Downloaded 41 times

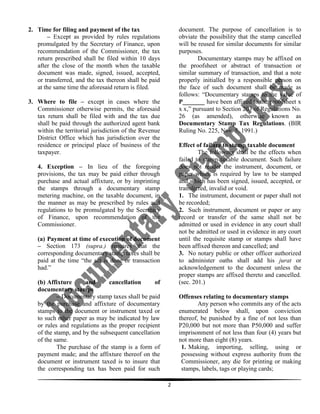

The document discusses various aspects of documentary stamp tax in the Philippines, including: 1) Persons liable for documentary stamp tax include both parties to a taxable transaction. The tax accrues when the privilege to enter the transaction is exercised, regardless of future events like cancellation. 2) The tax applies to original issues of shares and debt instruments, sales of shares, certificates of profits/interest, checks, bills of exchange, and foreign bills payable domestically. 3) Rates vary based on document type but are generally calculated per P200 (or portion thereof) of consideration, par value, actual value, or face value. For debt under 1 year, the rate is proportional to term.