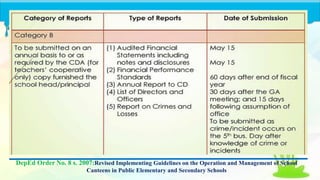

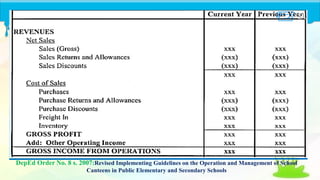

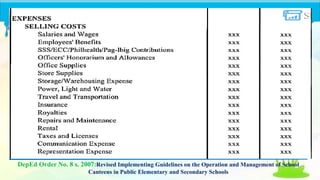

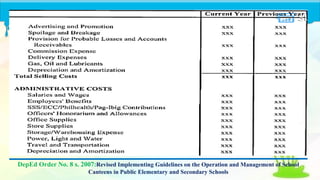

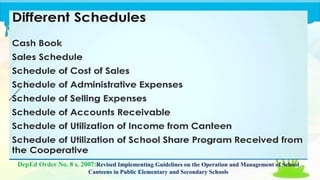

Download as PDF, PPTX

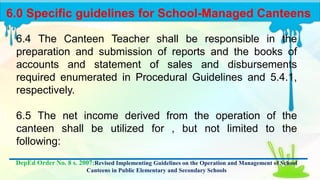

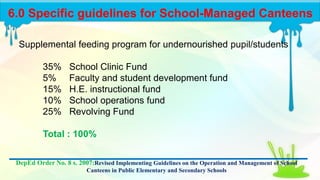

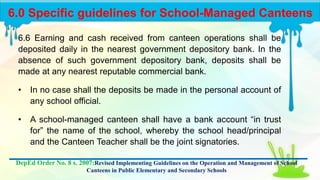

DepEd Order No. 8 s. 2007 provides revised guidelines for the operation and management of school canteens in public elementary and secondary schools, emphasizing the importance of eliminating malnutrition among students. The guidelines establish a structure for accountability, financial reporting, and management practices, detailing procedures for both school-managed and teachers' cooperative-managed canteens. Proceeds from canteen operations are to be utilized for student welfare programs, with specific allocations outlined for different purposes.