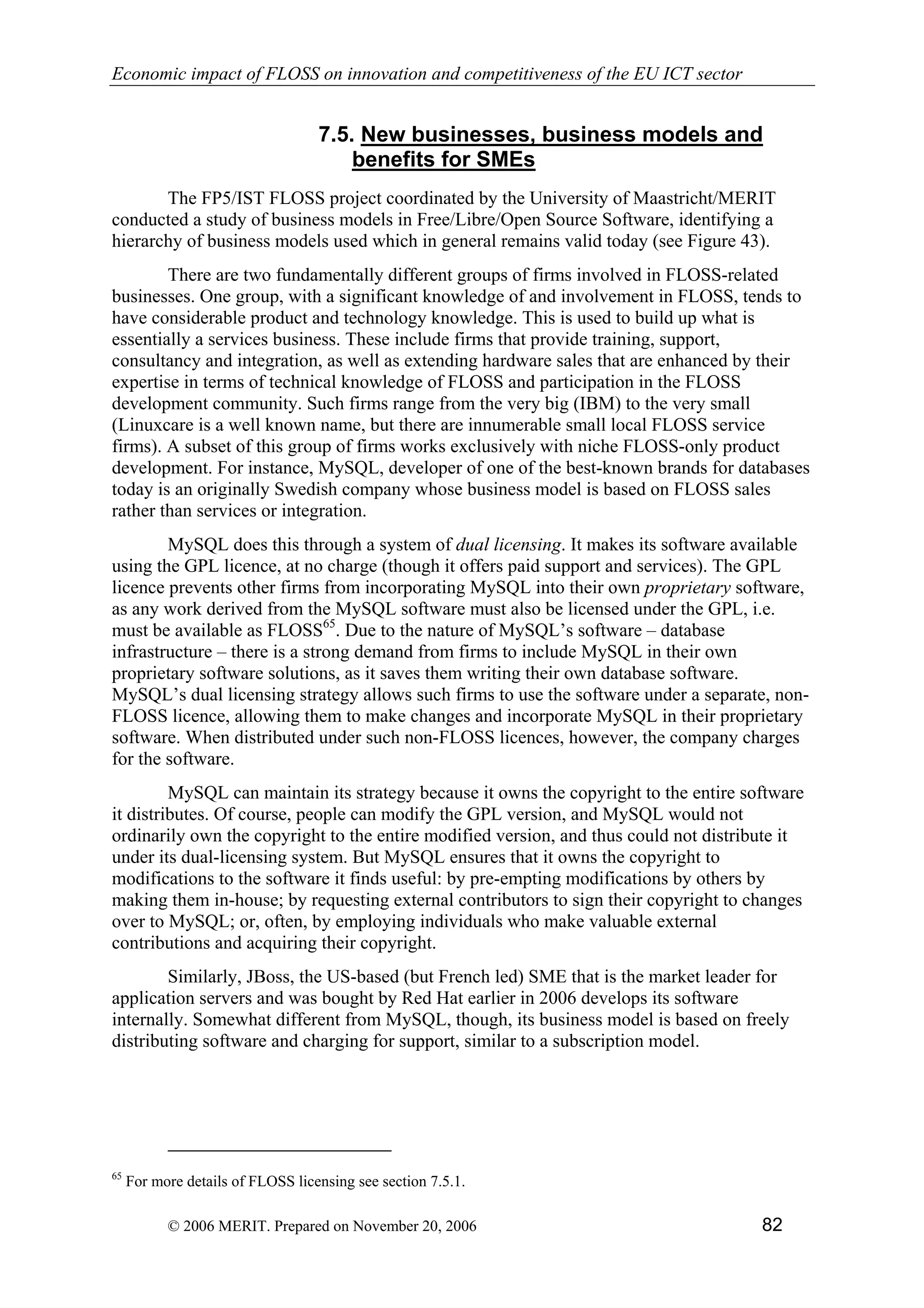

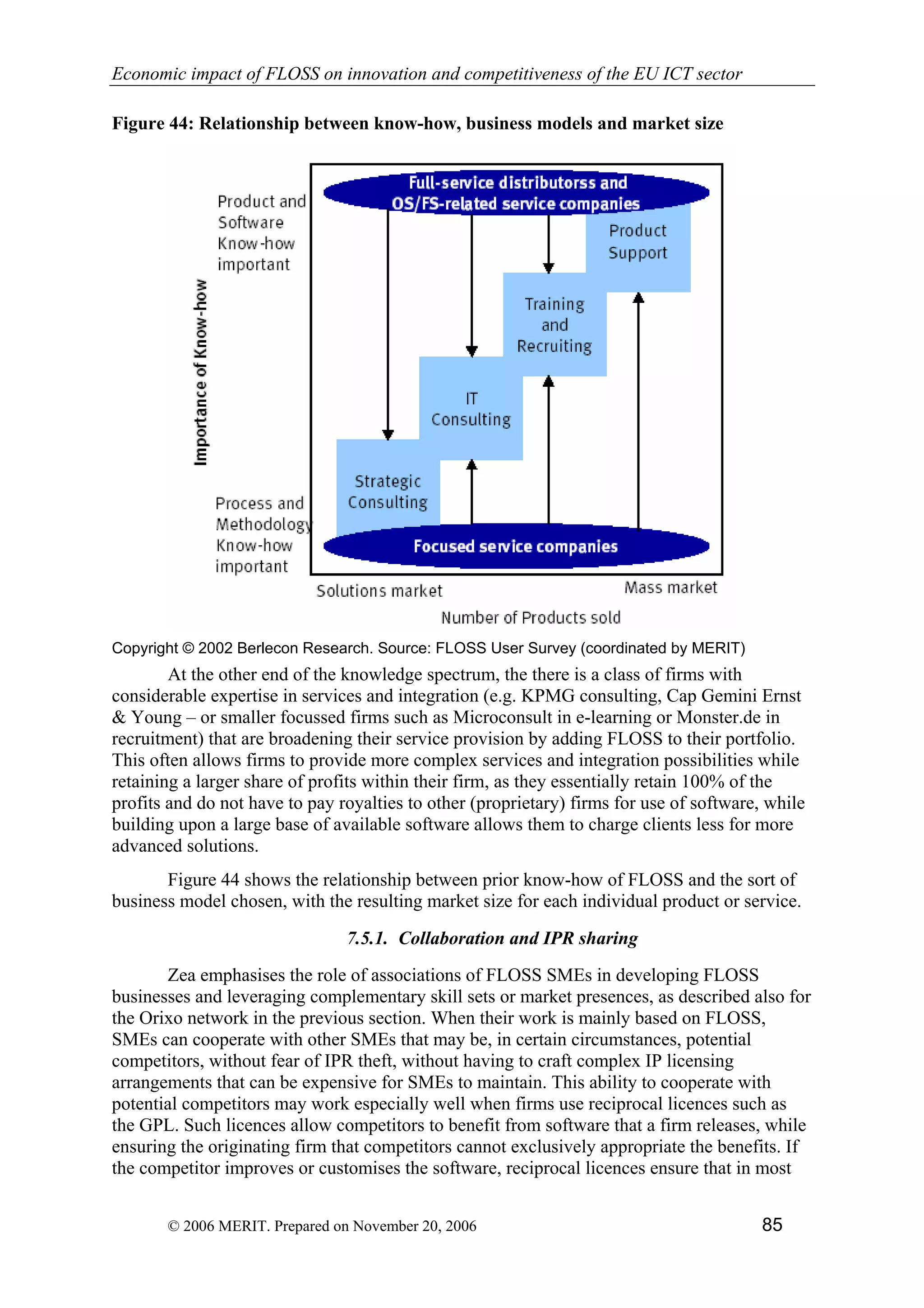

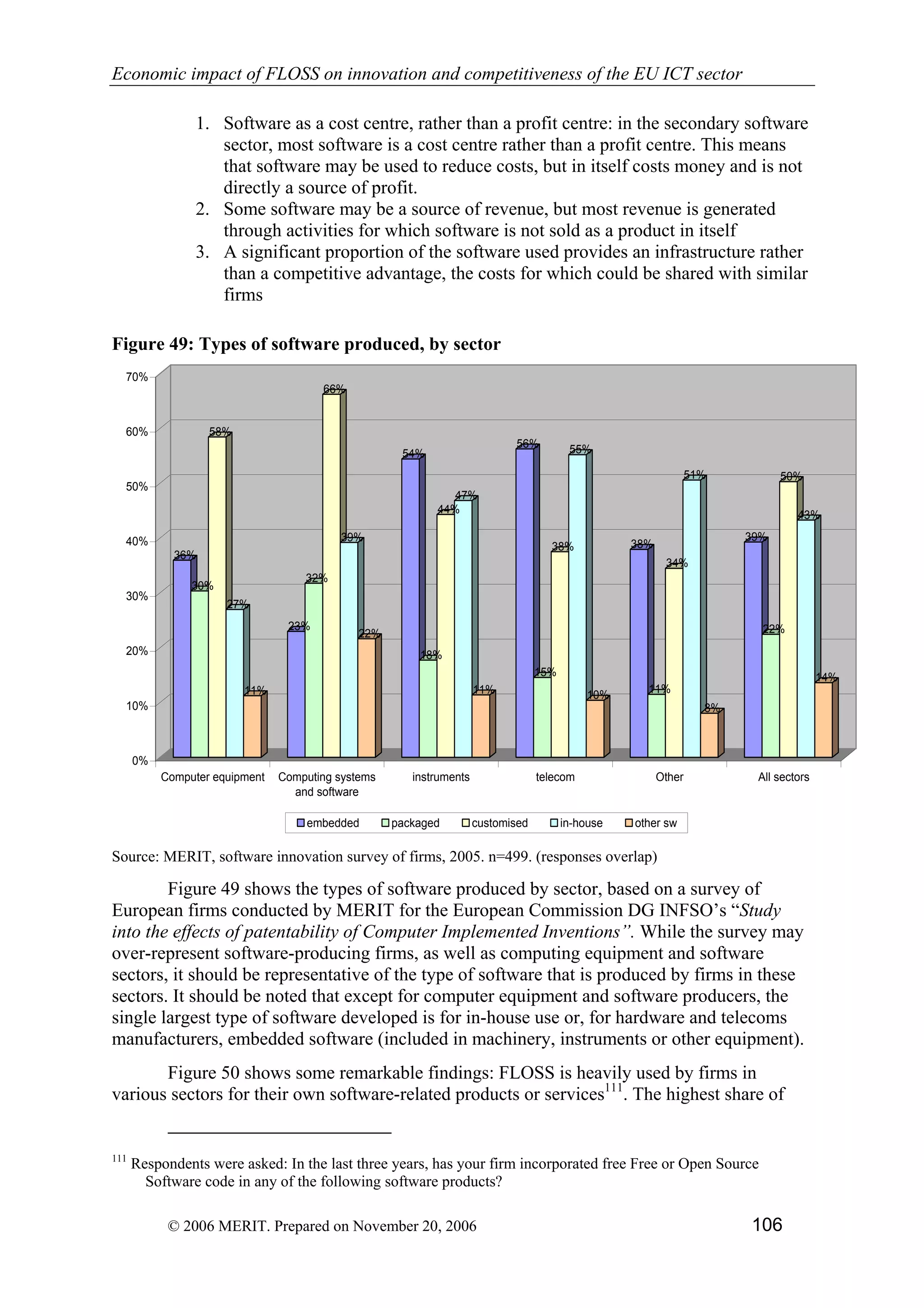

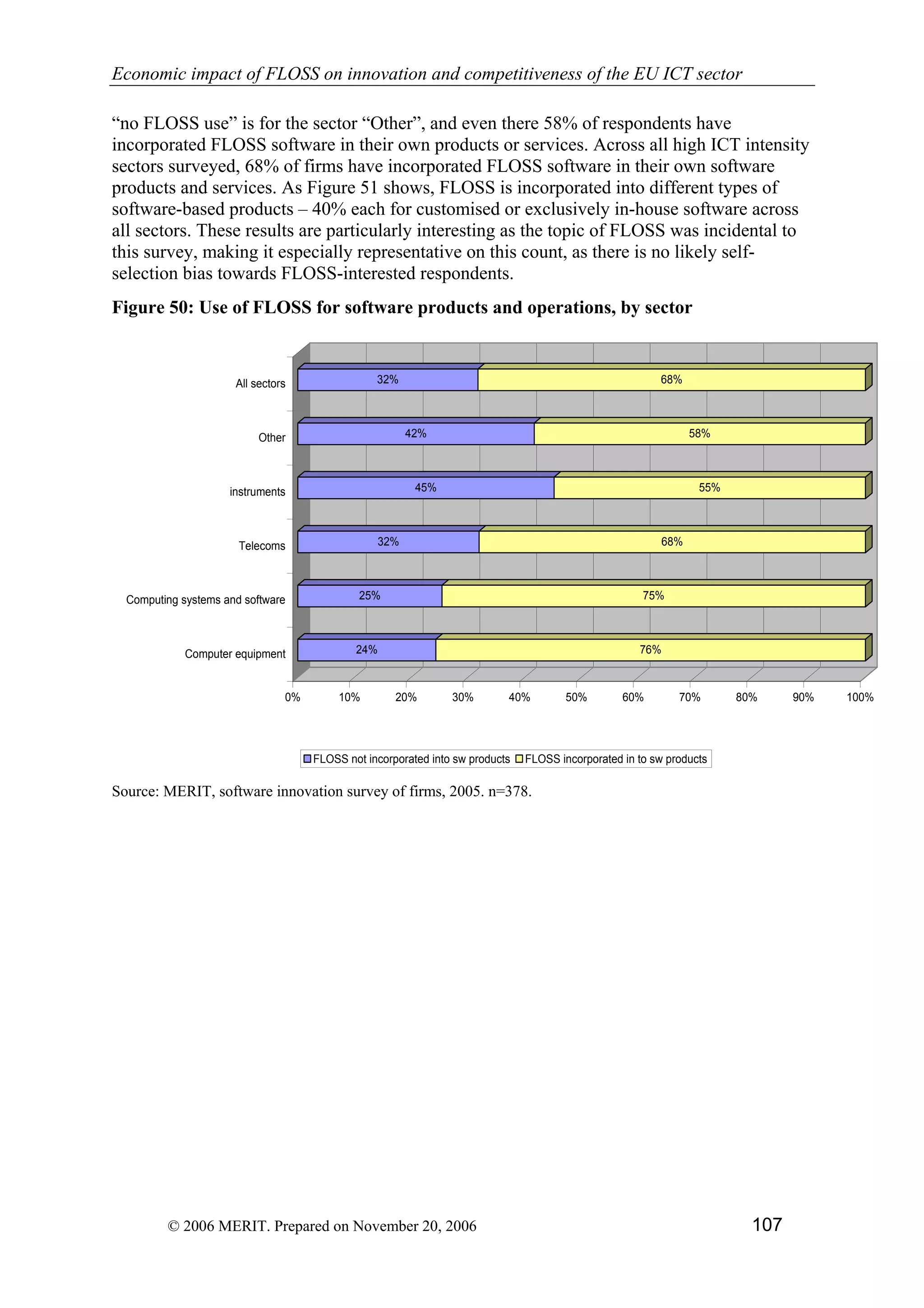

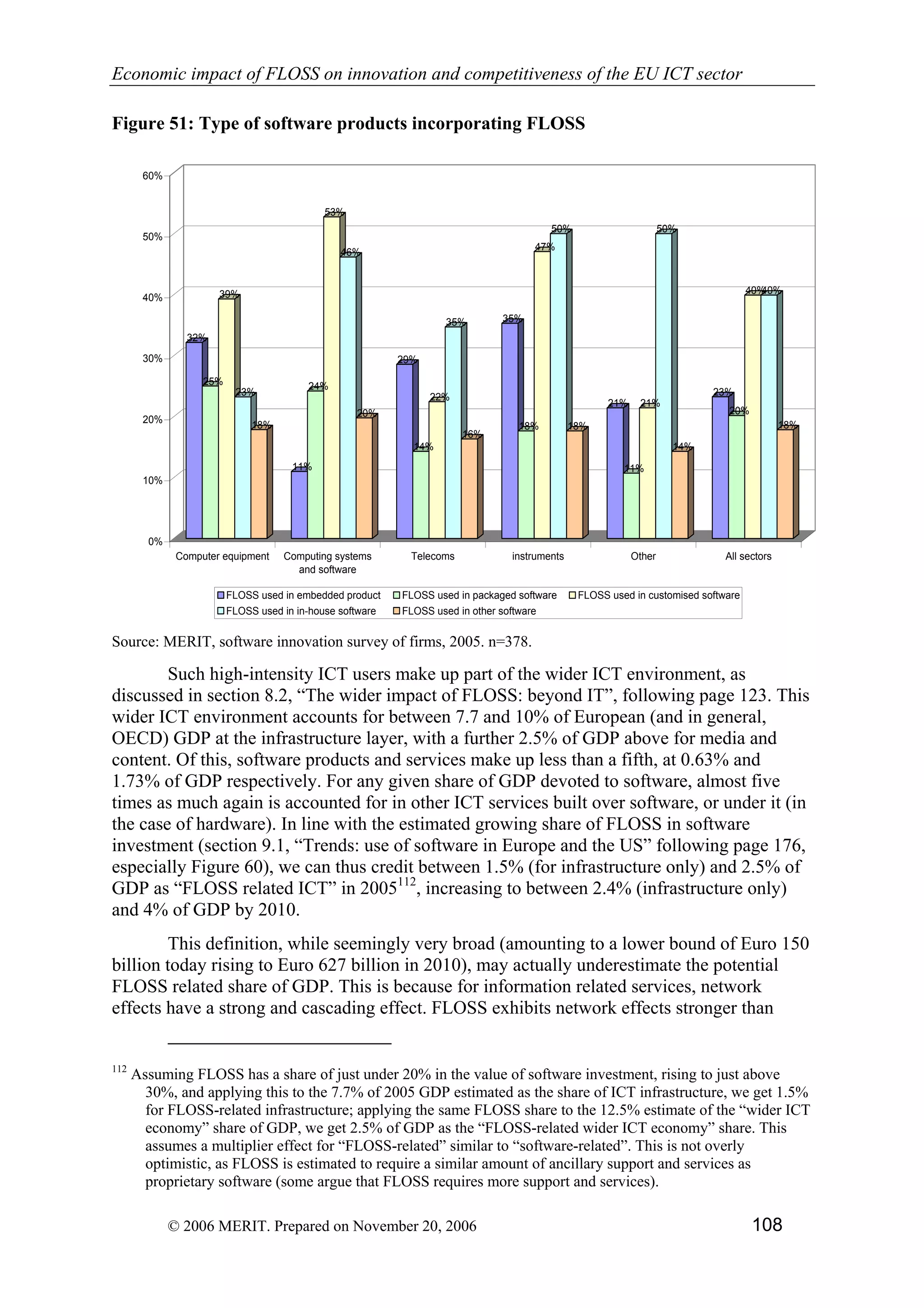

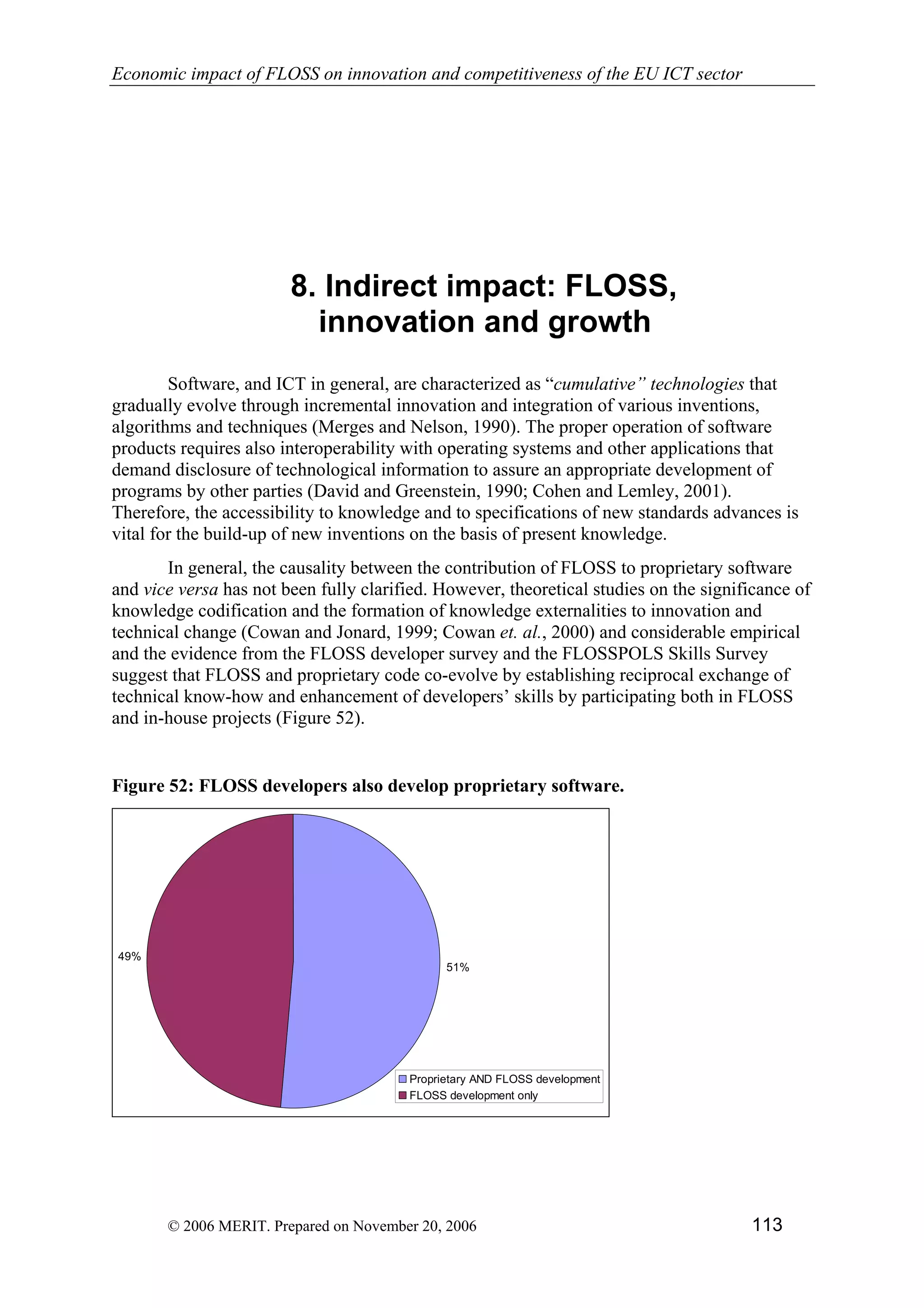

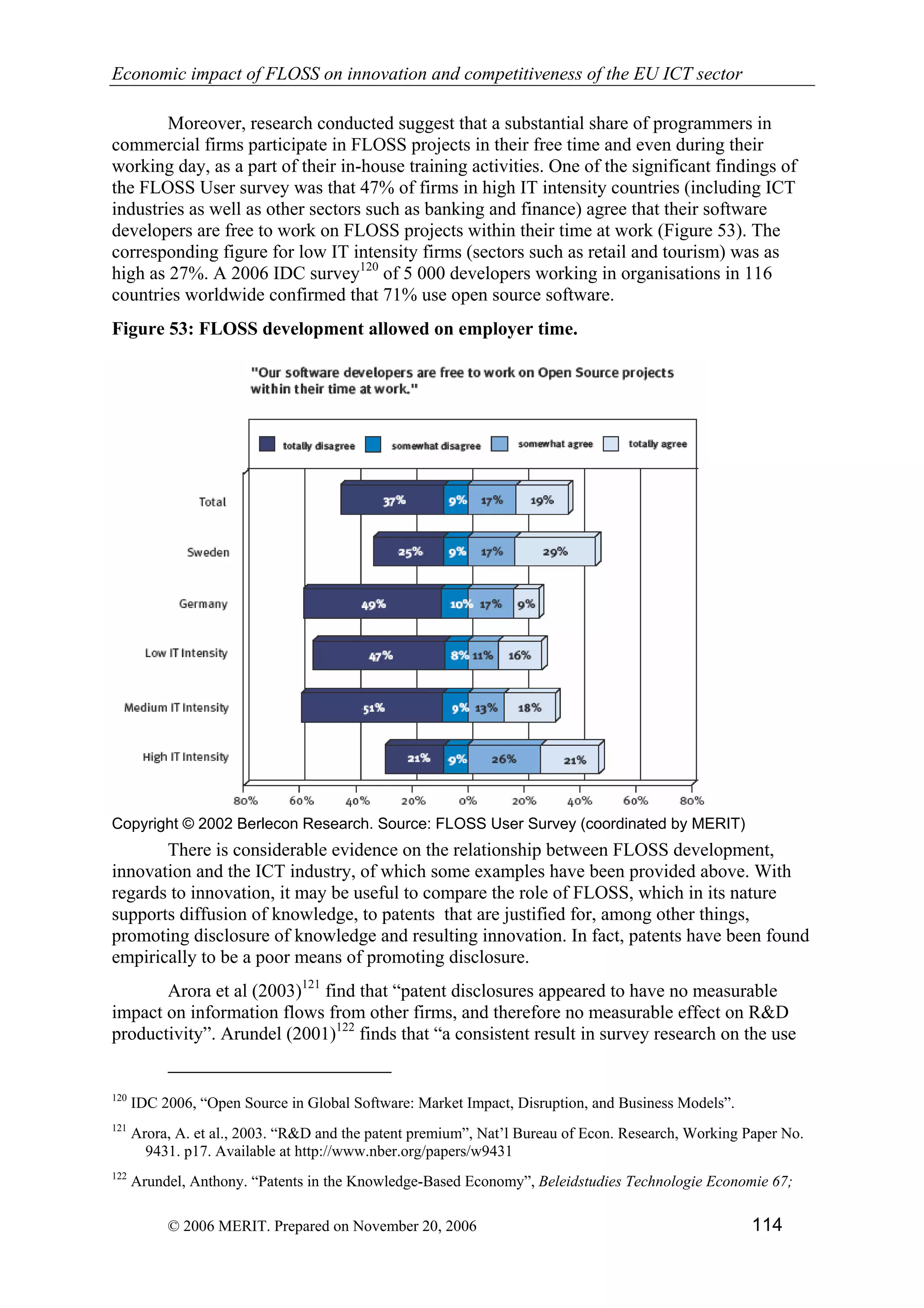

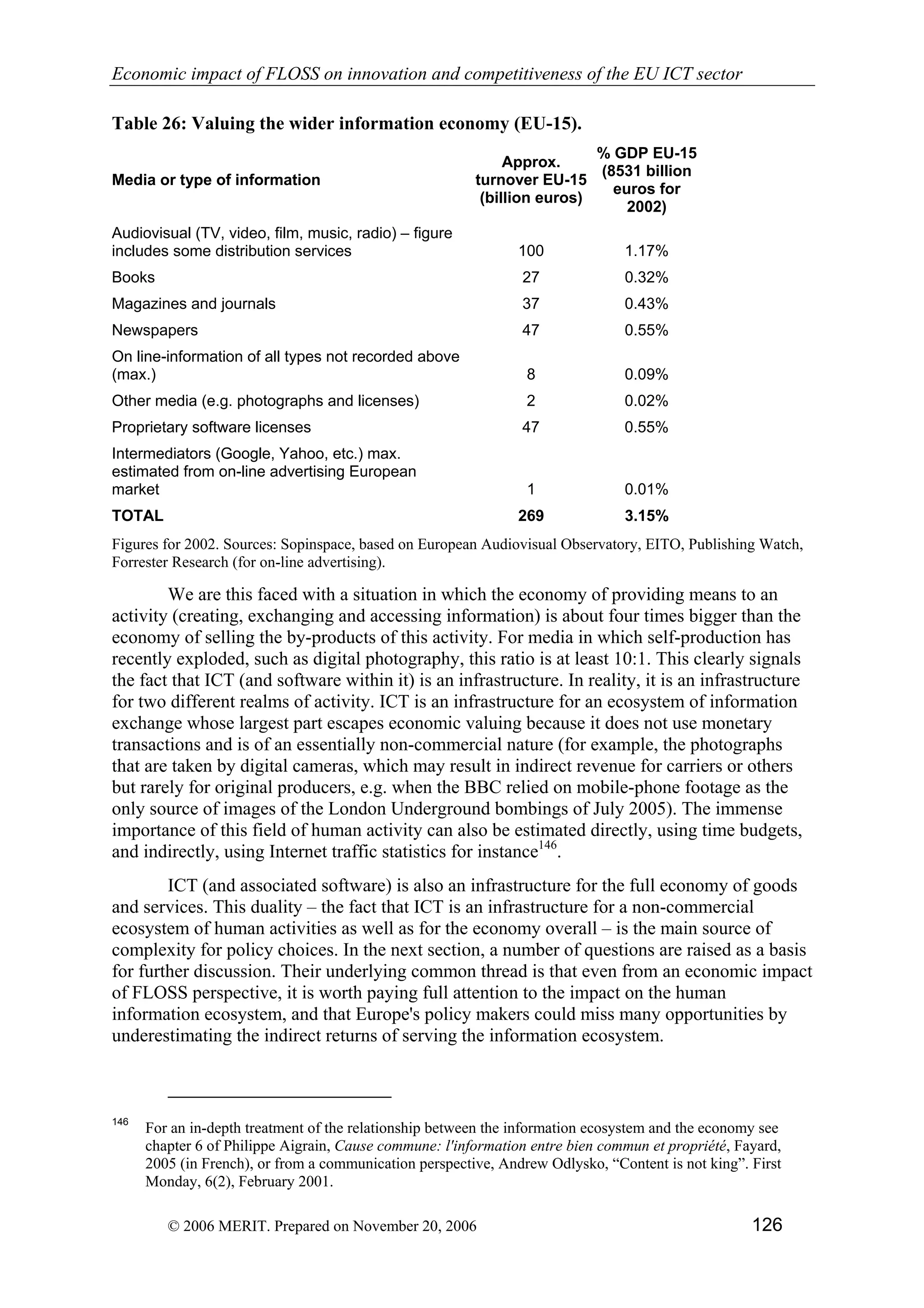

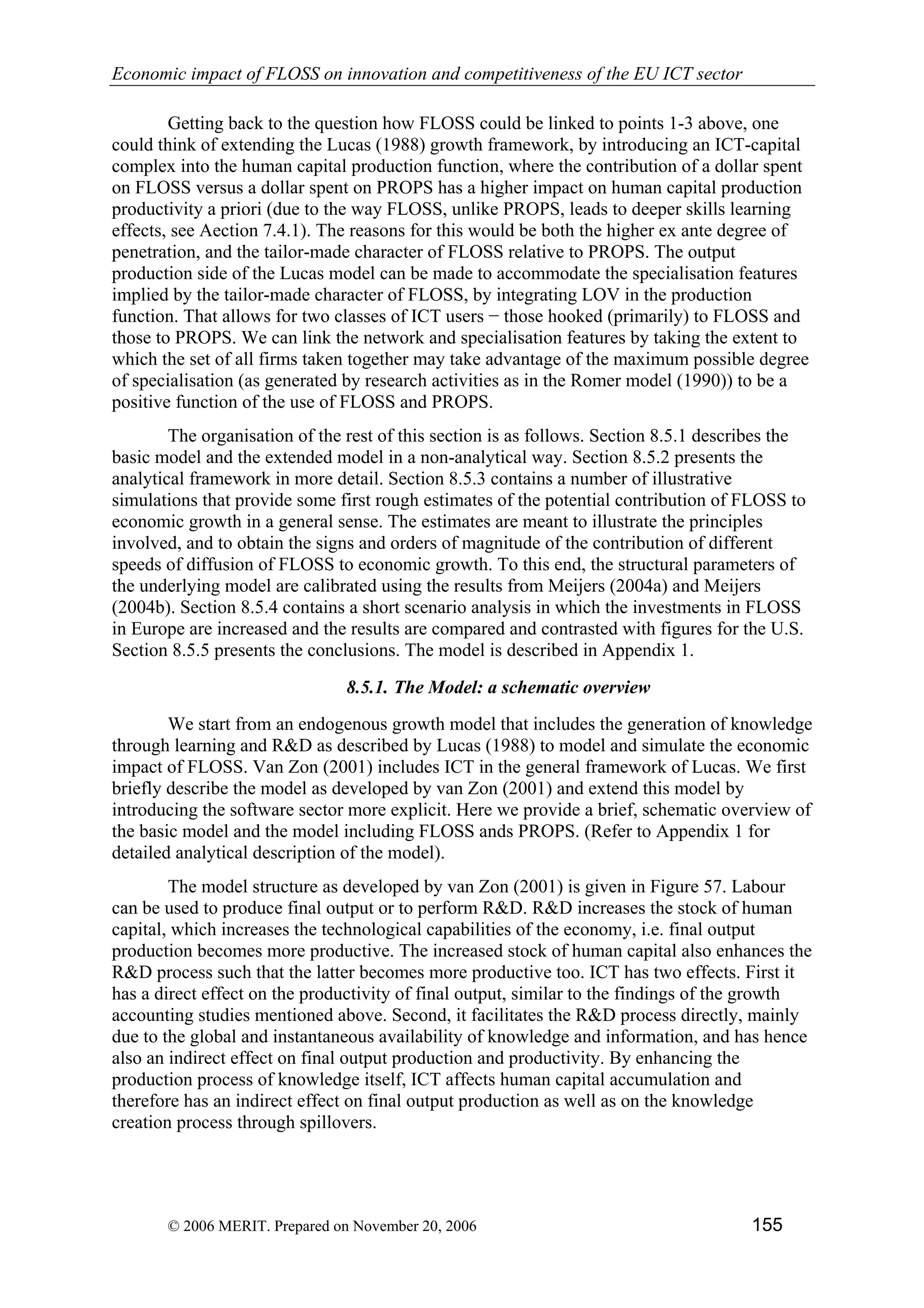

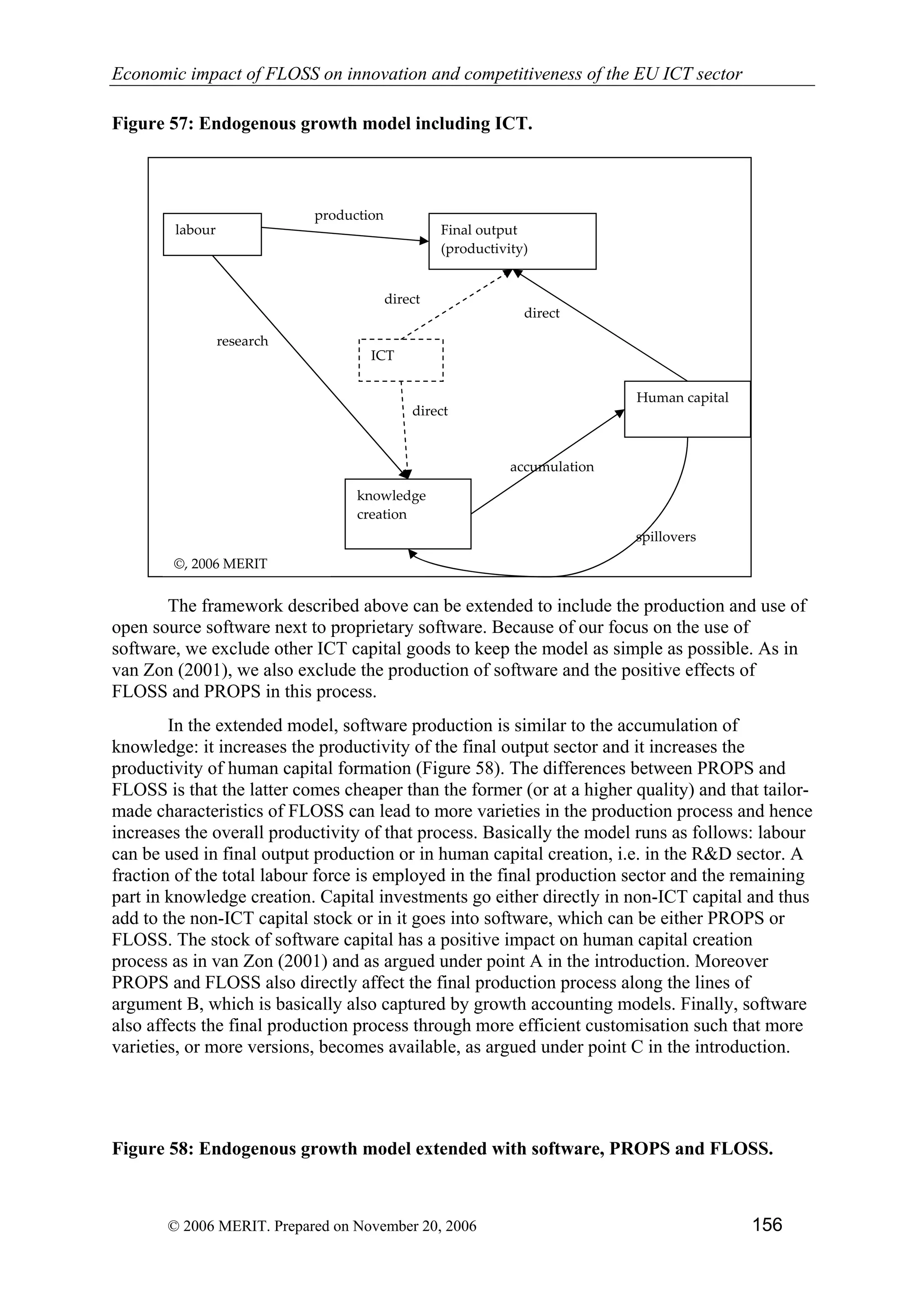

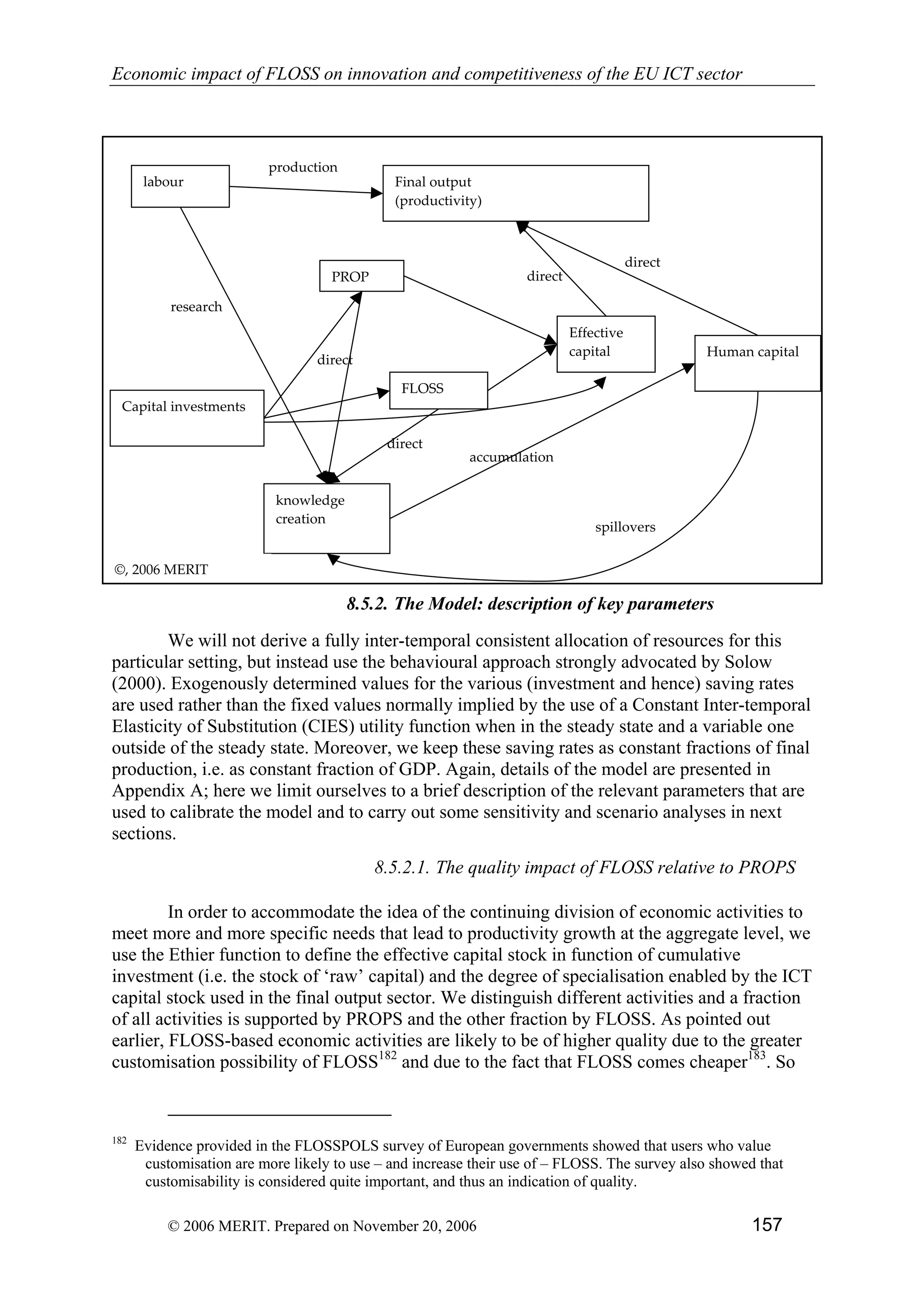

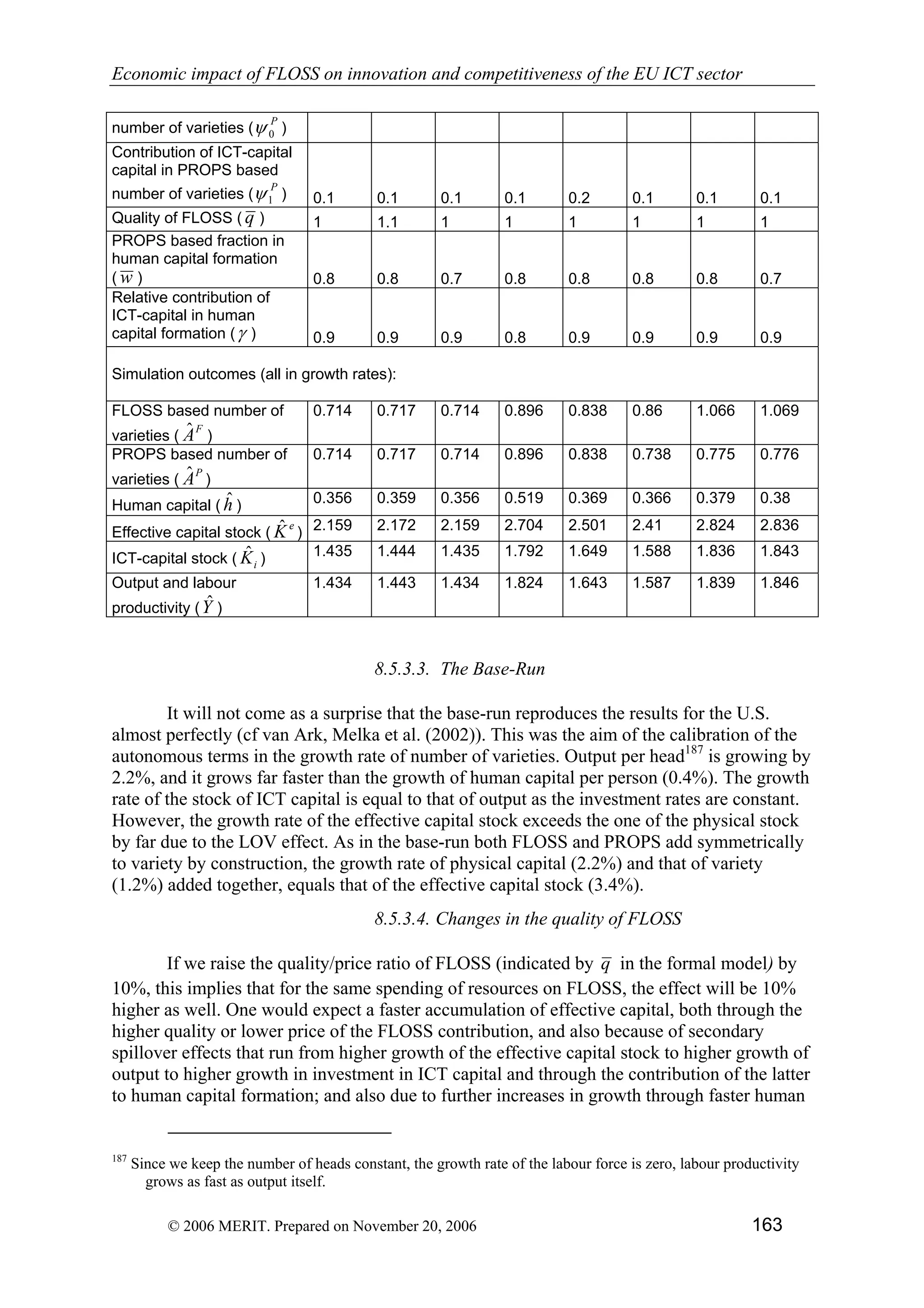

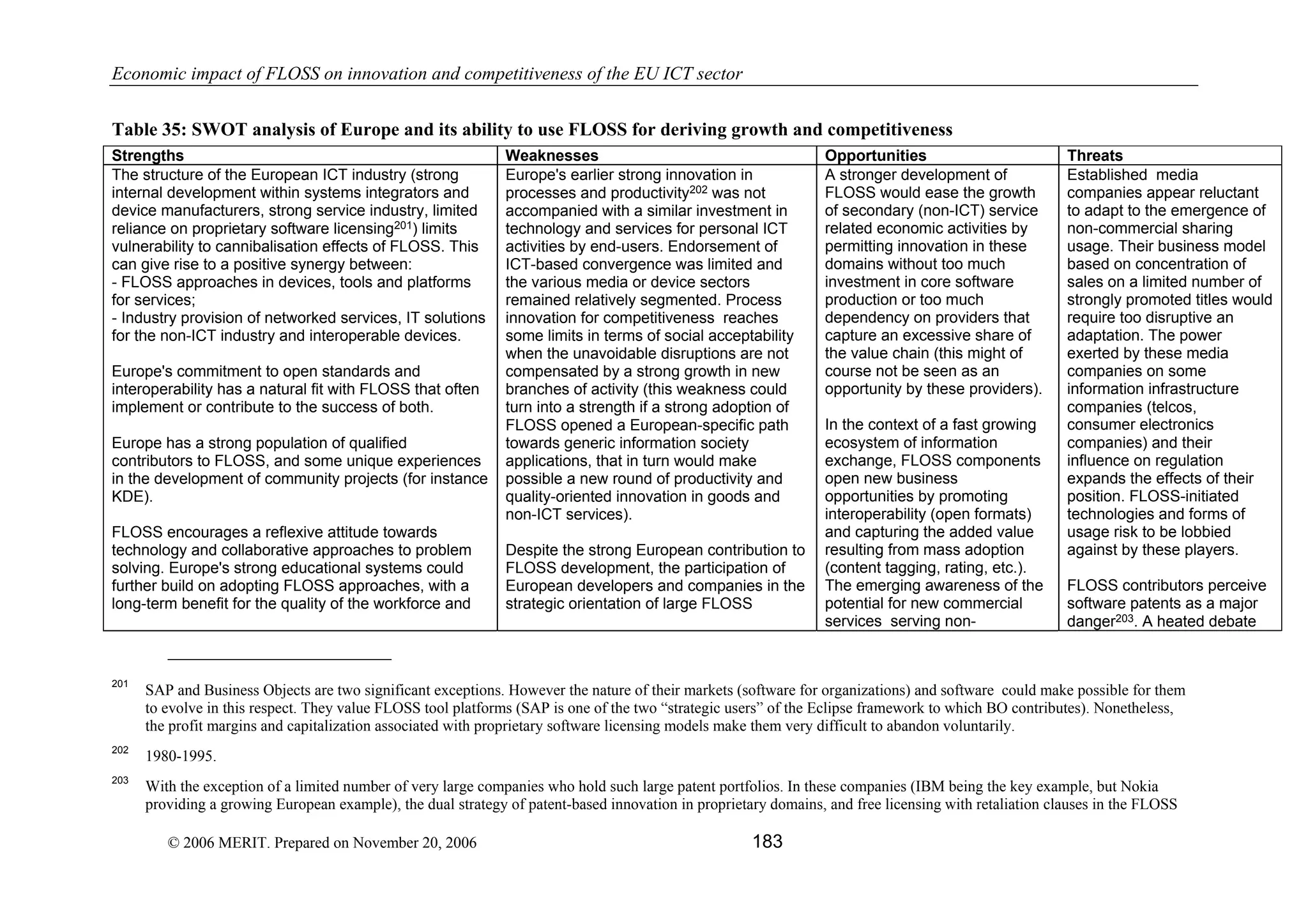

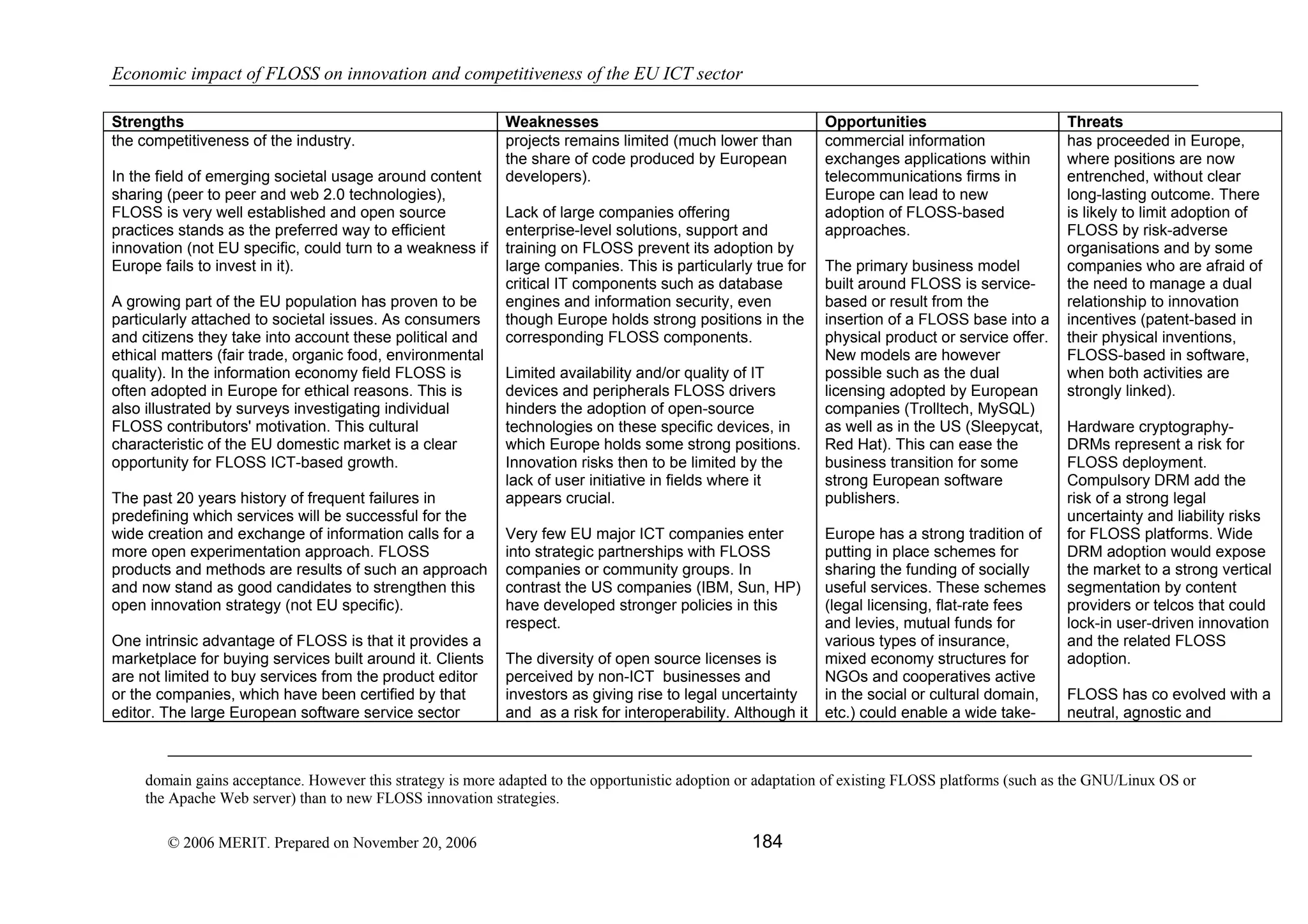

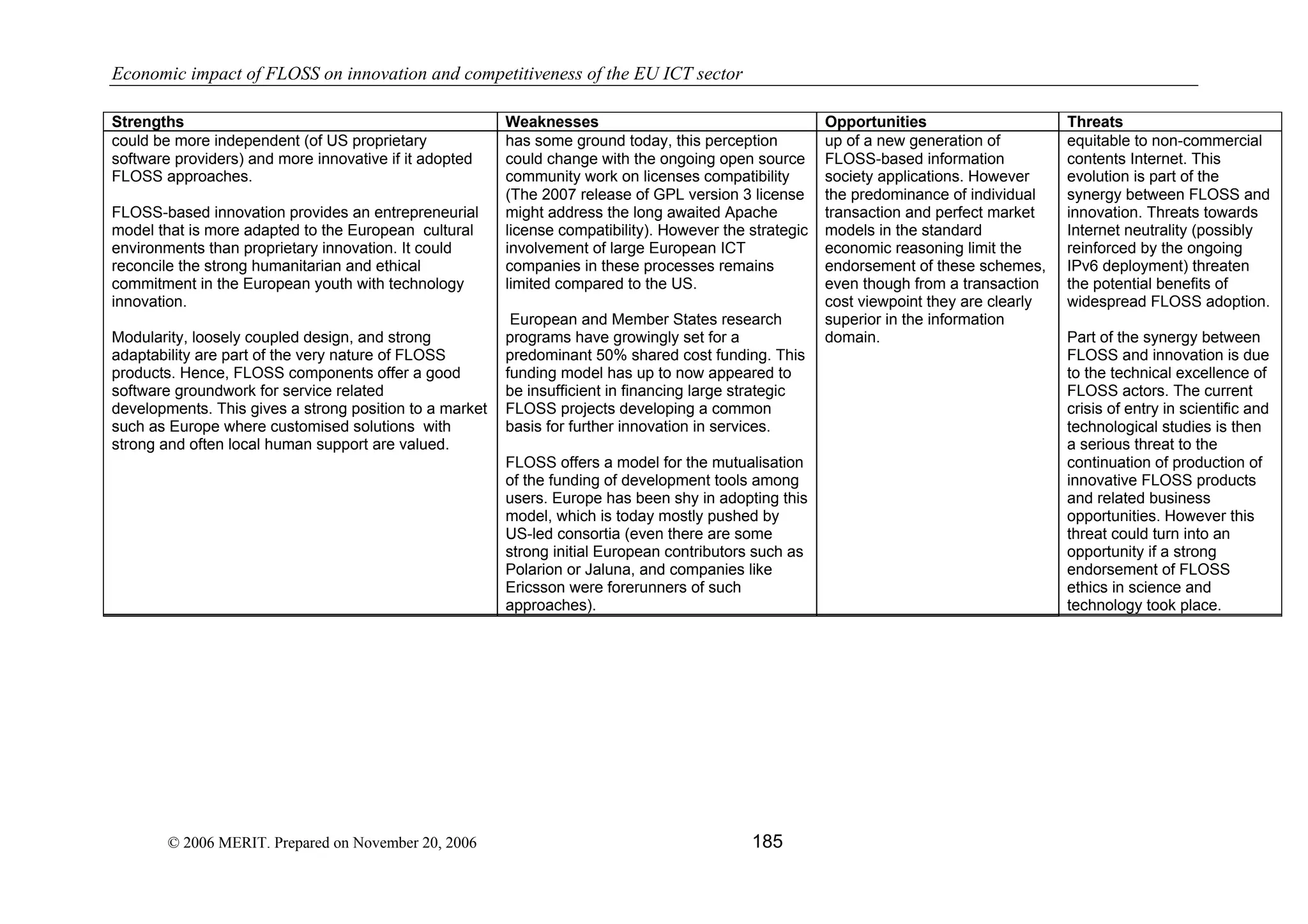

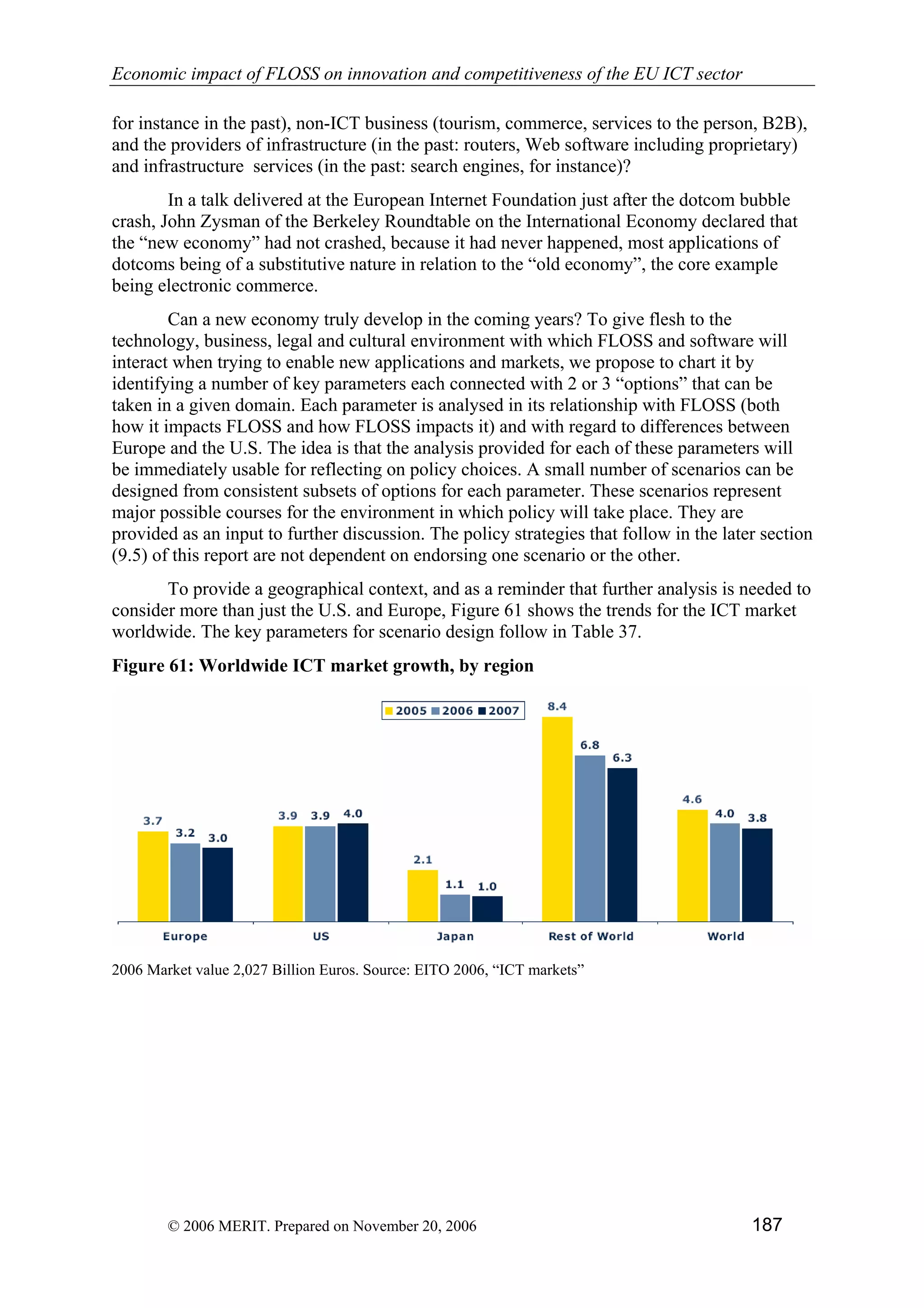

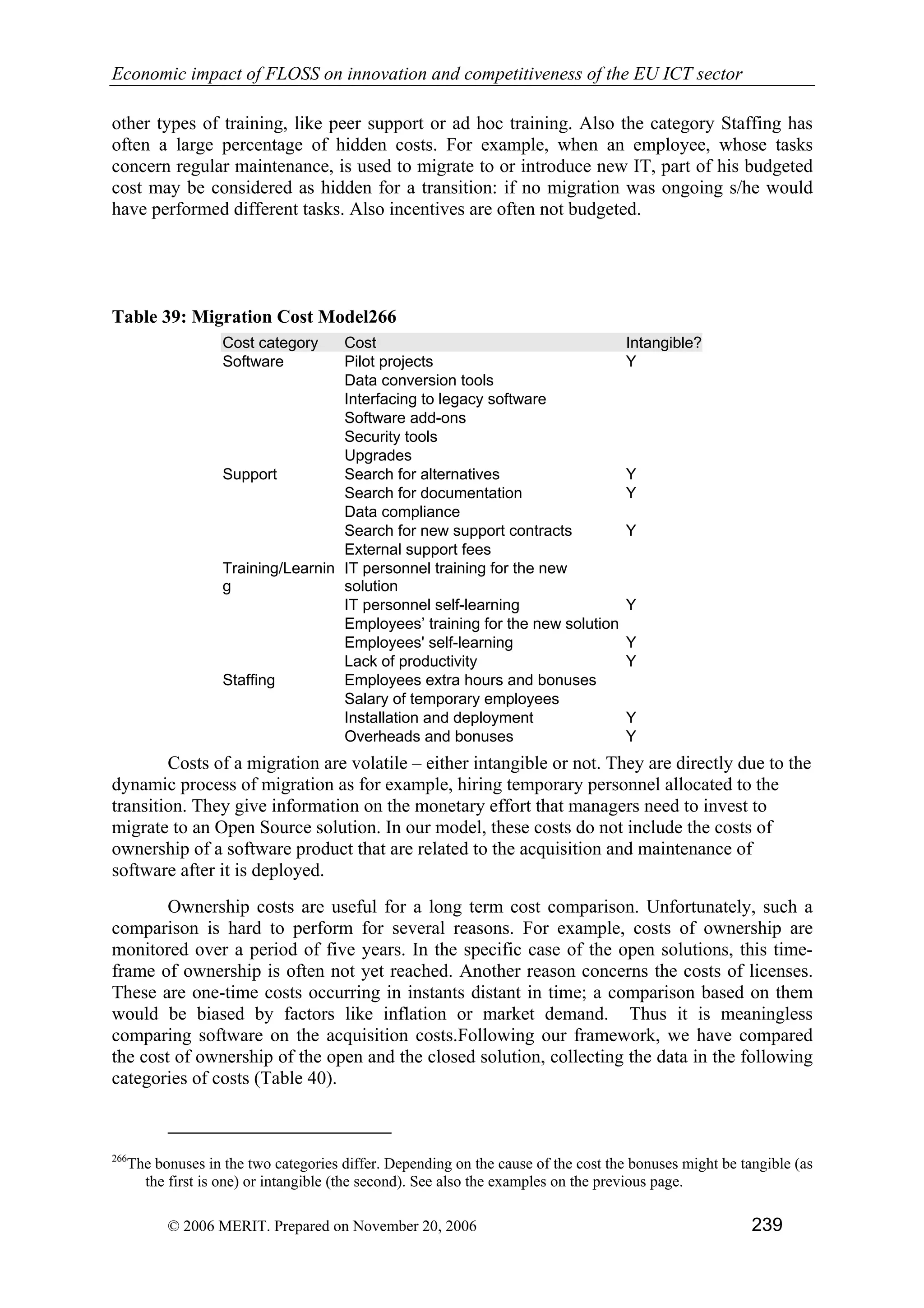

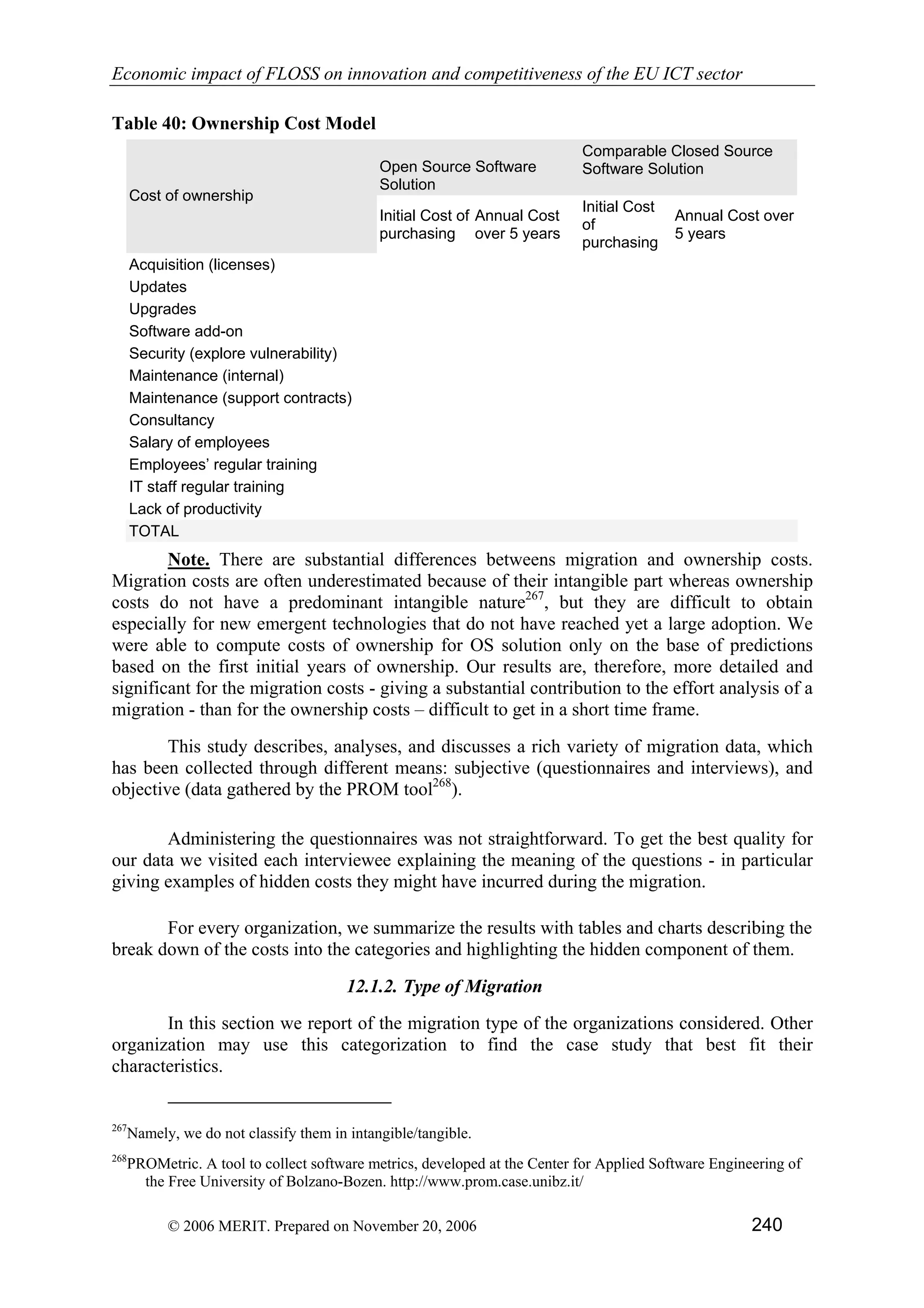

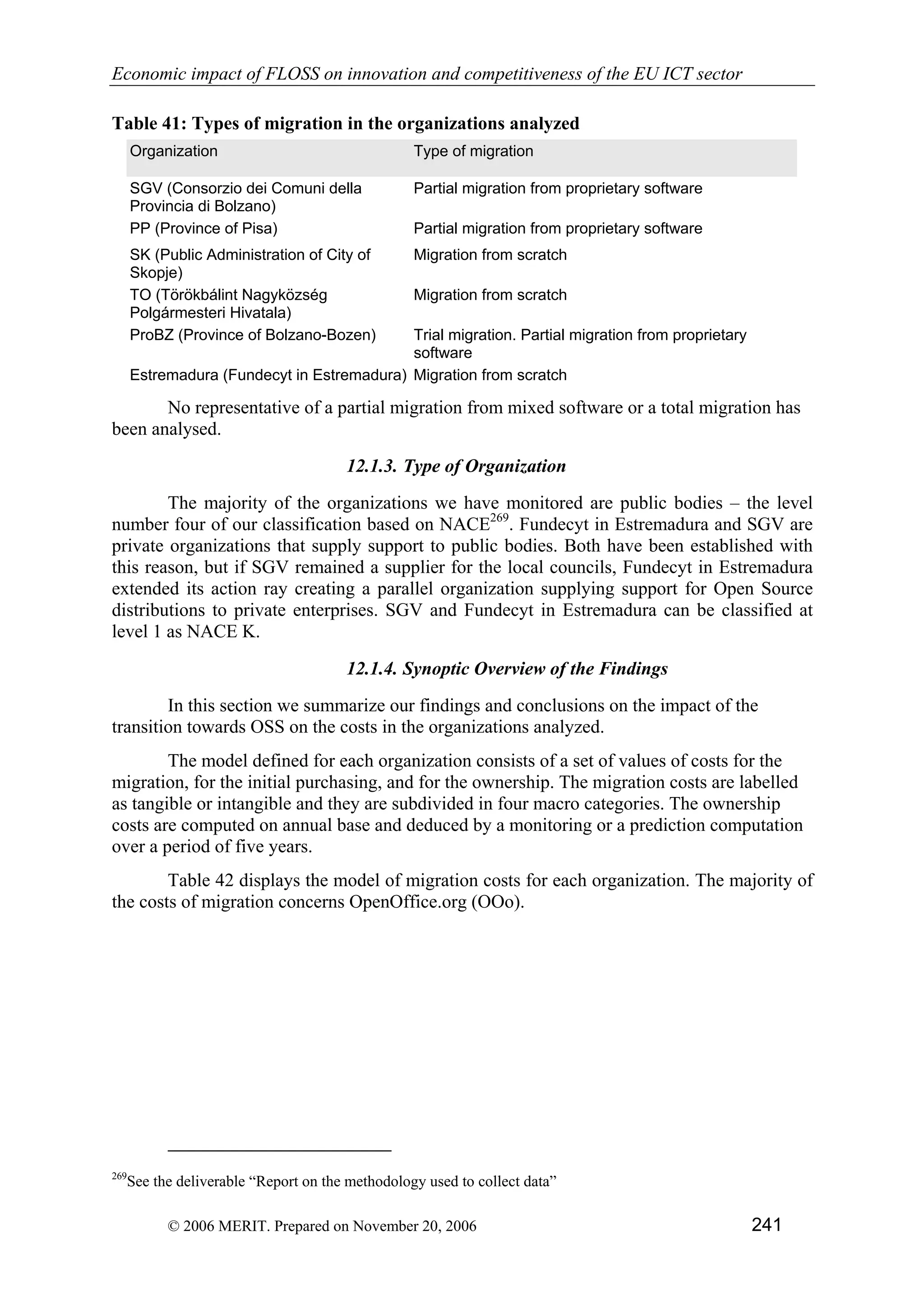

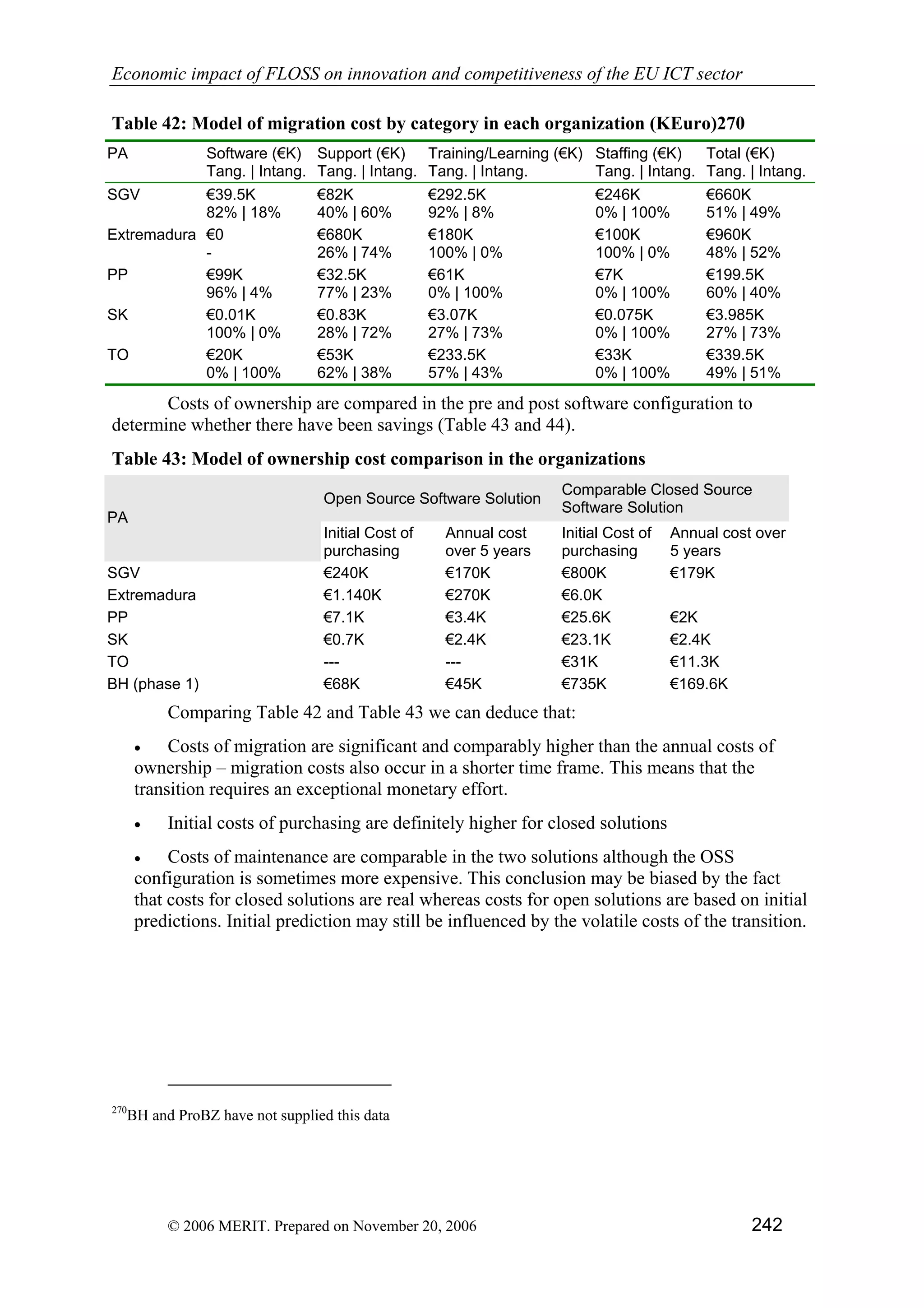

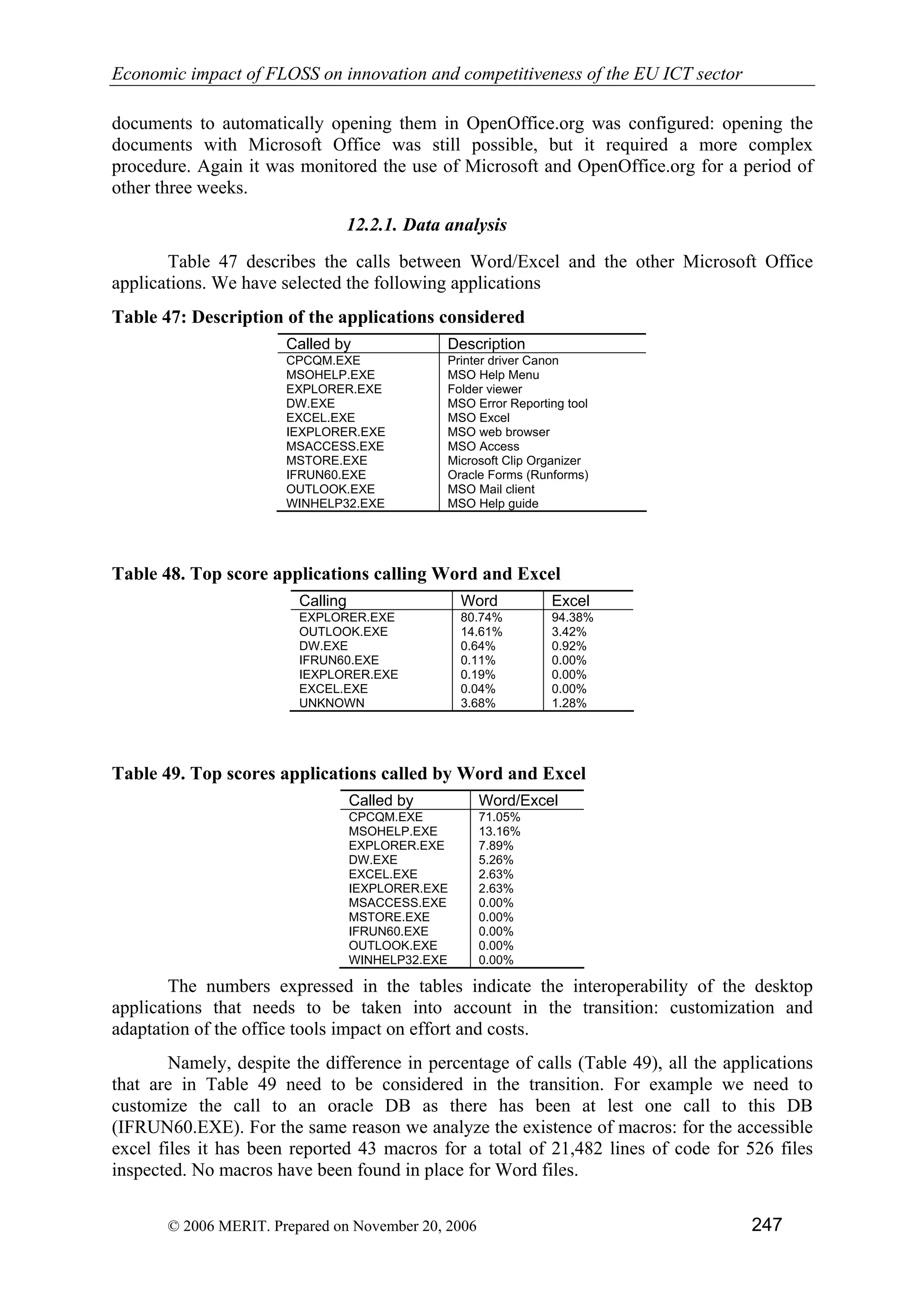

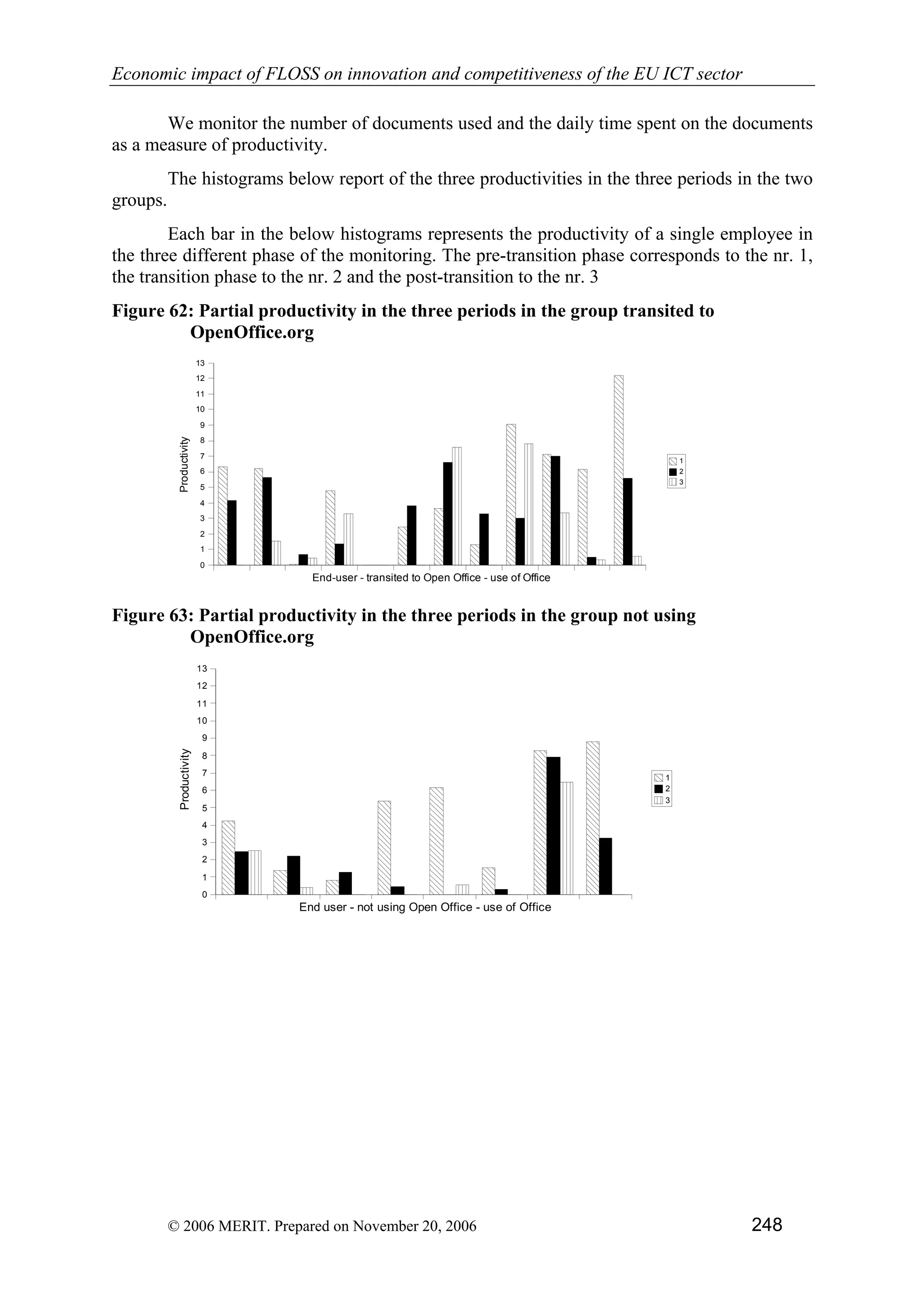

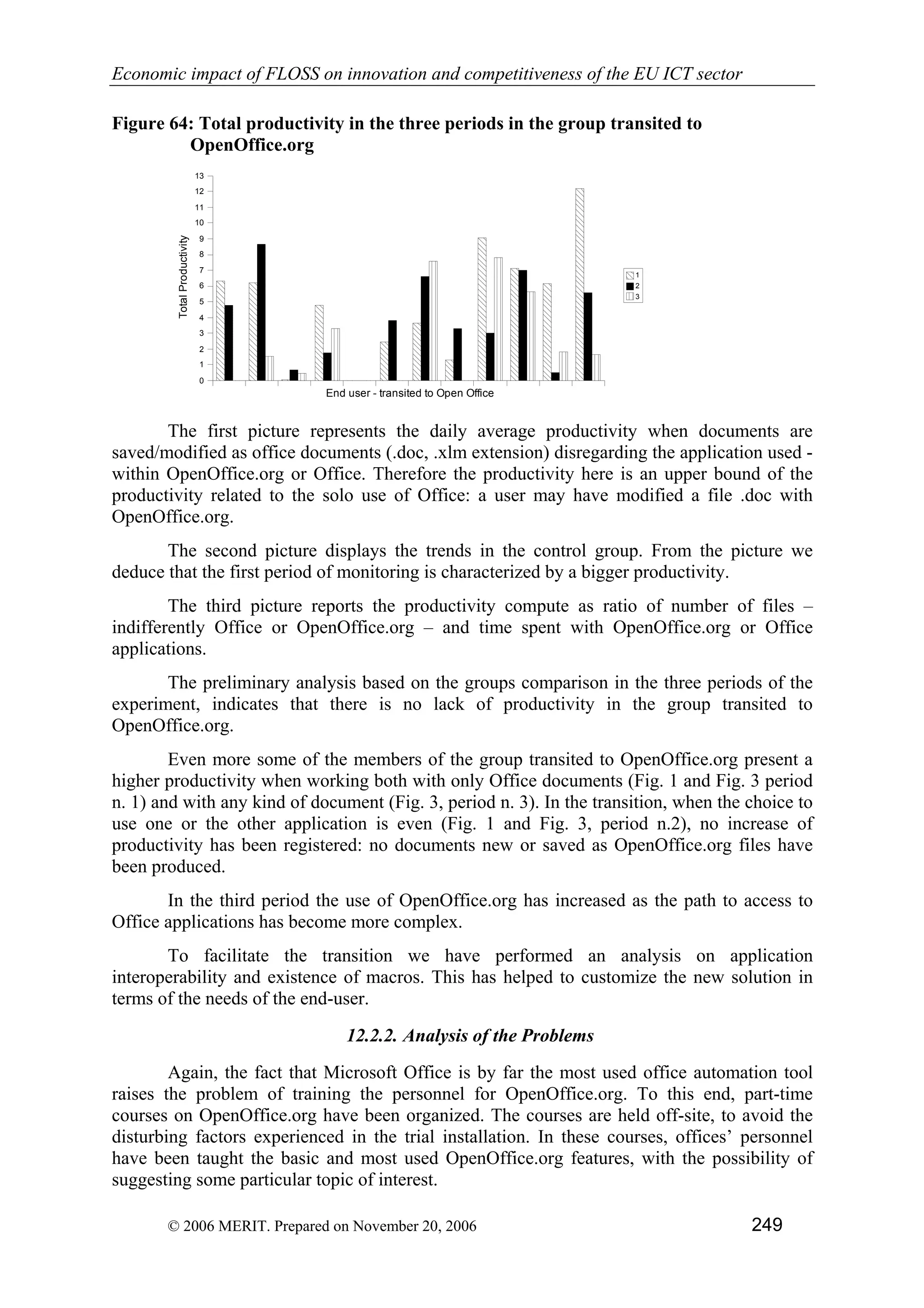

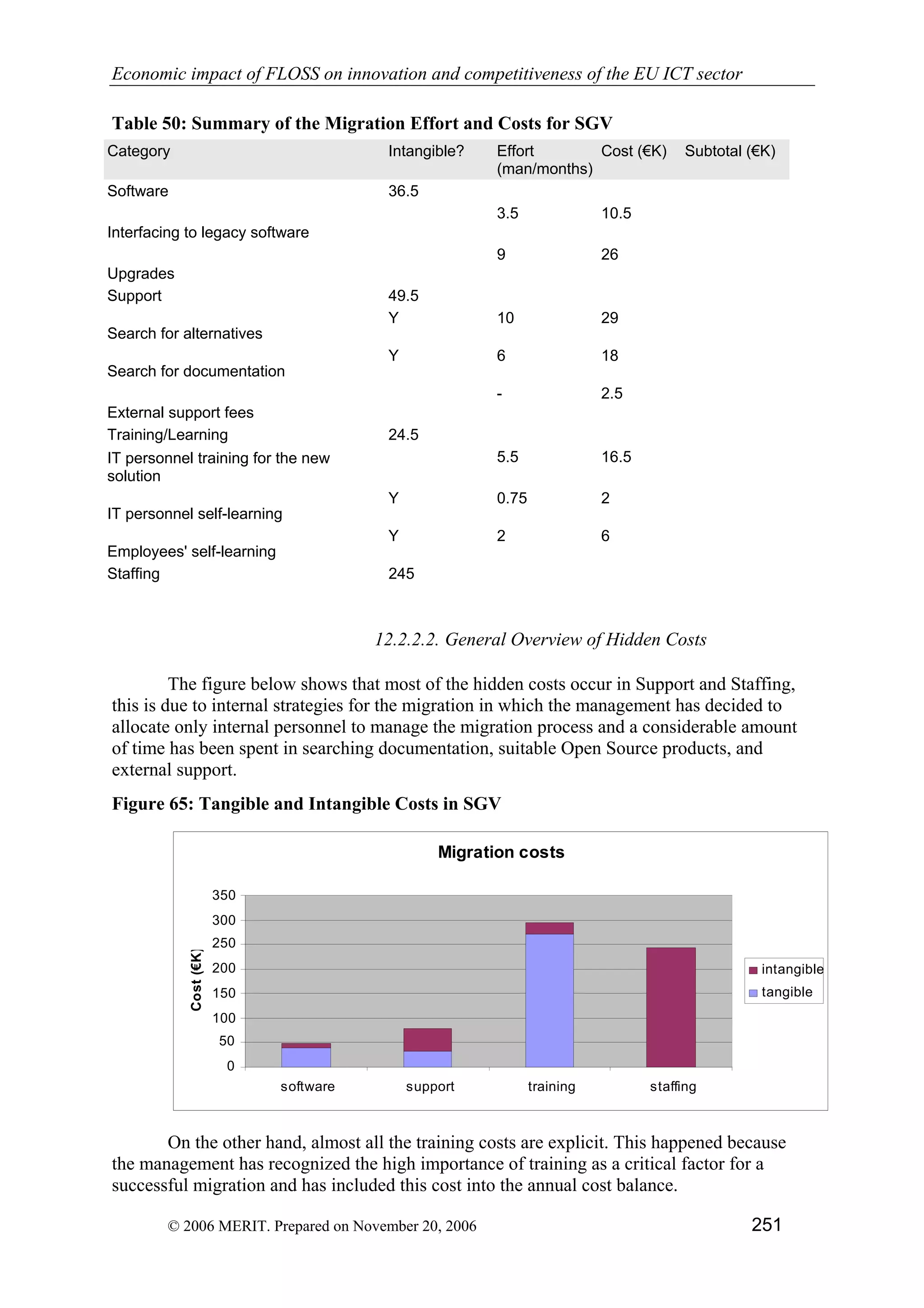

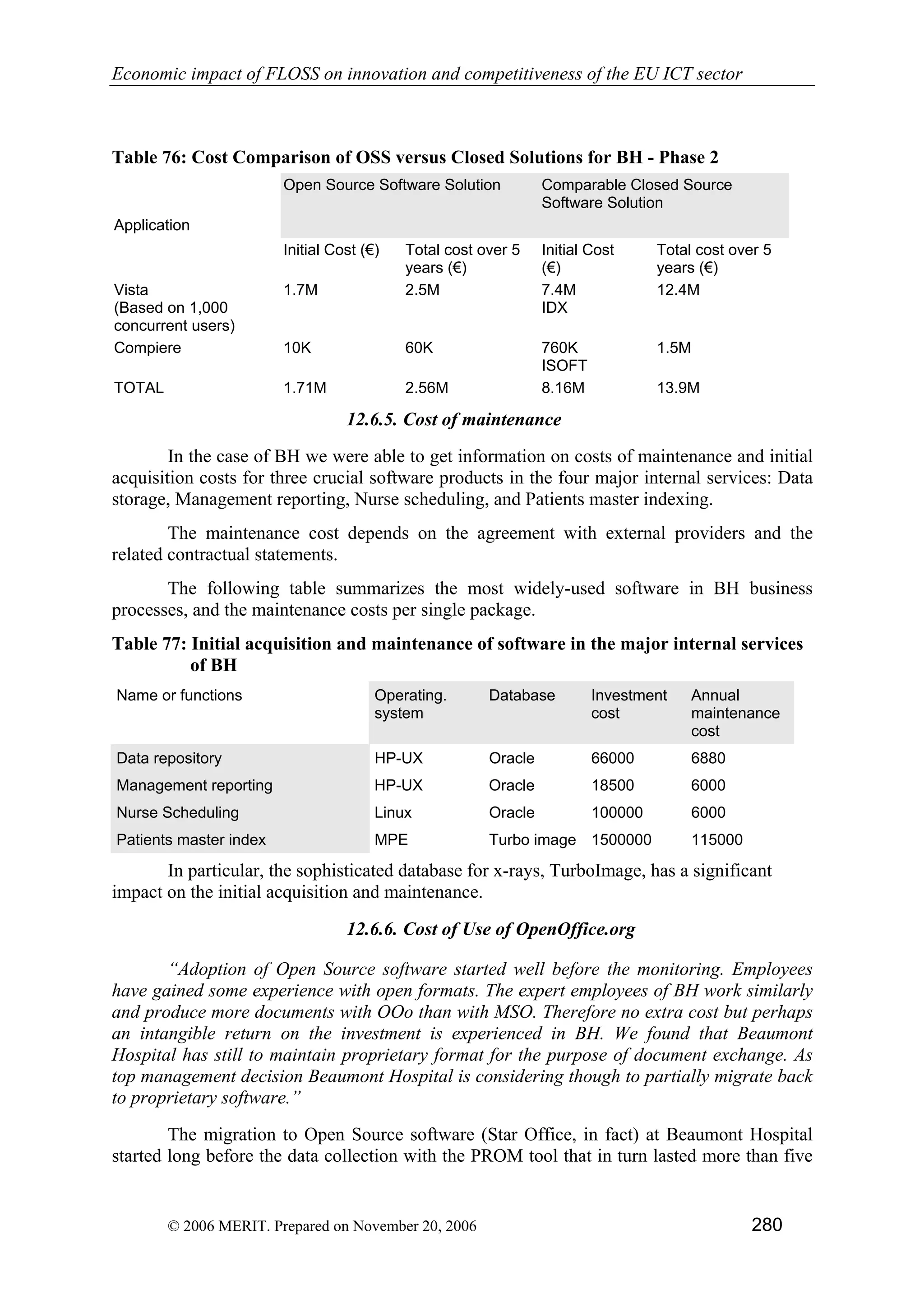

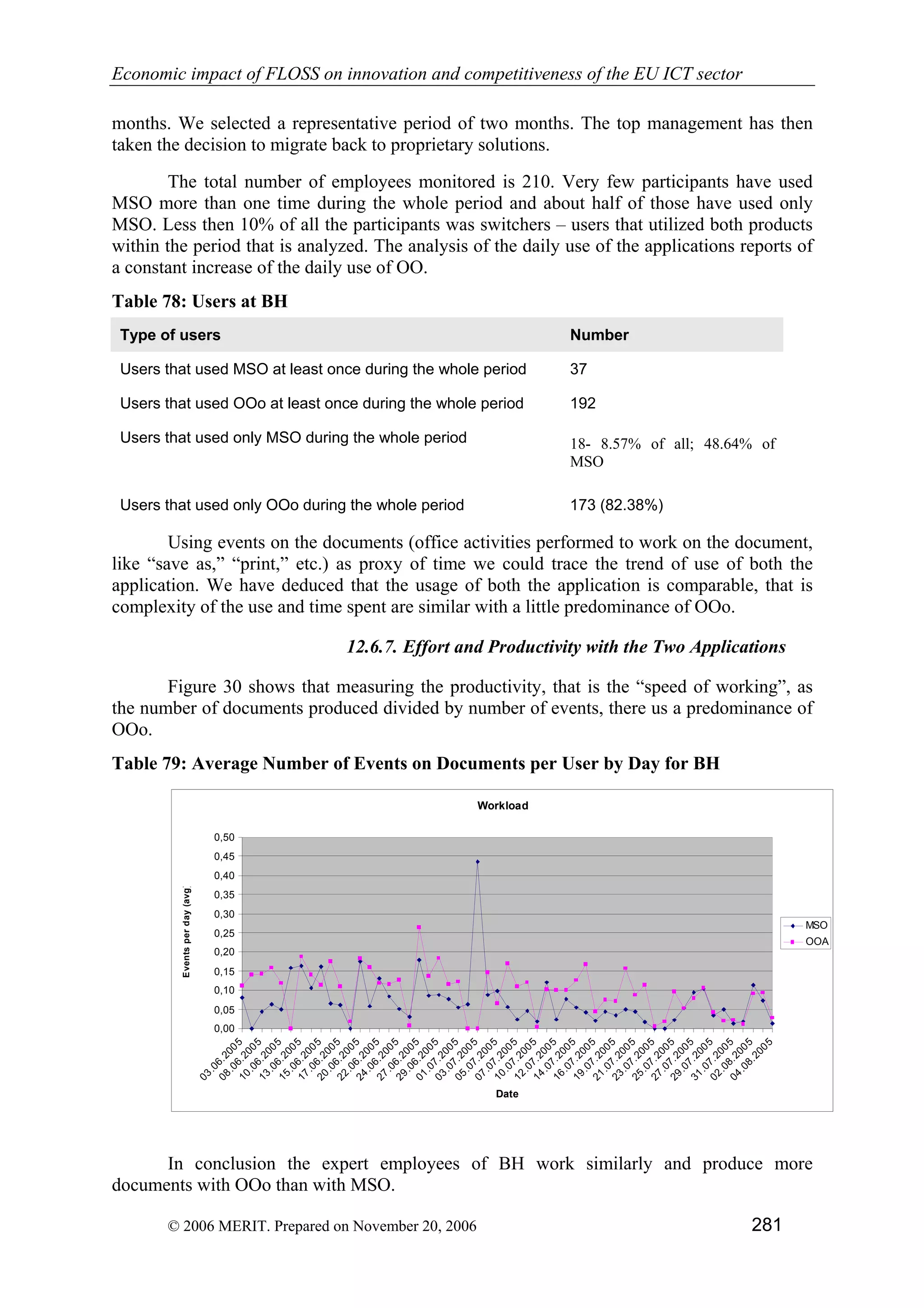

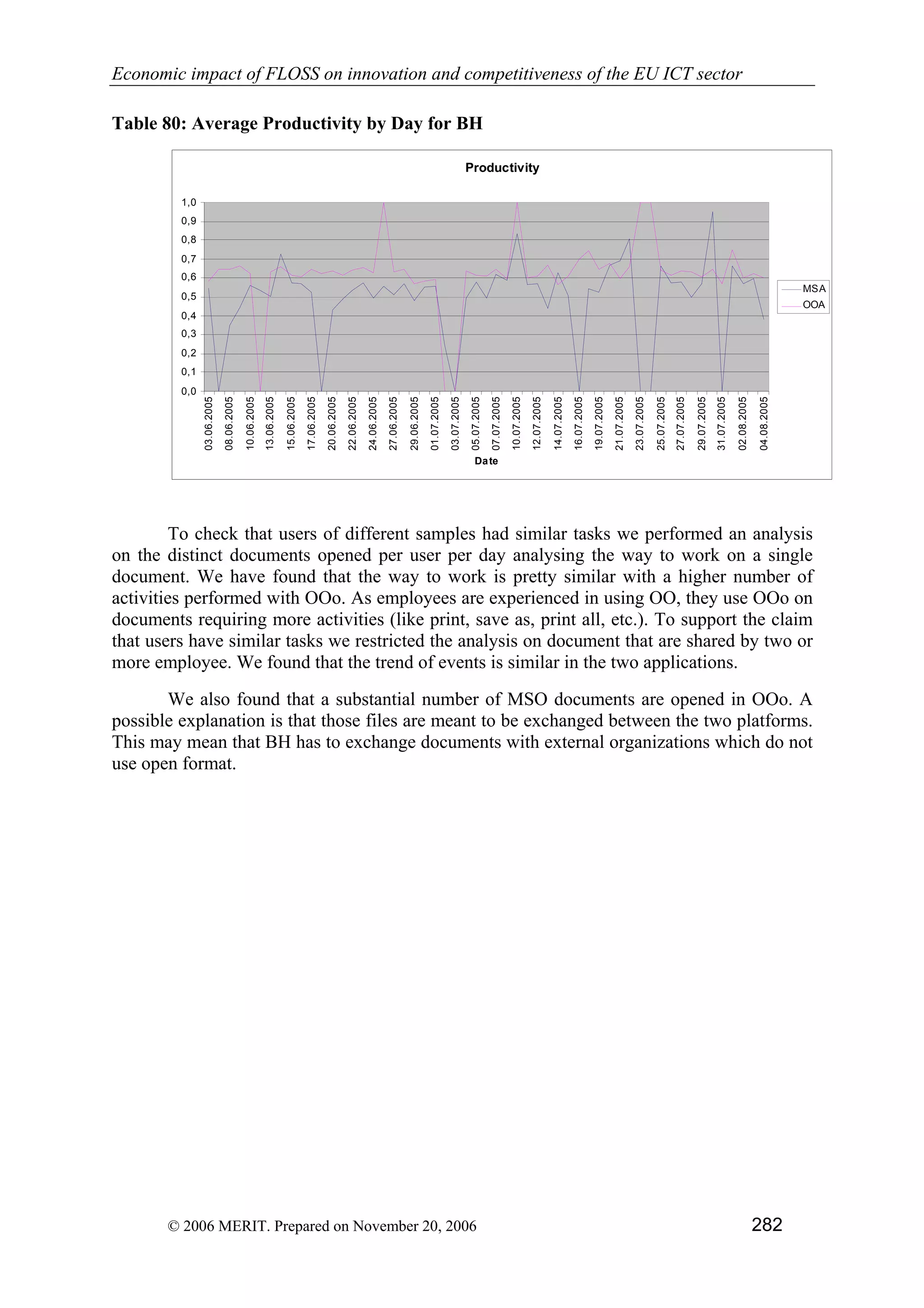

The document is a comprehensive study on the economic impact of free/libre open source software (FLOSS) on innovation and competitiveness within the EU information and communication technologies (ICT) sector. It explores direct and indirect economic effects, market penetration, and the role of FLOSS in fostering innovation, skills development, and new business models. The study also assesses trends, policy implications, and provides a SWOT analysis of the ICT industry concerning FLOSS adoption.

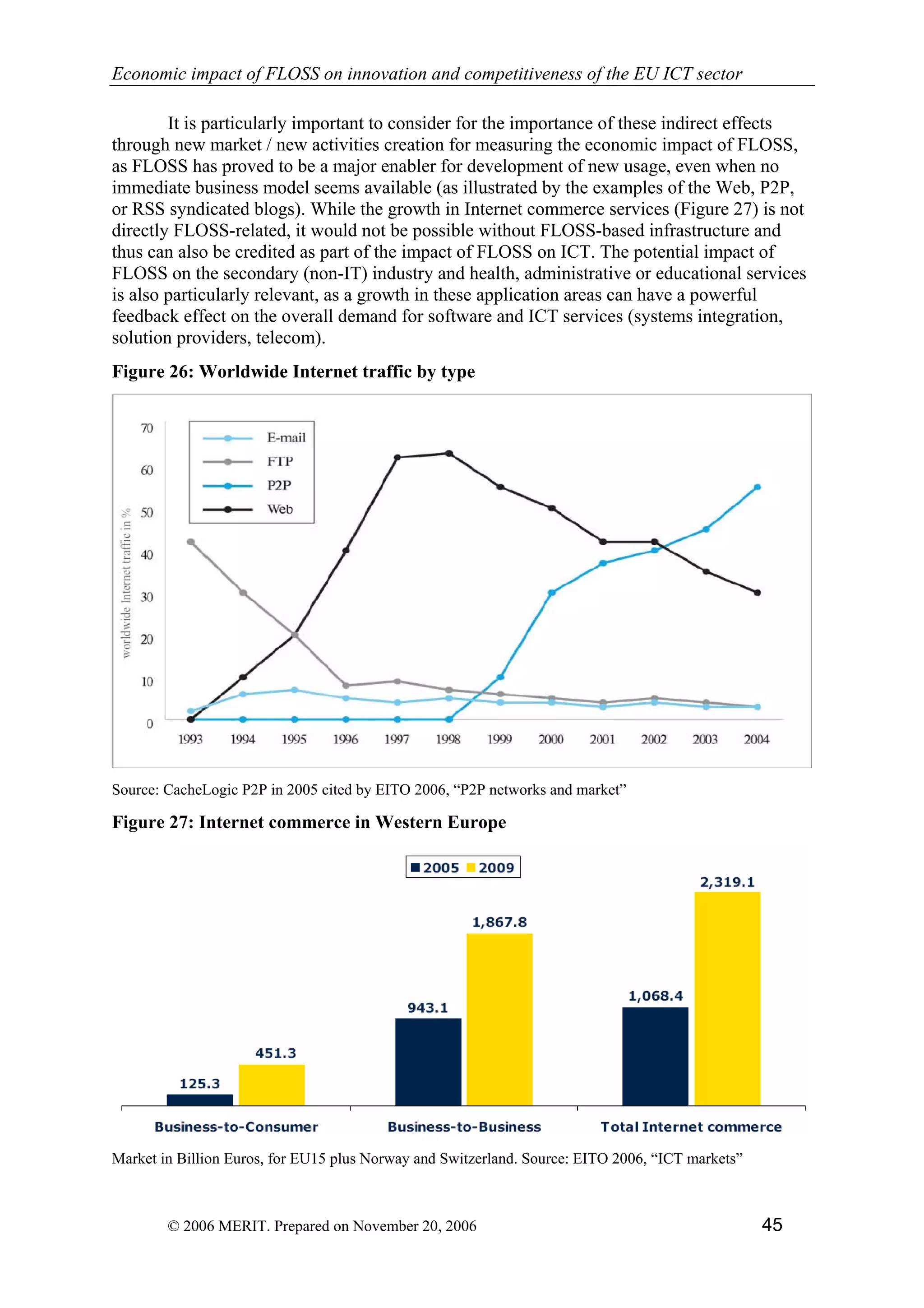

![Webinar Bm V4[1]](https://cdn.slidesharecdn.com/ss_thumbnails/webinar-bm-v41-091205142435-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)