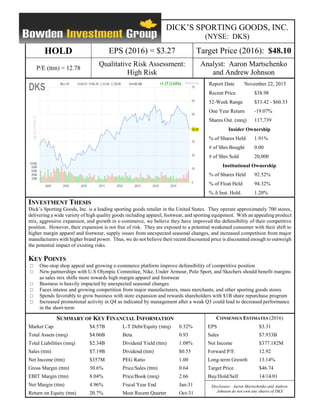

1. DICK’S SPORTING GOODS, INC.

(NYSE: DKS)

HOLD EPS (2016) = $3.27 Target Price (2016): $48.10

P/E (ttm) = 12.78

Qualitative Risk Assessment:

High Risk

Analyst: Aaron Martschenko

and Andrew Johnson

Report Date November 22, 2015

Recent Price $38.98

52-Week Range $33.42 - $60.33

One Year Return -19.07%

Shares Out. (mrq) 117,739

Insider Ownership

% of Shares Held 1.91%

# of Shrs Bought 0.00

# of Shrs Sold 20,000

Institutional Ownership

% of Shares Held 92.52%

% of Float Held 94.32%

% Δ Inst. Hold. 1.20%

INVESTMENT THESIS

Dick’s Sporting Goods, Inc. is a leading sporting goods retailer in the United States. They operate approximately 700 stores,

delivering a wide variety of high quality goods including apparel, footwear, and sporting equipment. With an appealing product

mix, aggressive expansion, and growth in e-commerce, we believe they have improved the defensibility of their competitive

position. However, their expansion is not free of risk. They are exposed to a potential weakened consumer with their shift to

higher margin apparel and footwear, supply issues from unexpected seasonal changes, and increased competition from major

manufacturers with higher brand power. Thus, we do not believe their recent discounted price is discounted enough to outweigh

the potential impact of existing risks.

KEY POINTS

□ One-stop shop appeal and growing e-commerce platform improve defensibility of competitive position

□ New partnerships with U.S Olympic Committee, Nike, Under Armour, Polo Sport, and Skechers should benefit margins

as sales mix shifts more towards high margin apparel and footwear

□ Business is heavily impacted by unexpected seasonal changes

□ Faces intense and growing competition from major manufacturers, mass merchants, and other sporting goods stores

□ Spends favorably to grow business with store expansion and rewards shareholders with $1B share repurchase program

□ Increased promotional activity in Q4 as indicated by management after a weak Q3 could lead to decreased performance

in the short-term

SUMMARY OF KEY FINANCIAL INFORMATION CONSENSUS ESTIMATES (2016)

Market Cap. $4.57B L-T Debt/Equity (mrq) 0.32% EPS $3.31

Total Assets (mrq) $4.06B Beta 0.93 Sales $7.933B

Total Liabilities (mrq) $2.34B Dividend Yield (ttm) 1.08% Net Income $377.182M

Sales (ttm) $7.19B Dividend (ttm) $0.55 Forward P/E 12.92

Net Income (ttm) $357M PEG Ratio 1.00 Long-term Growth 13.14%

Gross Margin (ttm) 30.6% Price/Sales (ttm) 0.64 Target Price $46.74

EBIT Margin (ttm) 8.04% Price/Book (mrq) 2.66 Buy/Hold/Sell 14/14/01

Net Margin (ttm) 4.96% Fiscal Year End Jan-31 Disclosure: Aaron Martschenko and Andrew

Johnson do not own any shares of DKSReturn on Equity (ttm) 20.7% Most Recent Quarter Oct-31

2. Company Overview

Dick’s Sporting Goods is a sporting goods retailer that began operations in 1948 in Binghamton, NY and is now

headquartered in Coraopolis, PA. As a sporting goods store, DKS offers a wide variety of products. They separate their

product segments into hardlines, apparel, footwear, and other. While they maintain a higher-quality of sporting goods

products, Dick’s accommodates the consumer’s style from a beginner to an enthusiast athlete. Hardlines refers to items

such as sporting goods equipment, fitness equipment, golf equipment and outdoors gear. The category other, refers to

Dick’s non-merchandising sales category, which includes in-store services provided and revenue from shipping. The

following chart expresses the approximate percentage of sales in regards to the four categories for fiscal year 2014:

Dick’s also owns and operates three specialty stores; Field & Stream, Golf Galaxy, and True Runner. Dick’s

prides itself on presenting and selling higher-performance items geared more directly towards the serious athlete. As of

August 2015, Dick’s operates over 600 stores in 46 states, 75 Golf Galaxy stores in 29 states, 12 Field & Stream stores in

seven states, and three True Runner stores in three states. A majority of these stores are located from the Mideast to the

East coast of the United States, but Dick’s is making strides to open more stores on the West coast, offering a wider range

of operations.

In terms of the management of DKS, the company has been held in family hands since Edward Stack, son of

Dick’s founder, became the CEO and Chairman of the Board of Directors in 1984. The Board of Directors is comprised of

Stack, William Colombo, and seven members outside the company.

Industry Outlook

The Sporting Goods Stores industry in the United States can be characterized by high internal and external

competition, a mature life cycle stage, and reliance on the business cycle and consumer preferences.

Overall, industry growth is fairly flat. This is due to the high amount of competition and lack of differentiation

across competing companies. Within the industry, sporting goods stores face significant competition from each other

3. because major suppliers such as Nike and Adidas supply products to nearly every company. In order to stay competitive,

these major brands must be carried at all stores. Therefore, the amount of differentiation in products offered between stores

is minimal. Competition is furthered by the threat of external competitors. External competitors include mass

merchandisers such as Walmart and Target, and major suppliers to the sporting goods store industry. Mass merchandisers

add to the competition for sporting goods sales because they typically carry a range of lower to medium priced goods that

tend to be lesser quality than some of the brands typically offered at sporting goods stores. This is a threat to lower priced

goods sold in the industry. Major suppliers contribute to the competition for sporting goods sales because they carry the

same high quality products that are stocked at sporting goods stores, albeit a narrower selection of brands. The more direct-

to-consumer avenues that major suppliers develop, the greater risk to the sales of participants in the sporting goods store

industry. These avenues can include an increasing number of outlet stores and a growing online retail presence. In fact,

both mass merchandisers and major suppliers carry the threat to the sporting goods store industry of developing better

online retail sites.

Despite all of the competition those in the industry are exposed to and the industry’s mature life cycle stage, there

are still attractive investment opportunities. To combat external competition, sporting goods stores need to grow their

online retailing abilities and increase the amount of high quality products they offer. A way this can be done is by securing

key relationships with suppliers to provide private-label brands and other less commonly found products that appeal to

niche markets and provide unique value. We believe that what makes a customer prefer to shop in one store over another

for their sporting goods is the amount and quality of selection they have available to them. It makes it much easier on the

customer to walk into only one store and compare products like shoes and baseball bats of varying prices and brands,

instead of having to shop at multiple locations to identify the best product. By offering a large selection of high quality and

highly demanded products in comparison to other companies, sporting goods stores can offer a one-stop shop appeal that

other competitors don’t have. This is crucial in minimizing the negative impact that direct internal competition, and also

external competitors like mass merchandisers and major suppliers to the industry will have.

We believe that going forward, there is investment opportunity and growth in companies that can offer the

broadest product portfolio of high quality goods for one-stop shop appeal, develop online retail, and expand their

geographical footprint to draw a larger consumer base and build brand reputation.

Company Outlook

To stay competitive in the industry, sporting goods stores have to develop a business model that adapts to new

consumer shopping preferences and keeps customers from purchasing their sporting goods from other distribution channels.

We believe Dick’s has responded to the threat of competition better than their competitors and have set themselves up for

future success. As major manufacturers such as Nike and Adidas increase their direct-to-consumer distribution channels

with both online and brick-and-mortar stores, it is imperative for sporting goods stores to do the same if they hope to keep

their customer base. In the general retail environment, we believe that e-commerce will play a role of increasing

importance because it provides customers with the value of having immediate information. Customers are able to quickly

shop around for the best price online and then order the product right now, or go to a physical store location to test out the

product before they purchase it. We see three ways that companies can adjust to the impact of changing consumer behavior

4. and believe Dick’s Sporting Goods has made adjustments superior to those of their competitors in their industry. Those

three things are to further develop one-stop shop appeal and grow their brand, adapt product mix to consumer preferences,

and grow their e-commerce segment.

We believe Dick’s Sporting Goods has developed their one-stop shop appeal much better than competitors in the

industry. We view this factor as one of the most important aspects that contributes to long-term success. Although e-

commerce growth is a key factor in long-term success, we are convinced that what really attracts people to a sporting goods

store over a mass merchant or outlet store for Nike is the wide availability of high quality products. When a customer goes

into a sporting goods store, having more options appeals to the value-conscious consumer and is important in retaining

customer base. Dick’s has an advantage because they have secured key relationships with suppliers that others don’t have

and the average size of their stores is larger than competitors. Dick’s operates stores that are about 50,000 square feet on

average while their closest competitor in Hibbett Sports only averages about 5,000 square feet. They have expanded each

year in store count by adding about 35-50 stores each year. Other companies in the industry have not been able to exhibit

this kind of expansion and we believe this increases Dick’s brand power relative to other sporting goods stores.

In addition to the appeal of their stores, they have made changes in their sales mix, which we see as a positive.

Not only has Dick’s secured relationships with major companies like Nike and Under Armour to offer a store-within-a-

store format, they have also shifted their product mix to being more heavily weighted in apparel and footwear. This

capitalizes on the current athleisure trend in the industry. They have secured a partnership with the United States Olympic

Committee, Skechers, Polo Sport, and Nike Air Jordan. We believe incorporating these products into their sales mix adds

more variety to the products and services they offer and with each of these partnerships providing high quality and higher

margin goods, it will improve the appeal of their store over those of competitors.

In addition, growth in e-commerce is something we believe will be a major factor going forward in the ways

consumers shop for goods. Because consumers have so much data available to them, they can shop around quickly for the

best price. Having an established brand and e-commerce platform brings customer attention to the company and even if the

customer doesn’t purchase the goods directly from the website, they may want to go to the store to test out the product

before ordering it. Thus, e-commerce growth is important in keeping strong sales at physical locations too, not just online.

We view growth in e-commerce sales as a major factor in keeping customers from shopping online at a Nike website or

other competitor.

Overall, we believe Dick’s Sporting Goods has made more aggressive efforts to expand their presence in the

industry and compete with external competition. With their growth strategy, attractive store layout and shifts in product

mix, we believe they have improved the defensibility of their competitive position. Despite these strengths, given their

recent weak performance in the third quarter and management’s expressed interest to create a “more promotional

environment,” we do believe the short-term outlook is not as strong as over the long-term. Promotional and advertisings

costs are one of the major factors for drops in profit margins for the past year and this could lead to weaker performance to

round out the year. We expect promotional costs will be higher because Dick’s will want to get rid of the piled up

inventory, and will hope to increase traffic in their stores as same store sales growth was weaker than expected in the third

quarter. Thus, we believe they may struggle in the near-term and that the risk is too high to be overly optimistic on their

long-term outlook.

5. Financial Analysis

Historically, return on equity for Dick’s Sporting Goods has been higher than the industry average but slightly

lower than their most similar competitor, Hibbett Sports. Growth in return on equity is due to improvement in profit

margins and more efficient use of assets. The use of debt has been limited and has had minimal positive or negative impact

on ROE in past years.

Table 1 – Return on Equity Components for Dick’s Sporting Goods, Inc.

2010 2011 2012 2013 2014 TTM

Hibbett

Sports

Industry

Average

Net profit margin 3.7% 4.9% 5.3% 5.4% 5.1% 5.0% 8.1% 6.8%

Total asset turnover 1.9 times 1.7 times 2.0 times 2.0 times 2.0 times 1.8 times 2.0 times 1.3 times

Equity multiplier 1.9 times 1.8 times 1.8 times 1.8 times 1.9 times 2.4 times 1.4 times 2.1 times

Return on equity 13.4% 15.6% 19.5% 20.0% 18.8% 20.7% 23.4% 18.6%

Source: Return on equity components are calculated from company financial statements

Industry averages are calculated from Bloomberg data

Each year, profit margins have had the most fluctuation and most impact on return on equity. After evaluation of

companies within the industry, factors we believe have the largest impact on profitability are: competitive pressures that

result in increased spending, and efficient production from existing stores.

In the sporting goods store industry, there are high levels of both internal and external competition. To retain the

appeal of a sporting goods store and defend against rising competition, those within the industry need to expand their

presence by increasing the size and number of brick-and-mortar stores, and by furthering their online presence.

Accomplishing this without hurting margins significantly is no easy task because it requires a substantial amount of

spending. Due to the increased emphasis on brand presence and expansion, cash has declined (Appendix A-4), while

additional costs have accumulated. Major costs incurred include occupancy costs of new and/or larger facilities, increased

shipping costs associated with the growing importance of e-commerce development, and advertising costs to promote

newly established stores.

Companies such as Dick’s Sporting Goods have responded to increased competition by ramping up spending and

expansion. The degree of spending and expansion has led to increased inventory levels for Dick’s over the past five years,

as well as property, plant & equipment (Appendix A-3). Other companies within the industry have not exhibited the same

amount of expansion efforts. The closest comparison is with Hibbett Sports, which has an ROE greater than that of Dick’s.

They have expanded with approximately 15 stores each year and with their average store size being approximately 1/10 the

size of a Dick’s store, their expenses associated with expansion are much less. As a result, Dick’s absolute revenue is much

higher than Hibbett Sports and commands significantly more market share. However, Dick’s expense ratios are also

higher, indicated by lower profit margins. They have incurred significant costs related to the increased salary expenses,

increased shipping expenses, advertising costs for products and new stores, and occupancy costs over the past several years.

Due to these higher expenses, their gains in profit margins from increased sales have been limited and we believe it’s the

6. main reason for not being up to par with the margins of Hibbett Sports. In the most recent fiscal year, Dick’s net profit

margin had declined due to these additional expenses and offset any gains from their move to a higher margin product mix.

Despite being below their closest competitor in net profit margins, we believe their expansion strategy will allow them to

improve in the future. The more market share they gain, a smaller amount of money will have to be spent on some

expenses that have hurt their profit margins in the past. For example, occupancy costs as a percentage of net sales dropped

ten basis points in their most recent fiscal year, which is a trend we believe will continue based on results of same store

sales in the industry.

Table 2 – Annual Same Store Sales Increase for DKS and Main Competitors

2010 2011 2012 2013 2014

DKS 7.4% 2.0% 4.3% 1.9% 2.4%

HIBB 1.6% 2.8% 6.9% 3.9% (12.3%)

CAB 0.1% 9.8% 6.8% 6.9% 1.8%

Source: Data obtained from company financial statements

Shown in Table 2, Dick’s same store sales growth has been more than those of their closest publicly traded

competitors in the most recent fiscal year, indicating improvements in efficiency of existing stores. Cabela’s had suffered

because of a decline for demand in hunting and fishing equipment, which makes up most of their sales. We believe Hibbett

Sports suffered because of their lack of ability to defend against rising competition. Hibbett Sports performs well in

smaller markets away from large competitors where they rely on their customer service to attract customers despite a

smaller product selection than companies such like Dick’s. We believe there are two major factors hurting their same store

sales. The first is the lack of development in their e-commerce platform that leaves them vulnerable to competition from

companies like Nike, Adidas, and Under Armour with strong internet presence. Secondly, the increasing presence of

Dick’s Sporting Goods across the United States competes with their stores in smaller markets, possibly stealing away sales

because we believe Dick’s offers a much larger selection of and more high profile products that consumers prefer in a

sporting goods store.

In regards to same store sales growth, we believe it can be improved through proper asset management. Dick’s

total asset turnover ratio of 2.0 (Table 1), is above industry average and right in-line with 2.0 for Hibbett Sports. Although

their fixed asset turnover ratio is lower than the industry (Appendix A-6), because of the risk of new stores not immediately

performing well in new markets, their higher inventory turnover allows them to get more production out of each asset.

Product mix is of critical importance in determining total asset turnover. We believe Dick’s product mix is better because

of their shift to a higher proportion of higher margin athletic apparel and footwear in their stores and supplier relationships

that allow them to carry products that other stores in the industry do not. The shift to a product mix with more apparel and

footwear capitalizes on the current athleisure trend and appeals to what the consumer wants now, aiding inventory turnover

and overall asset management. Historically, strong asset management has been a stable area of performance for Dick’s

Sporting Goods and has allowed them to have a return on equity exceeding that of the industry average despite having

lower profit margins.

7. Aside from the impacts of decisions impacting profitability and efficient use of assets in the industry, the use of

financial leverage is another factor impacting return on equity. However, it has played less of a role in upward or

downward moves in Dick’s return on equity. This is mainly due to their emphasis on not using much debt in financing

their expansion. After fiscal 2011, the use of debt financing played even less of a role. We believe this has allowed them to

still be in decent financial position even with a low level of liquidity. Going forward we expect debt will be used in

emergency situations such as in this most recent quarter in FY 2015, with the impact displayed in their TTM ROE (Table

2). Management’s assertions to have zero outstanding debt under their revolving credit facility demonstrates their efforts to

have very limited use of debt, and we believe it is indicative of how they will handle future borrowings (Appendix B-4).

Based on Dick’s corporate strategy, we believe their financial condition is sound. Dick’s Sporting Goods has

typically been able to generate a free cash flow per share greater than industry average (Appendix A-6) due to their efforts to

improve profitability and obtain more production out of each asset. To improve profitability, they have improved the

defensibility of their competitive position by further expanding into new markets and strengthening their internet presence,

and they have shifted their product mix to a higher proportion of high margin athletic apparel and footwear. By improving

their brand presence and better accommodating product mix to consumer preferences, they have been able to improve

efficiency of each asset and their existing stores, with limited exceptions such as their most recent quarter. This has

allowed them to expand with little use of debt. In addition, Dick’s has approached its brand presence expansion through the

usage of their cash balances as sources of funding. Between FY 2011 and FY 2013, cash & cash equivalents decreased

11.2% in relation to revenue (Appendix A-5). Despite having low liquidity due to the heavy use of cash balances used to

grow the company, we believe that they will continue to generate free cash flow per share above the industry average

because of how well they have implemented their corporate strategy focused on long-term growth. There is still the risk

that newly established stores and/or existing stores may perform worse than expected due to a variety of factors leading

DKS to not generate their usual level of free cash flow per share. However, because we are confident in their ability to

generate more than enough cash to pay down their low levels of debt, we believe Dick’s is in great financial condition.

Stock Valuation

We are using a justified P/E ratio of 14.0 times in our valuation, which is higher than Dick’s TTM P/E of 12.78.

We believe this is a conservative multiple based on what investors are willing to pay for comparable companies (Appendix

B-7). Our view is that Dick’s stock is trading much cheaper now because of the recent influx of negative news surrounding

many US retailers, management’s EPS guidance cut for the current fiscal year, and negative performance in the third

quarter consistent with that of overall retail companies. Because we believe Dick’s growth strategy will have its most

beneficial impacts in the future due to how they have improved the defensibility of their competitive position and investors

have proven to pay a historical average of 21.45 times earnings, we have raised our justified P/E higher than that of their

TTM P/E.

We have applied our justified P/E ratio to our expected 2016 diluted EPS of $3.29 (Appendix B-2). Our earnings

per share outlook sharply declined after Dick’s reported earnings in the third quarter. The main drivers behind this were

management’s drastic guidance cut and our belief that to get rid of excess inventory, Dick’s would have to ramp up

8. promotional activity and sales, which would put pressure on margins (Appendix B-3). This puts our forecasted one year

EPS growth rate at 10.03%, which is significantly lower than their 4-year EPS growth rate of 26.03%. However, as Dick’s

growth in EPS has slowed in recent years, we believe it is more representative of the current picture (Appendix B-6). We

believe our estimate of $3.29 is correct and is a fairly conservative estimate as it is just under consensus EPS of $3.31 and

slightly higher than the average of other analyst’s revisions after the most recent quarter (Appendix B-5).

In regards to our EV/EBITDA multiple, we have used 8.0 times, which is right around both Dick’s and Hibbett’s

TTM EV/EBITDA. Although we see a possibility in Dick’s performing better in the future, we applied a more

conservative multiple to display the risk of a weakened consumer and challenges in developing new stores in that

environment. Our estimate captures the recent performance from DKS and their closest competitor, and it is lower than

both of their three year averages (Appendix B-8), which was a period of increased performance for those in the sporting

goods store industry. We believe that multiples closer to those of the most recent year are more indicative of spending

behaviors than a historical three year view. Using a multiple of 8.0 times and our expected 2016 EBITDA of $851,461, we

arrived at a target price of $58.82.

To arrive at our target price per share of $49.27, we used weighted average of P/E and EV/EBITDA valuation

metrics. We believe our P/E ratio gives a better estimate of how investors will value a sporting goods retailer like Dick’s

than valuation using our EV/EBITDA multiple. Valuation using our EV/EBITDA multiple gives us a target price outside

of the highest of other analyst target prices (Appendix B-9). Thus, we decided to weight our P/E multiple at 75% and

valuation using EV/EBITDA at 25%, arriving at a target price of $49.27 (refer to Appendix B-1 for further valuation

discussion and Appendix B-10 for detailed valuation).

Investment Risks

Risks related to performance include consumer spending behavior, seasonal impacts, effects of Dick’s gross profit

margin, and impact of increased competition. Being involved in retail, Dick’s is inherently vulnerable to changes in

consumer spending habits. This could impact Dick’s because as they have shifted their product mix to high margin apparel

and footwear. The shift in product mix was largely seen as a positive because it goes along with the athleisure trend in the

industry. However, these products tend to be more expensive and their sales could be negatively impacted if consumers are

less willing to spend on discretionary items. This could have a large impact on Dick’s performance because as they have

expanded aggressively to defend against competition and grow their brand, they have also included significant costs. If

customers are not as willing to spend and their new stores that are incurring expenses do not generate the revenue as

expected, their profits could take a hit.

In regards to how many retail companies have performed this most recent quarter, the impacts of unexpected

seasonal adjustments are clear. In the third quarter, many retail companies have reported weaker than expected earnings.

Many of them cite the reason for this as sluggish sales and the build-up of inventory due to surprising warm weather that

impacts more seasonal products. In Dick’s most recent quarter, they had similar problems because of warmer weather that

offset any gains they had in athletic apparel and footwear. It goes to show how prone retail companies are to weather

conditions for a large assortment of products. Selling more apparel in sporting goods stores could leave them more

vulnerable in the future to weather trends and they could have a repeat performance of this most recent quarter. Products

9. dependent on weather conditions in a Dick’s Sporting Goods store include their hunting equipment and various types of

clothing.

Gross profit has decreased to 30.6% after reaching their peak in 2012 at 31.5%. The decline can be attributed to

expenses related to expansion (Appendix A-1). Main reasons for a decline are higher inventory costs, higher promotional

costs as a percentage of sales, and higher shipping costs. With the recent decline in the gross profit margin, this has a direct

impact on diluted earnings per share. However, due to the five year, $1,000,000,000 share repurchase program announced

in March 2013, the growth rate in diluted EPS has declined at a lesser rate compared to that of the growth rate in net income

(Appendix A-2) as a percentage of sales. Moving forward, store expansion and the variability of associated costs

incorporates risk factors relating to Dick’s overall performance.

Lastly, Dick’s Sporting Goods performance could be influenced by the impact of increased competition. Both

Nike and Under Armour are two major companies that have expressed desires to increase their direct-to-consumer

segments, both with online and physical store locations. This could have an adverse impact on sales because even though

Under Armour and Nike don’t have as wide of a variety, both offer many of the same high quality products and carry

higher brand power.

The impact of these risks can be substantial, each with the ability to put downward pressure on margins, as can be

seen in the most recent quarter. Management’s guidance was cut severely for FY 2015. We believe they anticipate lower

profit margins because of the need to get rid of inventory using more promotional selling measures. Colder weather apparel

and hunting products are often higher margin and higher priced goods. In the absence of typical these key sales in the later

parts of the year, gross profit could suffer. Our forecasts for revenue growth rate and gross profit margins are 8.0% and

30.7% respectively, with a projected diluted EPS of $3.29 for FY 2016. Shown in Table 3, even a small decline in gross

profit margins would have a large impact on earnings per share for DKS.

Table 3: Impact of Investment Risks on Diluted EPS

Source: Analyst’s Calculations

Recommendation

Dick’s Sporting Goods is a HOLD at the current share price of $38.98. Their improvements in e-commerce,

aggressive expansion strategy, relationships with suppliers, and shift to a more favorable product mix based on industry

trends give them the tools to improve their competitive position. This could potentially make them an attractive buy later

on. However, because they are so dependent on consumer spending and are prone to adverse impacts from competition in

10. companies that have much larger brand power, we only foresee Dick’s moderately besting the market, and with high risk to

that assertion. In the short-term, we expect they will struggle. Management had cut EPS guidance for FY 2015 to a range

of $2.85 - $3.00 from a range of $3.13 to $3.21. They had also indicated that they would have a more promotional

environment in the fourth quarter of this year. We believe this is because their same store sales in the quarter were not as

high as expected and need more marketing efforts to drive up their sales. Promotional costs in the past have proven to be

one of the driving forces in putting pressure on their margins. Even though we expect some margin improvement because

of a better sales mix, higher promotional activity will likely limit these gains once again. We believe Dick’s is a great

company with the possibility of upside because of their attractive store layout and product mix. However, we do not

believe the stock is a buy right now because of the risks involved while they are trying to expand aggressively.

11. References

1. Bloomberg Finance L.P

2. Athletic Apparel: Outperforming the Competition in 2014. Retrieved from http://fortune.com/2014/12/25/athletic-

apparel-top-performer/. Author: Kell, John.

3. Sporting Goods Logistics: Keeping the Ball Rolling. Retrieved from

http://www.inboundlogistics.com/cms/article/sporting-goods-logistics-keeping-the-ball-rolling/. Author: Brown,

Justine.

4. Product Life Cycle Stages. Retrieved from http://productlifecyclestages.com/product-life-cycle-stages/maturity/

5. 7 Charts that Show the State of Youth Sports in the US and Why it Matters. Retrieved from

http://www.aspeninstitute.org/about/blog/7-charts-that-show-the-state-of-youth-sports-in-the-us-and-why-it-

matters. Author: Lee, Alice.

6. IBISWorld Industry Report 45111 – Sporting goods Stores in the US. IBISworld.com. Retrieved from http://0-

clients1.ibisworld.com/wncln.wncln.org/reports/us/industry/default.aspx?entid=1079.

7. Sporting Goods Industry FAQ. Retrieved from https://www.nsga.org/globalassets/research/public/sporting-goods-

industry-faq---2015.pdf.

8. Edited Transcript of DKS Earnings Conference Call. Retrieved from http://finance.yahoo.comnews/edited-

transcript-dks-earnings-conference-012935404.html.

9. Investor Relations – Dick’s Sporting Goods. Retrieved from http://investors.dicks.com/company-

information/company-overview.aspx.

10. Why Nike Air Jordan, Polo Sport stores-within-a-store coming to Dick’s Sporting Goods Near You. Retrieved

from http://www.bizjournals.com/pittsburgh/news/2015/08/18/why-ralph-laurennike-air-jordan-polo-sport-

stores.html. Author: Schooley, Tim.

11. Dick’s Sporting Goods, Inc. Form 10-K. U.S Securities and Exchange Commission. Retrieved from

http://www.sec.gov/cgi-bin/browse-edgar?CIK=DKS&Find=Search&owner=exclude&action=getcompany

2010

2011

2012

2013

2014

12. Dick’s Sporting Goods, Inc. Form 10-Q. U.S Securities and Exchange Commission. Retrieved from

http://www.sec.gov/cgi-bin-browse/edgar?CIK=DKS&Find=Search&ownder=exclude&action=getcompany

10-Q: Filed 08/28/2014

10-Q: Filed 11/26/2014

10-Q: Filed 05/28/2015

10-Q: Filed 08/27/2015

12. References (cont.)

13. Dick’s Sporting Goods, Inc. Form 8-K. US Securities and Exchange Commission. Retrieved from

http://www.sec.gov/Archives/edgar/data/1089063/000108906315000084/0001089063-15-000084-index.htm

13. Appendix A-1: Income Statement

Source: Company Filings & Analyst’s Estimates

INCOMESTATEMENT

Fiscal year 2010A 2011A* 2012A* 2013A 2014A TTM 2015P 2016P

Fiscal year end date 1/29/2011 1/28/2012 2/2/2013 2/1/2014 1/31/2015 10/31/2015 1/31/2016 1/31/2017

Net sales 4,871,492 5,211,802 5,836,119 6,213,173 6,814,479 7,190,920 7,393,710 7,985,206

Cost of good sold, inc. occupancy and distribution costs (3,422,462) (3,616,921) (3,998,956) (4,269,223) (4,727,813) (4,988,743) (5,131,235) (5,533,748)

Gross profit 1,449,030 1,594,881 1,837,163 1,943,950 2,086,666 2,202,177 2,262,475 2,451,458

Selling, general and administrative expenses (1,129,293) (1,148,268) (1,297,413) (1,386,315) (1,502,089) (1,590,424) (1,663,585) (1,812,642)

Pre-opening expenses (10,488) (14,593) (16,076) (20,823) (30,518) (33,874) (36,969) (39,926)

EBIT/income from operations 309,249 432,020 523,674 536,812 554,059 577,879 561,922 598,890

Interest expense (14,016) (13,868) (6,034) (2,929) (3,215) (3,535) (627) (542)

Interest income 0 0 0 0 0 0 0 0

Other income 2,278 (26) 4,555 12,224 5,170 1,119 5,170 5,170

EBT/income before income taxes 297,511 418,126 522,195 546,107 556,014 575,463 566,465 603,519

Provision for income taxes (115,434) (162,651) (212,533) (208,509) (211,816) (218,528) (215,111) (229,182)

Net income 182,077 255,475 309,662 337,598 344,198 356,935 351,354 374,337

Basic shares outstanding 116,236 120,232 121,629 122,878 119,244 116,101 116,045 112,068

Impact of dilutive securities 5,488 5,536 4,366 2,750 1,994 1,638 1,638 1,638

Diluted shares outstanding 121,724 125,768 125,995 125,628 121,238 117,739 117,683 113,706

Basic EPS $1.57 $2.12 $2.55 $2.75 $2.89 $3.07 $3.03 $3.34

DilutedEPS $1.50 $2.03 $2.46 $2.69 $2.84 $3.03 $2.99 $3.29

14. Appendix A-2: Common-Size Income Statement

Source: Company Filings & Analyst’s Estimates

COMMON-SIZEINCOMESTATEMENT

Fiscal year 2010A 2011A* 2012A* 2013A 2014A TTM 2015P 2016P

Fiscal year end date 1/29/2011 1/28/2012 2/2/2013 2/1/2014 1/31/2015 10/31/2015 1/31/2016 1/31/2017

Net Sales 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Cost of good sold, inc. occupancy and distribution costs 70.3% 69.4% 68.5% 68.7% 69.4% 69.4% 69.4% 69.3%

Gross profit 29.7% 30.6% 31.5% 31.3% 30.6% 30.6% 30.6% 30.7%

Selling, general and administrative expenses 23.2% 22.0% 22.2% 22.3% 22.0% 22.1% 22.5% 22.7%

Pre-opening expenses 0.2% 0.3% 0.3% 0.3% 0.4% 0.5% 0.5% 0.5%

EBIT/income from operations 6.3% 8.3% 9.0% 8.6% 8.1% 8.0% 7.6% 7.5%

Interest expense 0.3% 0.3% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0%

Interest income 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other income 0.0% 0.0% 0.1% 0.2% 0.1% 0.0% 0.1% 0.1%

EBT/income before income taxes 6.1% 8.0% 8.9% 8.8% 8.2% 8.0% 7.7% 7.6%

Provision for income taxes 2.4% 3.1% 3.6% 3.4% 3.1% 3.0% 2.9% 2.9%

Net income 3.7% 4.9% 5.3% 5.4% 5.1% 5.0% 4.8% 4.7%

15. Appendix A-3: Balance Sheet

Source: Company Filings & Analyst’s Estimates

BALANCESHEET

Fiscal year 2010A 2011A* 2012A* 2013A 2014A MRQ 2015P 2016P

Fiscal year end date 1/29/2011 1/28/2012 2/2/2013 2/1/2014 1/31/2015 10/31/2015 1/31/2016 1/31/2017

Assets

Current assets:

Cash and cash equivalents 546,052 734,402 345,214 181,731 221,679 73,799 165,397 199,808

Accounts receivable, net 34,978 38,338 34,625 60,779 80,292 96,406 96,118 111,793

Income taxes receivable 9,050 4,113 15,737 7,275 14,293 8,719 14,293 14,293

Inventories, net 896,895 1,014,997 1,096,186 1,232,065 1,390,767 1,997,105 1,693,307 1,770,799

Prepaid expenses and other current assets 58,394 64,213 73,838 99,386 91,767 107,755 91,767 91,767

Deferred income taxes 18,961 12,330 30,289 38,835 51,586 47,789 51,586 51,586

Total current assets 1,564,330 1,868,393 1,595,889 1,620,071 1,850,384 2,331,573 2,112,468 2,240,047

Property and equipment, net 684,886 775,896 840,135 1,084,529 1,203,382 1,341,166 1,384,084 1,579,243

Construction in progress --- leased facilities 0 2,138 0 0 0 0 0 0

Intangible assets, net (inc. Goodwill) 251,664 251,084 299,497 298,849 310,756 310,421 309,203 307,705

Deferred income taxes 27,157 12,566 4,382 2,477 1,862 1,355 1,862 1,862

Other assets 69,499 86,375 147,904 65,561 69,814 73,912 69,814 69,814

Total assets 2,597,536 2,996,452 2,887,807 3,071,487 3,436,198 4,058,427 3,877,432 4,198,670

Liabilities andStockholder's Equity

Current liabilities:

Accounts payable 446,511 510,398 507,247 562,439 614,511 941,973 872,310 913,068

Accrued expenses 279,284 264,073 269,900 265,040 283,828 345,052 354,898 375,305

Deferred revenue and other liabilities 121,753 128,765 146,362 154,384 172,259 133,593 184,843 199,630

Income taxes payable 0 29,484 68,746 19,825 47,698 0 47,698 47,698

Current portion of other long-termdebt and leasing obligations 995 7,426 8,513 899 537 575 800 950

Total current liabilities 848,543 940,146 1,000,768 1,002,587 1,118,833 1,421,193 1,460,549 1,536,651

Long-termliabilities:

Revolver 0 0 0 0 0 342,400 0 0

Long-termdebt and leasing obligations 139,846 151,596 7,762 6,476 5,913 5,477 5,113 4,163

Non-cash obligations for construction in progress --- leased facilities 0 2,138 0 0 0 0 0 0

Deferred income taxes 0 0 7,413 38,617 44,494 29,078 44,494 44,494

Deferred revenue and other liabilities 245,566 269,827 284,540 331,628 434,733 536,973 517,560 574,935

Total long-termliabilities 385,412 423,561 299,715 376,721 485,140 913,928 567,167 623,592

Total liabilities 1,233,955 1,363,707 1,300,483 1,379,308 1,603,973 2,335,121 2,027,715 2,160,243

Stockholder's equity:

Common stock / additional paid-in capital 626,122 700,730 875,217 959,904 1,016,336 1,054,631 1,045,009 1,076,009

Class B common stock 250 250 249 249 249 249 249 249

Retained earnings 730,468 932,871 911,704 1,187,514 1,471,182 1,623,962 1,760,000 2,067,711

Other comprehensive income / (loss) 6,741 118 112 24 (73) (125) (73) (73)

Treasury stock 0 (1,224) (199,958) (455,512) (655,469) (955,411) (955,469) (1,105,469)

Total stockholder's equity 1,363,581 1,632,745 1,587,324 1,692,179 1,832,225 1,723,306 1,849,716 2,038,427

Total liabilities andstockholder's equity 2,597,536 2,996,452 2,887,807 3,071,487 3,436,198 4,058,427 3,877,432 4,198,670

16. Appendix A-4: Common-Size Balance Sheet

Source: Company Filings & Analyst’s Estimates

COMMON-SIZEBALANCESHEET

Fiscal year 2010A 2011A* 2012A* 2013A 2014A MRQ 2015P 2016P

Fiscal year end date 1/29/2011 1/28/2012 2/2/2013 2/1/2014 1/31/2015 10/31/2015 1/31/2016 1/31/2017

Assets

Current assets:

Cash and cash equivalents 21.0% 24.5% 12.0% 5.9% 6.5% 1.8% 4.3% 4.8%

Accounts receivable, net 1.3% 1.3% 1.2% 2.0% 2.3% 2.4% 2.5% 2.7%

Income taxes receivable 0.3% 0.1% 0.5% 0.2% 0.4% 0.2% 0.4% 0.3%

Inventories, net 34.5% 33.9% 38.0% 40.1% 40.5% 49.2% 43.7% 42.2%

Prepaid expenses and other current assets 2.2% 2.1% 2.6% 3.2% 2.7% 2.7% 2.4% 2.2%

Deferred income taxes 0.7% 0.4% 1.0% 1.3% 1.5% 1.2% 1.3% 1.2%

Total current assets 60.2% 62.4% 55.3% 52.7% 53.8% 57.5% 54.5% 53.4%

Property and equipment, net 26.4% 25.9% 29.1% 35.3% 35.0% 33.0% 35.7% 37.6%

Construction in progress --- leased facilities 0.0% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Intangible assets, net (inc. Goodwill) 9.7% 8.4% 10.4% 9.7% 9.0% 7.6% 8.0% 7.3%

Deferred income taxes 1.0% 0.4% 0.2% 0.1% 0.1% 0.0% 0.0% 0.0%

Other assets 2.7% 2.9% 5.1% 2.1% 2.0% 1.8% 1.8% 1.7%

Total assets 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Liabilities andStockholder's Equity

Current liabilities:

Accounts payable 17.2% 17.0% 17.6% 18.3% 17.9% 23.2% 22.5% 21.7%

Accrued expenses 10.8% 8.8% 9.3% 8.6% 8.3% 8.5% 9.2% 8.9%

Deferred revenue and other liabilities 4.7% 4.3% 5.1% 5.0% 5.0% 3.3% 4.8% 4.8%

Income taxes payable 0.0% 1.0% 2.4% 0.6% 1.4% 0.0% 1.2% 1.1%

Current portion of other long-termdebt and leasing obligations 0.0% 0.2% 0.3% 0.0% 0.0% 0.0% 0.0% 0.0%

Total current liabilities 32.7% 31.4% 34.7% 32.6% 32.6% 35.0% 37.7% 36.6%

Long-termliabilities:

Revolver 0.0% 0.0% 0.0% 0.0% 0.0% 8.4% 0.0% 0.0%

Long-termdebt and leasing obligations 5.4% 5.1% 0.3% 0.2% 0.2% 0.1% 0.1% 0.1%

Non-cash obligations for construction in progress --- leased facilities 0.0% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Deferred income taxes 0.0% 0.0% 0.3% 1.3% 1.3% 0.7% 1.1% 1.1%

Deferred revenue and other liabilities 9.5% 9.0% 9.9% 10.8% 12.7% 13.2% 13.3% 13.7%

Total long-termliabilities 14.8% 14.1% 10.4% 12.3% 14.1% 22.5% 14.6% 14.9%

Total liabilities 47.5% 45.5% 45.0% 44.9% 46.7% 57.5% 52.3% 51.5%

Stockholder's equity:

Common stock / additional paid-in capital 24.1% 23.4% 30.3% 31.3% 29.6% 26.0% 27.0% 25.6%

Class B common stock 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Retained earnings 28.1% 31.1% 31.6% 38.7% 42.8% 40.0% 45.4% 49.2%

Other comprehensive income / (loss) 0.3% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Treasury stock 0.0% 0.0% -6.9% -14.8% -19.1% -23.5% -24.6% -26.3%

Total stockholder's equity 52.5% 54.5% 55.0% 55.1% 53.3% 42.5% 47.7% 48.5%

Total liabilities andstockholder's equity 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

17. Appendix A-5: Balance Sheet as a Percentage of Revenue

Source: Company Filings & Analyst’s Estimates

BALANCESHEET AS % OF REVENUE

Fiscal year 2010A 2011A* 2012A* 2013A 2014A MRQ 2015P 2016P

Fiscal year end date 1/29/2011 1/28/2012 2/2/2013 2/1/2014 1/31/2015 10/31/2015 1/31/2016 1/31/2017

Assets

Current assets:

Cash and cash equivalents 11.2% 14.1% 5.9% 2.9% 3.3% 1.0% 2.2% 2.5%

Accounts receivable, net 0.7% 0.7% 0.6% 1.0% 1.2% 1.3% 1.3% 1.4%

Income taxes receivable 0.2% 0.1% 0.3% 0.1% 0.2% 0.1% 0.2% 0.2%

Inventories, net 18.4% 19.5% 18.8% 19.8% 20.4% 27.8% 22.9% 22.2%

Prepaid expenses and other current assets 1.2% 1.2% 1.3% 1.6% 1.3% 1.5% 1.2% 1.1%

Deferred income taxes 0.4% 0.2% 0.5% 0.6% 0.8% 0.7% 0.7% 0.6%

Total current assets 32.1% 35.8% 27.3% 26.1% 27.2% 32.4% 28.6% 28.1%

Property and equipment, net 14.1% 14.9% 14.4% 17.5% 17.7% 18.7% 18.7% 19.8%

Construction in progress --- leased facilities 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Intangible assets, net (inc. Goodwill) 5.2% 4.8% 5.1% 4.8% 4.6% 4.3% 4.2% 3.9%

Deferred income taxes 0.6% 0.2% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0%

Other assets 1.4% 1.7% 2.5% 1.1% 1.0% 1.0% 0.9% 0.9%

Total assets 53.3% 57.5% 49.5% 49.4% 50.4% 56.4% 52.4% 52.6%

Liabilities andStockholder's Equity

Current liabilities:

Accounts payable 9.2% 9.8% 8.7% 9.1% 9.0% 13.1% 11.8% 11.4%

Accrued expenses 5.7% 5.1% 4.6% 4.3% 4.2% 4.8% 4.8% 4.7%

Deferred revenue and other liabilities 2.5% 2.5% 2.5% 2.5% 2.5% 1.9% 2.5% 2.5%

Income taxes payable 0.0% 0.6% 1.2% 0.3% 0.7% 0.0% 0.6% 0.6%

Current portion of other long-termdebt and leasing obligations 0.0% 0.1% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0%

Total current liabilities 17.4% 18.0% 17.1% 16.1% 16.4% 19.8% 19.8% 19.2%

Long-termliabilities:

Revolver 0.0% 0.0% 0.0% 0.0% 0.0% 4.8% 0.0% 0.0%

Long-termdebt and leasing obligations 2.9% 2.9% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

Non-cash obligations for construction in progress --- leased facilities 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Deferred income taxes 0.0% 0.0% 0.1% 0.6% 0.7% 0.4% 0.6% 0.6%

Deferred revenue and other liabilities 5.0% 5.2% 4.9% 5.3% 6.4% 7.5% 7.0% 7.2%

Total long-termliabilities 7.9% 8.1% 5.1% 6.1% 7.1% 12.7% 7.7% 7.8%

Total liabilities 25.3% 26.2% 22.3% 22.2% 23.5% 32.5% 27.4% 27.1%

Stockholder's equity:

Common stock / additional paid-in capital 12.9% 13.4% 15.0% 15.4% 14.9% 14.7% 14.1% 13.5%

Class B common stock 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Retained earnings 15.0% 17.9% 15.6% 19.1% 21.6% 22.6% 23.8% 25.9%

Other comprehensive income / (loss) 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Treasury stock 0.0% 0.0% -3.4% -7.3% -9.6% -13.3% -12.9% -13.8%

Total stockholder's equity 28.0% 31.3% 27.2% 27.2% 26.9% 24.0% 25.0% 25.5%

Total liabilities andstockholder's equity 53.3% 57.5% 49.5% 49.4% 50.4% 56.4% 52.4% 52.6%

18. Appendix A-6: Financial Ratios

Source: Company Filings & Analyst’s Estimates

RATIO ANALYSIS

Fiscal year 2010A 2011A* 2012A* 2013A 2014A TTM 2015P 2016P Industry Avg.

Fiscal year end date 1/29/2011 1/28/2012 2/2/2013 2/1/2014 1/31/2015 10/31/2015 1/31/2016 1/31/2017

Profitability

Gross Profit Margin 29.7% 30.6% 31.5% 31.3% 30.6% 30.6% 30.6% 30.7% 39.7%

EBIT Margin 6.3% 8.3% 9.0% 8.6% 8.1% 8.0% 7.6% 7.5% 11.1%

EBITDA Margin 9.1% 11.0% 11.7% 11.6% 11.1% 10.9% 10.8% 10.7% 13.5%

PretaxProfit Margin 6.1% 8.0% 8.9% 8.8% 8.2% 8.0% 7.7% 7.6% 10.8%

Net Profit Margin 3.7% 4.9% 5.3% 5.4% 5.1% 5.0% 4.8% 4.7% 6.8%

Return on Assets 7.0% 8.5% 10.7% 11.0% 10.0% 8.8% 9.1% 8.9% 9.9%

Return on Equity 13.4% 15.6% 19.5% 20.0% 18.8% 20.7% 19.0% 18.4% 17.6%

Return on Invested Capital 12.6% 14.7% 19.4% 19.5% 18.7% 17.3% 18.8% 18.2% 16.1%

YOYGrowth in Revenue n/a 7.0% 12.0% 6.5% 9.7% n/a 8.5% 8.0% n/a

YOYGrowth in Net Income n/a 40.3% 21.2% 9.0% 2.0% n/a 2.1% 6.5% n/a

YOYGrowth in Diluted EPS n/a 35.8% 21.0% 9.3% 5.6% n/a 5.2% 10.3% n/a

Asset Management

Inventory Turnover 3.8 times 3.6 times 3.6 times 3.5 times 3.4 times 2.5 times 3.0 times 3.1 times 2.7 times

Average Collection Period 3 days 3 days 2 days 4 days 4 days 5 days 5 days 5 days 213 days

Fixed Asset Turnover 7.1 times 6.7 times 6.9 times 5.7 times 5.7 times 5.4 times 5.3 times 5.1 times 6.4 times

Total Asset Turnover 1.9 times 1.7 times 2.0 times 2.0 times 2.0 times 1.8 times 1.9 times 1.9 times 1.3 times

Leverage andLiquidity

Times Interest Earned 22.1 times 31.2 times 86.8 times 183.3 times 172.3 times 163.5 times 896.5 times 1105.0 times 192.0 times

Long-termDebt/Common Equity 10.3% 9.3% 0.5% 0.4% 0.3% 0.3% 0.3% 0.2% 14.0%

Debt-to-Invested Capital 9.3% 8.5% 0.5% 0.4% 0.3% 0.3% 0.3% 0.2% 18.0%

Total Debt Ratio 47.5% 45.5% 45.0% 44.9% 46.7% 57.5% 52.3% 51.5% 52.3%

Equity Multiplier 1.9 times 1.8 times 1.8 times 1.8 times 1.9 times 2.4 times 2.1 times 2.1 times 2.1 times

Current Ratio 1.8 times 2.0 times 1.6 times 1.6 times 1.7 times 1.6 times 1.4 times 1.5 times 3.5 times

Quick Ratio 0.7 times 0.8 times 0.4 times 0.2 times 0.3 times 0.1 times 0.2 times 0.2 times 1.6 times

Additional Ratios

Free Cash Flow Per Share n/a (0.34) 4.36 1.47 0.50 2.48 2.14 1.14 0.28

Dividend Yield (%) 0.0% 1.2% 5.2% 1.0% 1.0% 1.1% 1.0% 0.9% 0.0%

YOYGrowth in Dividends Per Share 0.0% 5000.0% 400.0% -80.0% 0.0% 10.0% 10.0% 0.0% 0.0%

Weighted-Average Cost of Capital 12.6% 11.5% 10.6% 10.4% 7.9%

BondRatings (list each bondissue andthe rating on the issue) n/a n/a n/a n/a n/a n/a n/a n/a n/a

19. Appendix A-6: Financial Ratios (cont.)

Source: Company Filings & Analyst’s Estimates

DuPont Analysis

Net profit margin 3.7% 4.9% 5.3% 5.4% 5.1% 5.0% 4.8% 4.7% 6.8%

Total asset turnover 1.9 times 1.7 times 2.0 times 2.0 times 2.0 times 1.8 times 1.9 times 1.9 times 1.3 times

Equity multiplier 1.9 times 1.8 times 1.8 times 1.8 times 1.9 times 2.4 times 2.1 times 2.1 times 2.1 times

Return on equity 13.4% 15.6% 19.5% 20.0% 18.8% 20.7% 19.0% 18.4% 18.6%

ExtendedDuPont Analysis

EBIT Margin 6.3% 8.3% 9.0% 8.6% 8.1% 8.0% 7.6% 7.5%

Total Asset Turnover 1.9 times 1.7 times 2.0 times 2.0 times 2.0 times 1.8 times 1.9 times 1.9 times

Equity Multiplier 1.9 times 1.8 times 1.8 times 1.8 times 1.9 times 2.4 times 2.1 times 2.1 times

Interest Burden 96.2% 96.8% 99.7% 101.7% 100.4% 99.6% 100.8% 100.8%

TaxBurden 61.2% 61.1% 59.3% 61.8% 61.9% 62.0% 62.0% 62.0%

Return on equity 13.4% 15.6% 19.5% 20.0% 18.8% 20.7% 19.0% 18.4%

Free Cash Flow

Net Income n/a 255,475 309,662 337,598 344,198 356,935 351,354 374,337

Plus: Depreciation & Amortization n/a 116,581 125,096 154,928 179,431 180,114 205,324 221,570

Less: Change in Working Capital n/a 212,460 (333,126) 22,363 114,067 89,988 (79,631) 51,476

Less: Capital Expenditures n/a 201,807 219,026 285,668 349,007 154,785 384,473 415,231

Free Cash Flow n/a (42,211) 548,858 184,495 60,555 292,276 251,836 129,201

20. Appendix B-1: Multiples Justification

Justified P/E

Our P/E used for valuation purposes is 14.0 times. Dick’s TTM P/E is 12.78. We adjusted our P/E higher than that

of the TTM for a number of reasons. First, we believe Dick’s stock is trading at a discount right now. In tandem

with other retailers, Dick’s stock price has fallen considerably in the last month, further pushing their stock down,

which was due to poor performance in the third quarter. Dick’s management had stated the main reason for this was

an unexpected warmer climate that impacted cold weather apparel and hunting equipment sales. We believe that

this is not an event that will occur with any sort of regularity. However, because it does expose Dick’s weakness to

unexpected weather changes, we still believe that in the future, investors will not be willing to pay as much for DKS

stock as they have in the past. Historically, their stock has been trading at 21.45 times. This accounts for years

when Dick’s was growing at a much more rapid pace than they are and does not reflect their current situation. It

also does not reflect what investors are willing to pay for comparable companies. Hibbett Sports’ TMM P/E is

11.48 and Cabela’s TTM P/E is 17.01, where Hibbett Sports is a closer comparison to DKS. Thus, because Dick’s

is not growing as fast as they have been in the past and they are currently have some troubles along with the rest of

the retail sector, we believe that investors will only be willing to pay a slight amount more for their stock in 14

months (14.0 vs. 12.78).

EV/EBITDA

The EV/EBITDA multiple we have used for valuation purposes is 8.0 times. In this case we decided to use a

conservative estimate. Dick’s TTM EV/EVBITDA is 7.93 and Hibbett Sports’ TTM EV/EBITDA is 8.04. They are

trading lower than both their three year and five year EV/EBITDA historical averages. We believe Dick’s EBIT

margins have upside potential because we are convinced that their growth strategy has positioned themselves better

than competitors in the future. However, there is a fair amount of risk in them being able to generate their expected

profits from the new stores they have been opening. Thus, we applied a conservative estimate of 8.0 times to reflect

the risk of Dick’s aggressive expansion potentially being impacted by increasing competition from companies with

larger brand power and weaker consumer spending.

Weighted-Average Target Price

Our target price per share of $49.27 is a function of a weighted average of both valuation metrics. We weighted P/E

valuation at 75% and EV/EBITDA valuation at 25%. We weighted P/E valuation much higher because we view its

target price as being more realistic. With a consensus target price of $46.74 and the highest analyst target price

being $55 (based on revised target prices after weak Q3), a target price of $58.82 reached with our EV/EBITDA

valuation seemed much too high. P/E valuation returned a target price of $46.09, which we believe is much more

reasonable. In addition, we expect that investors could be wary of investing in retail stocks given recent negative

news and that our P/E valuation reflects this better than EV/EBITDA valuation.

21. Appendix B-2: EPS Justification

Diluted EPS

Our forecasted diluted earnings per share for FY 2016 is $3.29. This is lower than consensus EPS, but is higher than

average broker analyst’s estimates of EPS of $3.26 (after Nov 17). We chose to compare to both consensus EPS and

broker analyst’s estimates of EPS after Nov 17 because Dick’s third quarter earnings came out the morning of Nov

17. Before earnings release, many analysts had projected EPS for FY 2016 between $3.50 and $3.60. Sharp

downward revisions were made after the company downgraded its FY 2015 EPS guidance from a range of $3.13 -

$3.21 to a range of $2.85 - $3.00. This made a substantial difference in our EPS estimates as well. In addition to

management lowering EPS guidance for FY 2015, we believe a big driver for the lowering of many other analyst’s

estimates was the anticipated pressure on profit margins. Management had stated that the fourth quarter would be a

more promotional environment and in the past, promotional costs have put a damper on margins even in the

presence of gains from shifting to a higher margin product mix. After earnings were released, we made adjustments

to both gross and SG&A margins to reflect our takeaways from the earnings report, which made our forecasted EPS

relatively close in-line with those of other analysts.

22. Appendix B-3: Income Statement Assumptions

Income Statement Assumptions 2015P 2016P

Revenue Growth 8.5% 8.0%

Gross Profit Margin 30.6% 30.7%

SG&A Margin 22.5% 22.7%

Pre-opening Expenses as a % of Sales 0.5% 0.5%

Marginal Tax Rate 38.0% 38.0%

Source: Analyst’s Calculations

Revenue Growth: our forecasts shows strong revenue growth in FY 2015 and FY 2016, although at a decreasing

rate. We believe revenue growth will remain strong because of how DKS has improved their brand power and

online presence, giving them some protection from increased competition. However, competition is increasing and

will likely have some impact, especially on new stores where Dick’s brand is less established. Thus, we have stated

revenue at a declining rate. This is fairly in-line with consensus revenue estimates for FY 2016. Our model

forecasts $7.985B in FY 2016 while consensus estimates are at $7.933B.

Gross Profit Margin: forecasts for gross profit margins show only a marginal increase. After DKS third quarter

earnings release, they had discussed a more promotional environment in the coming months to get rid of their

inventory that had piled up because of unanticipated weather conditions. Although we still believe their shift in

product mix to higher margin apparel and footwear is a good move, it does come with risks. In their most recent 10-

K, they had cited promotional costs as being a big factor in offsetting gains from improvements in sales mix. We

believe they will be more profitable over a longer horizon, but in 14 months, we expect the build-up of inventory

and the promotional activity will put downward pressure on margins, especially because colder weather apparel

tends to be higher margin goods and future weak consumer spending could result in more promotional activity.

SG&A Margin: major expenses for Dick’s in this line item include advertising, marketing, and payroll costs. We

forecasted an increase for selling, general, and administrative expenses as a percentage of sales because as they

expand away from the southeast where their brand is strong, there is the risk that their stores won’t be as productive

and more advertising efforts may need to be put into place to get more production out of them.

Pre-opening Expenses as a % of Sales: this line item mainly includes marketing and payroll costs incurred before

a store is opened. In accordance with their growth strategy, we forecasted increases in pre-opening expenses

roughly similar to the increases they’ve had in the past, demonstrating steady growth in number of stores.

23. Appendix B-3: Income Statement Assumptions (cont.)

Marginal Tax Rate: we forecasted a tax rate of 38.0%. This is in-line with what they have paid in the trailing

twelve months.

24. Appendix B-4: Other Key Modeling Assumptions

Treasury Stock: for our treasury stock schedule, we have forecasted $300M of stock repurchases in FY 2015 and

$150M of stock repurchases in FY 2016. In March of 2013, Dick’s authorized a five year, one billion dollar share

repurchase program. As of Q3 in FY 2015, Dick’s has spent $300M in stock repurchases. Because of their recent

struggles, we do not foresee more buybacks in the period as $300M in one fiscal year already surpasses any of their

previous amounts. The amount remaining in their five year repurchase program is $245M. In FY 2016, we

forecasted that DKS would repurchase $150M in common stock as they’re share price is trading significantly lower

than their high of approximately $60 in 2016. We believe they would repurchase a significant amount as they could

buy back their stock at a relatively discounted price to reward shareholders, leaving approximately $100M left on

their repurchase program.

Revolver: in the most recent quarter, Dick’s had $342,400,000 in outstanding debt on their revolving credit facility.

Our forecast shows them ending FY 2015 with a zero balance as stated by management. For the following year in

FY 2016, we also forecast a zero balance for year end, staying consistent the company’s historical use of their

revolver.

26. Appendix B-6: Earnings Growth Rate Estimate Applied to Current Earnings

DKS Historical EPS Data

Fiscal Year EPS 1 Yr. Growth Rate

2014 $2.84 5.6%

2013 $2.69 28.1%

2012 $2.10 40.0%

2011 $1.50 30.4%

2010 $1.15 419.4%

2009 ($0.36) (127.1%)

2008 $1.33 31.68%

2007 $1.01 48.53%

2006 $0.68 6.25%

2005 $0.64 156.0%

2004 $0.25 n/a

Source: Bloomberg and Analyst’s Calculations

4 Yr. EPS Growth = 26.03%

EPS2016 = 2.84 (1+0.2603)14/12

= $3.72 (4 Yr. EPS growth rate applied to current EPS)

Note: Only four years of historical data were included in EPS growth rate calculations. The growth rate in 2010 is

skewed because of how poorly Dick’s performed after the recession. Prior to 2010, their growth rates were very

sporadic. Thus, we believe that only the past four years of data have real meaning.

27. Appendix B-7: Comparative Analysis of P/E Ratios

P/E Multiple

TTM P/E – DKS 12.78

TTM P/E – HIBB 11.48

TTM P/E – CAB 17.01

Historical Average P/E – DKS 21.45

Historical Average P/E – HIBB 20.25

Justified P/E 14.00

Source: Bloomberg & Analyst’s Calculations

Note: For comparative analysis of P/E ratios, we focused on what investors are willing to pay for Dick’s Sporting

Goods and their competitors most recently, and what investors are willing to pay for Dick’s and their closest

competitor historically. We chose to closely look at what investors are willing to pay for DKS and comparable

companies most recently because retail, in general, have been hit pretty hard by the market recently. Many major

retailers have reported sour earnings and that has had an impact on Dick’s and Hibbett Sports particularly. To a

lesser degree, we considered what investors are willing pay to for Dick’s and their closest competitor on a historical

basis because today’s prices are trading at a discount. However, because we believe that investor expectations of

retail stocks will remain fairly low, but we placed more weight on TTM P/E ratios.

28. Appendix B-8: Comparative Analysis of EV/EBITDA Ratios

EV/EBITDA Comparison

TTM EV/EBITDA – DKS 7.93

TTM EV/EBITDA – HIBB 8.04

Historical 3 Yr. Average EV/EBITDA – DKS 8.46

Historical 3 Yr. Average EV/EBITDA – HIBB 9.67

Justified EV/EBITDA 8.00

Source: Bloomberg & Analyst’s Calculations

Note: For EV/EBITDA ratios we placed most of our emphasis on comparing Dick’s Sporting Goods to Hibbett

Sports. Cabela’s, although a competitor in the industry, sells a much larger proportion of outdoor equipment. Thus,

aside from a few similarities, they face a different set of risks to operating profits than Dick’s and Hibbett Sports do.

As a conservative estimate, we estimated closer to TTM EV/EBITDA between both DKS and HIBB because we

Dick’s current performance will be closer to future performance than an average of performance from three years

ago. Dick’s EBITDA margins peaked in 2012 and have declined steadily since then.

29. Appendix B-9: Target Price Estimates

Broker Analyst Target Price Estimates

Firm Analyst Date Target Price

Stifel David A Shick 11.19.15 $46

Monness, Crespi, Hardt & Co Jim Chartier 11.19.15 $45

Morgan Stanley Simeon Gutman 11.18.15 $44

Goldman Sachs Stephen Tanal 11.18.15 $49

Brean Capital LLC Eric B Tracy 11.18.15 $44

UBS Michael Lasser 11.18.15 $43

Stephens Inc Rick Nelson 11.18.15 $42

Canaccord Genuity Camilo R Lyon 11.18.15 $46

Barclays Matthew McClintock 11.18.15 $50

Tesley Advisory Group Joseph I Feldman 11.18.15 $50

BMO Capital Markets Wayne Hood 11.17.15 $48

RBC Capital Markets R Scot Ciccarelli 11.17.15 $45

Credit Suisse Seth Sigman 11.17.15 $40

SunTrust Robinson Humphrey David G Magee 11.17.15 $43

J.P Morgan Christopher Horvers 11.17.15 $41

Robert Baird Peter S Benedict 11.17.15 $42

Sterne Agee CRT Sam Poser 11.17.15 $55

Cowen John Kernan 11.17.15 $43

Susquehanna Financial Christopher Svezia 11.17.15 $53

Wolfe Research Aram Rubinson 11.17.15 $32

Argus Research Corp Christopher Graja 08.26.15 $63

Imperial Capital LLC John O’Neil 07.08.15 $62

Source: Bloomberg

Note: Third quarter results were reported November 17, 2015

Consensus Target Price = $46.74

High (Date ≥ Nov 17) = $55

Average Target Price (Date ≥ Nov 17) = $45.05

Low (Date ≥ Nov 17) = $32

Our Target Price = $49.27

30. Appendix B-10: Valuation Template

Source: Analyst’s Calculations

Valuation Date November 20, 2015

Target Date January 31, 2017

Expected Diluted EPS $3.29 Method Value Weight Product

Justified P/E 14.0 P/E Multiple 46.09$ 75% 34.57

Target Price 46.09$ EV/EBITDA Multiple 58.82$ 25% 14.70

Target Price Per Share 49.27$

Expected EBITDA 851,461$ Risk-free rate 3.02%

Justified EV/EBITDA 8.0 Market risk premium 6.7%

Enterprise Value 6,811,689$ Beta 0.93

Required Rate of Return 9.3%

Size Premium 1.01%

Current portion of L-T debt - Required Return Adjusted for Size 10.3%

Current portion of capital leases 950

Short termdebt -

Long termdebt - Target Price 49.27$

Capital leases 4,163 Required Return 10.3%

Minority interest - Number of months to discount 14

Preferred stock - Current value $43.97

Other -

Less: Excess cash 118,421

Less: Investment securities - Current Stock Value $43.97

Less: Other Nonoperating assets - Current Stock Price 38.90$

Less: Equity investments - Margin of Safety 13.0%

Net Debt 123,534$

Enterprise Value 6,811,689

Less: Net Debt (123,534)

Equity Value 6,688,156$

Equity Value 6,688,156

Shares outstanding 113,706

Equity value / share 58.82$

Current Value Calculation

Margin of Safety Calculation

Calculation of Equity Value

Calculation of Equity Value per Share

Valuation Basedon P/E Targe Price Calculation

Valuation Basedon EV/EBITDA

Calculation of Enterprise Value Estimating RequiredRate of Return on Equity

Calculation of ExpectedNet Debt