Download as PDF, PPTX

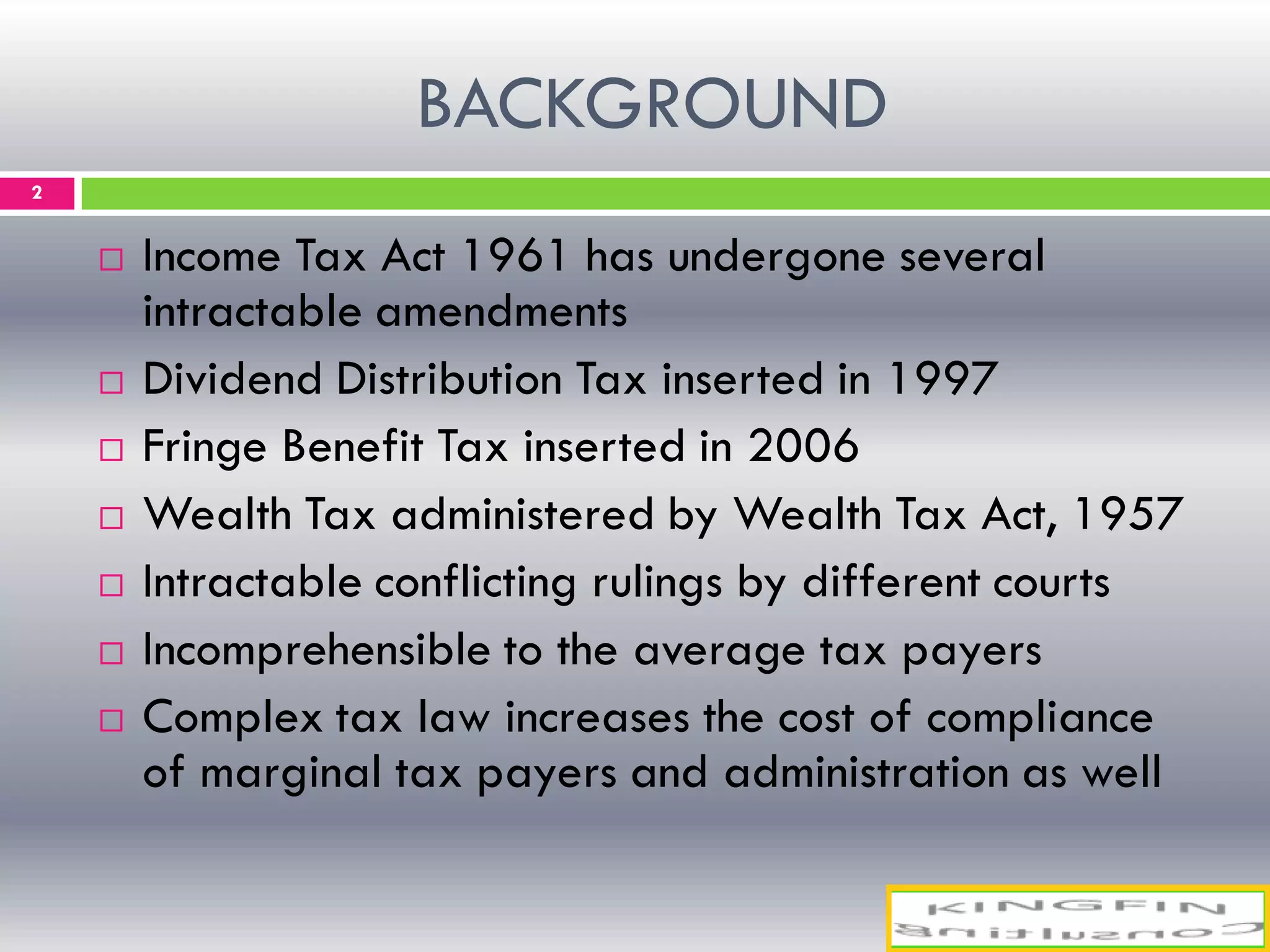

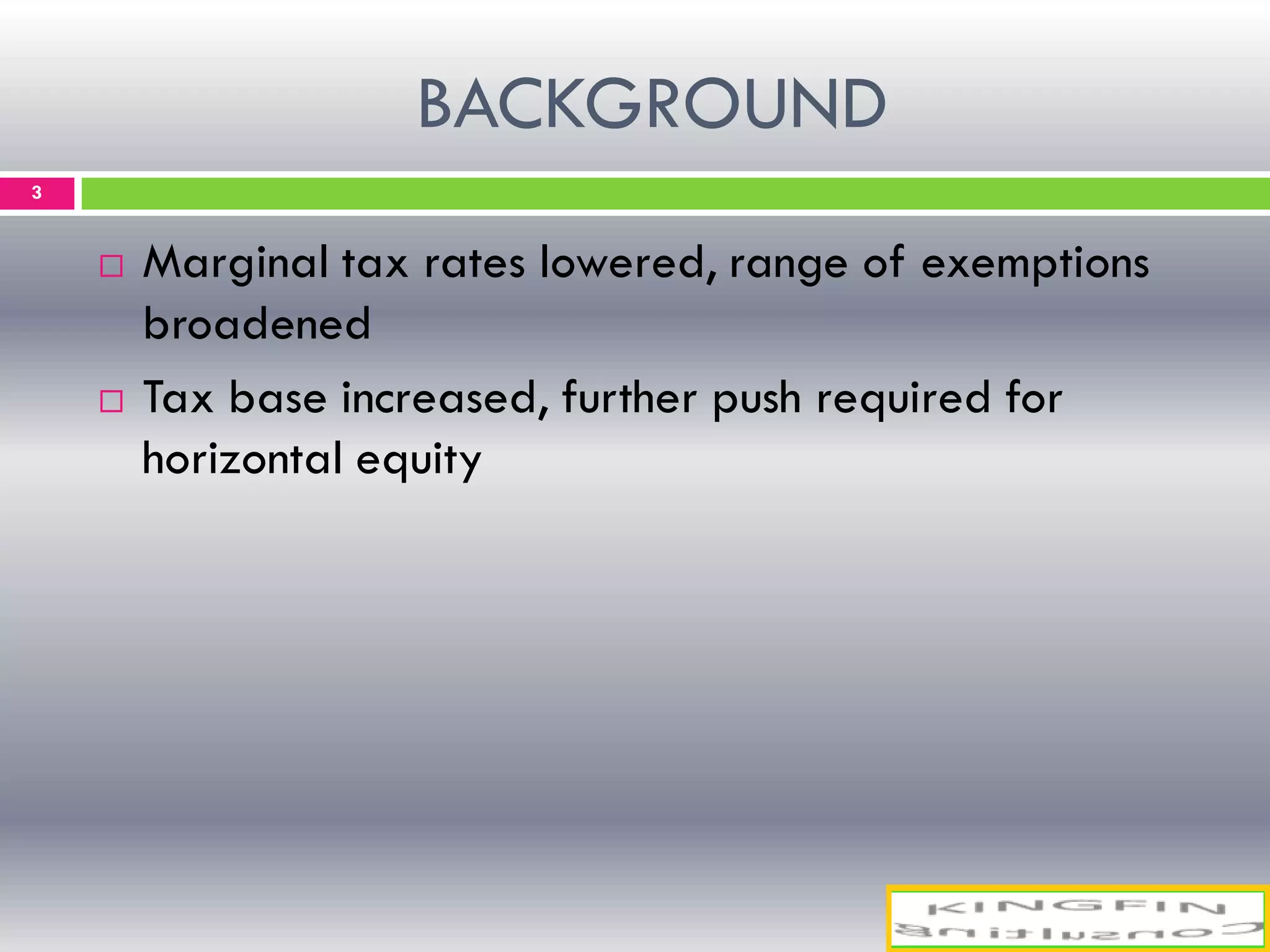

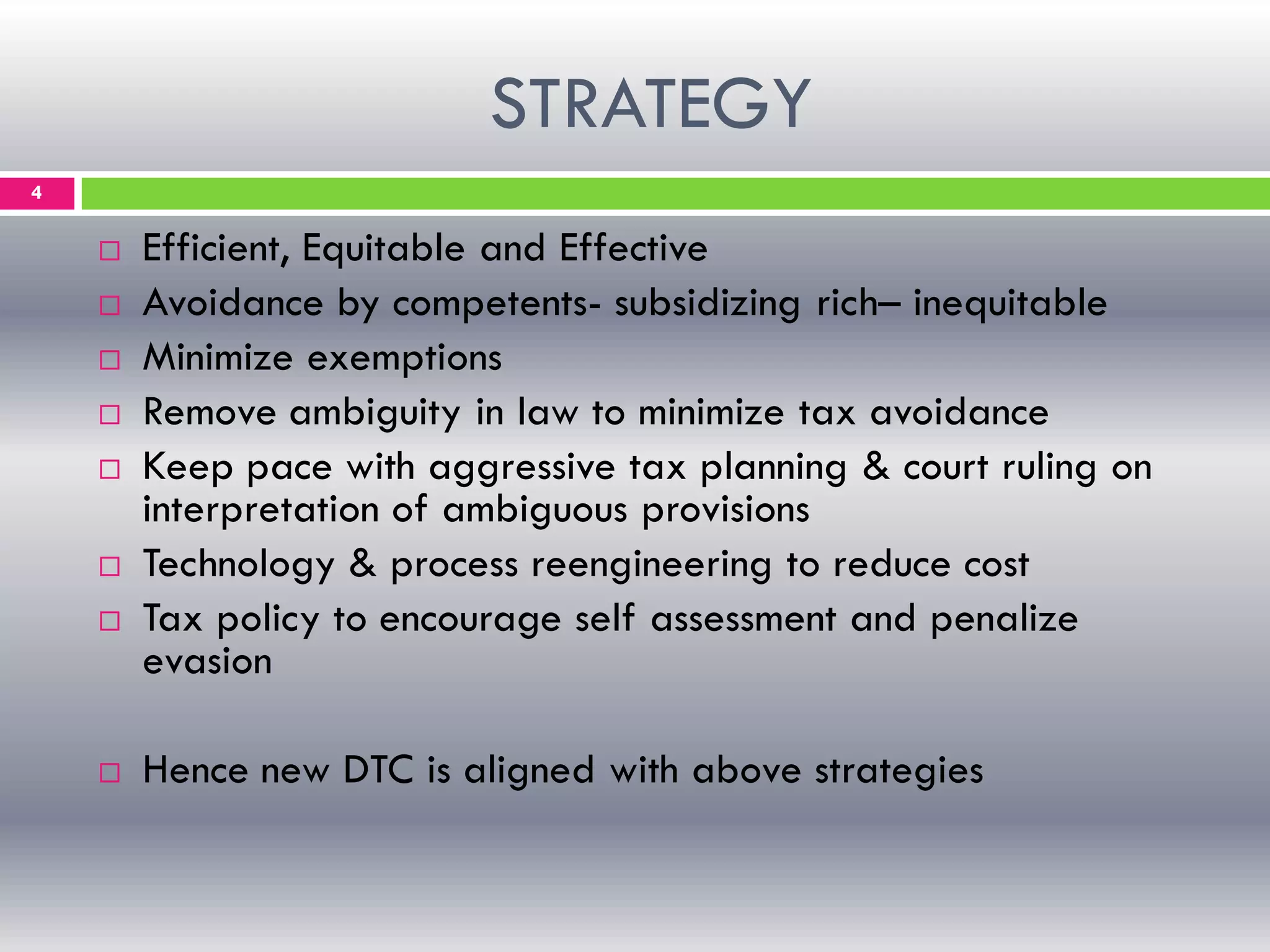

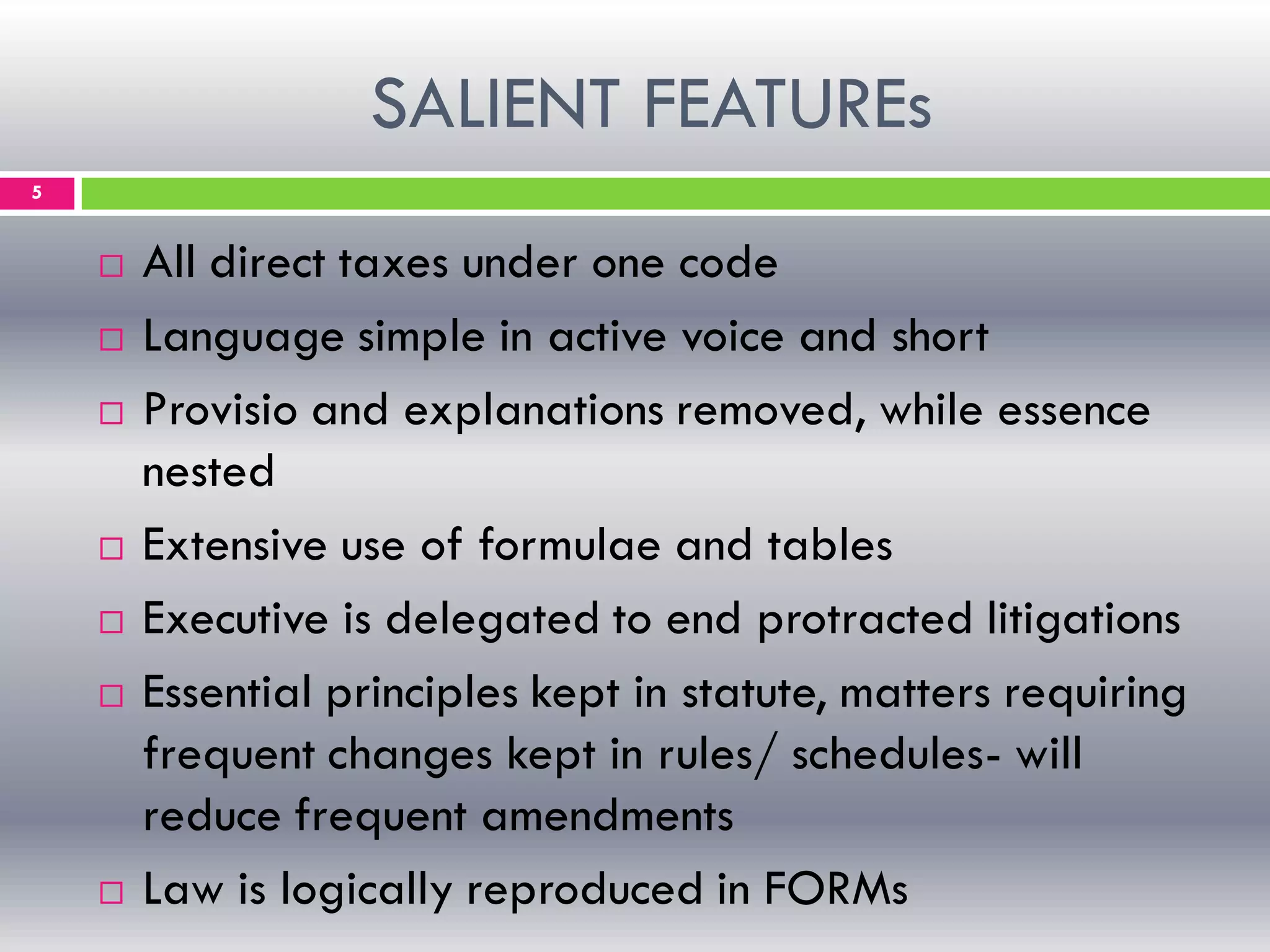

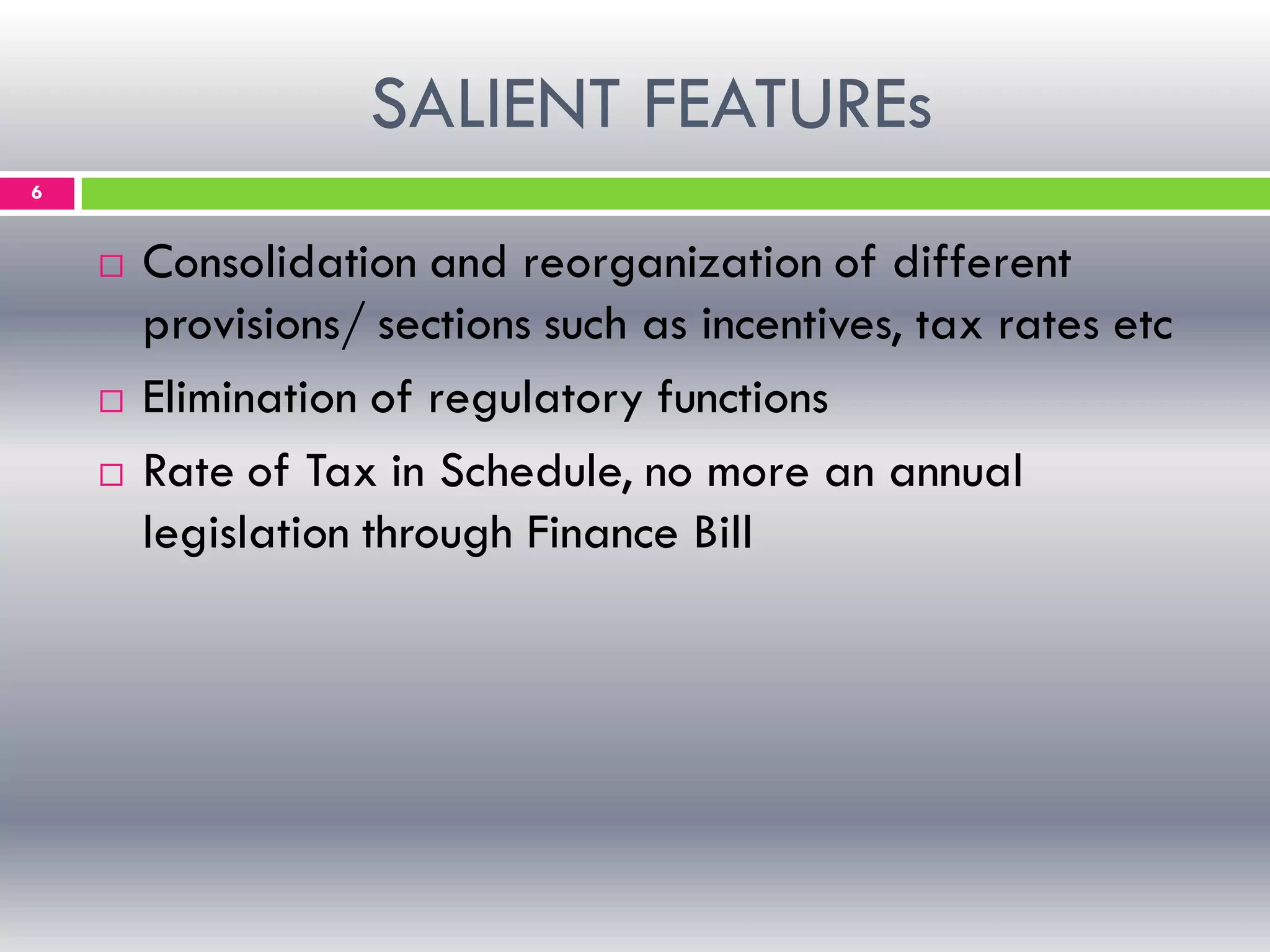

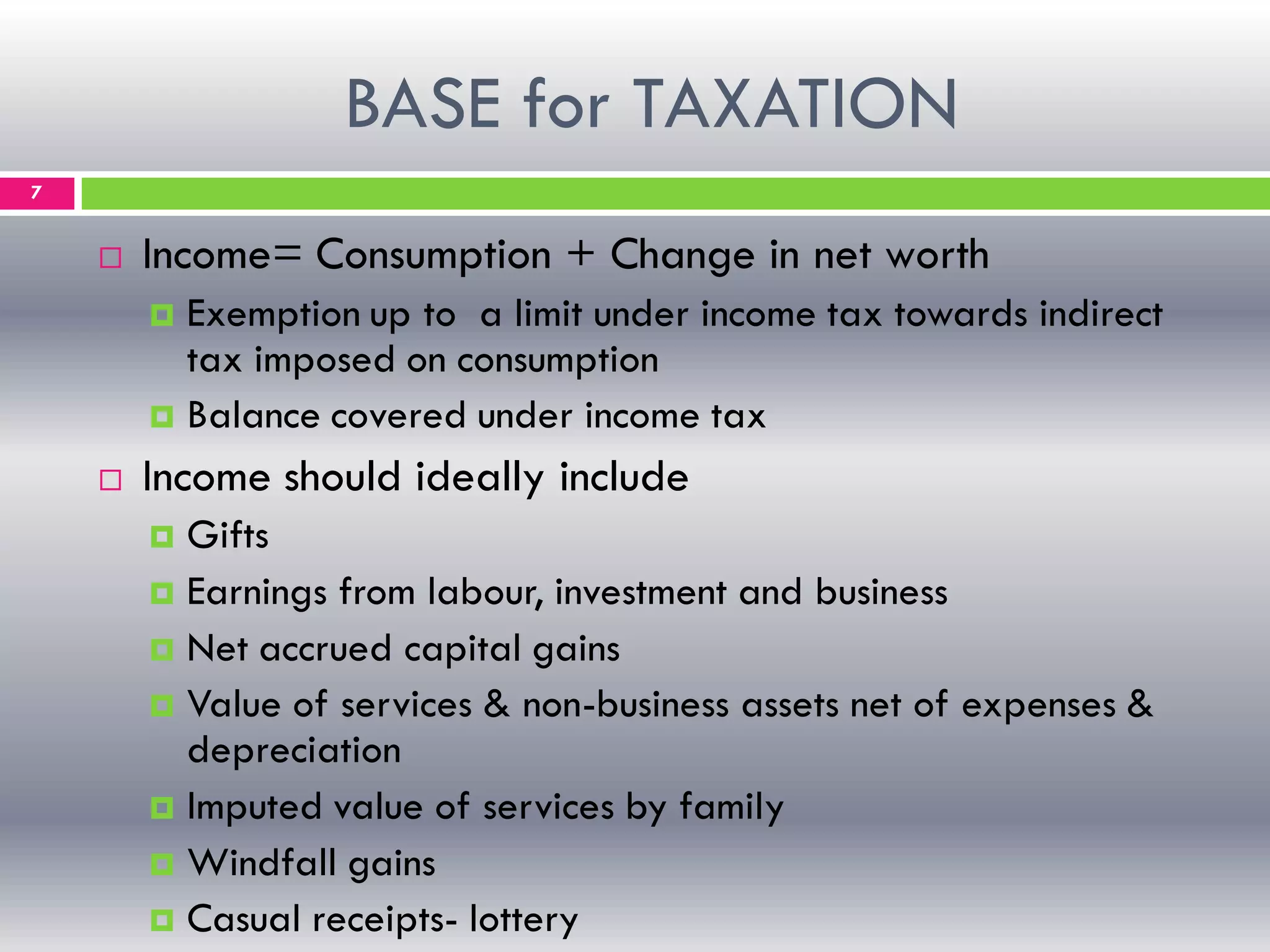

The document provides background on India's direct tax code. It notes the existing income tax act has undergone many amendments and other taxes like wealth tax are administered separately by different laws. This leads to conflicting court rulings and complexity for taxpayers. The new direct tax code aims to simplify laws, avoid exemptions, minimize tax avoidance, keep pace with court rulings, and encourage self-assessment and compliance through technology. It will consolidate all direct taxes under one code with simple language. Key features include eliminating regulatory functions, setting tax rates in schedules instead of annual finance bills, and delegating powers to reduce litigation.