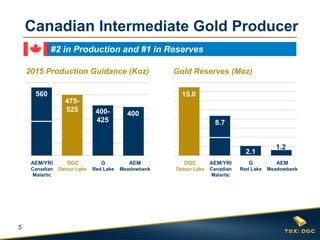

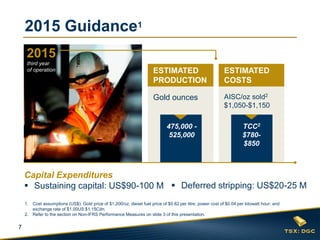

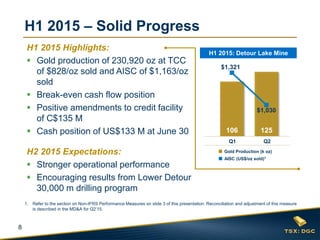

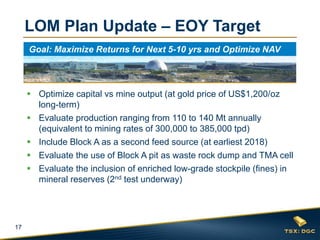

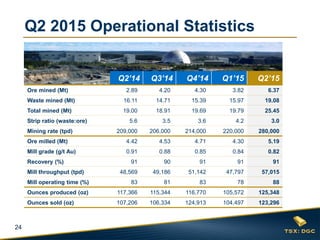

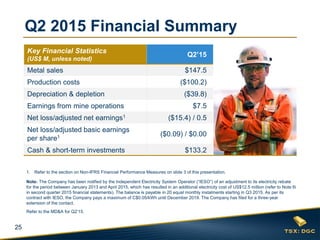

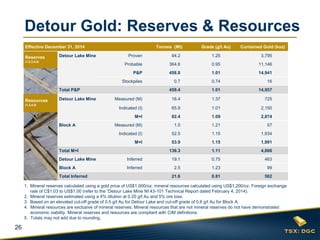

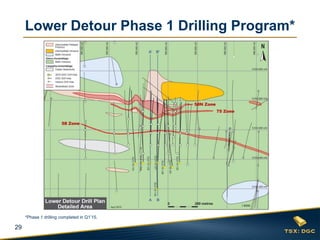

Detour Gold Corporation is Canada's second largest gold producer and has the largest gold reserves in Canada. The document provides Detour Gold's 2015 production guidance of 475,000-525,000 ounces of gold at a total cash cost of $780-$850 per ounce and all-in sustaining costs of $1,050-$1,150 per ounce. It also outlines Detour Gold's key drivers for success in 2015, including execution of its plan to increase gold production through higher mining and milling rates and strengthening its balance sheet. Near to long-term value enhancements include plant optimization, development of the Block A deposit, and exploration potential.