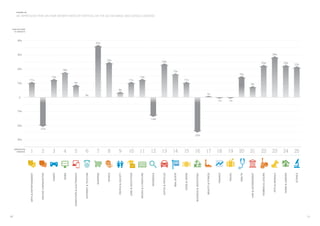

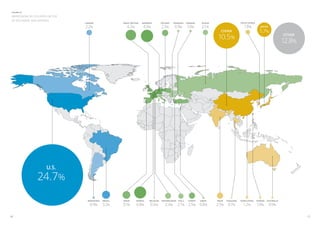

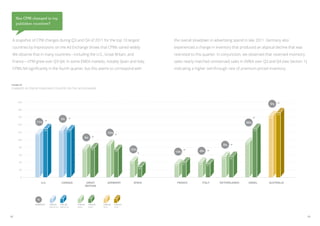

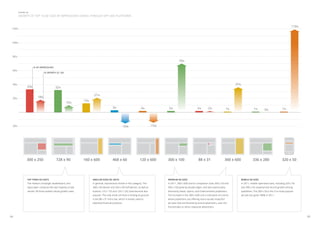

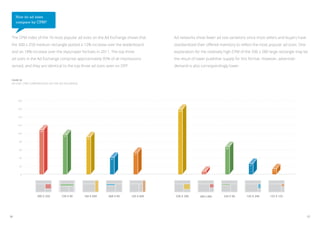

1) The document analyzes trends in the publisher display business based on data from Google publisher products. It finds that globally, unreserved impressions were higher than reserved impressions in 2011, though the gap narrowed towards the end of the year. 2) Arts & Entertainment was the top vertical by impressions and grew 11% year-over-year. Shopping and Sports also saw strong growth. The US, China, and Japan were the top countries by impressions. 3) CPMs varied widely by country, with some like the US and UK seeing growth from Q3 to Q4 2011 while others like Spain and Italy declined.