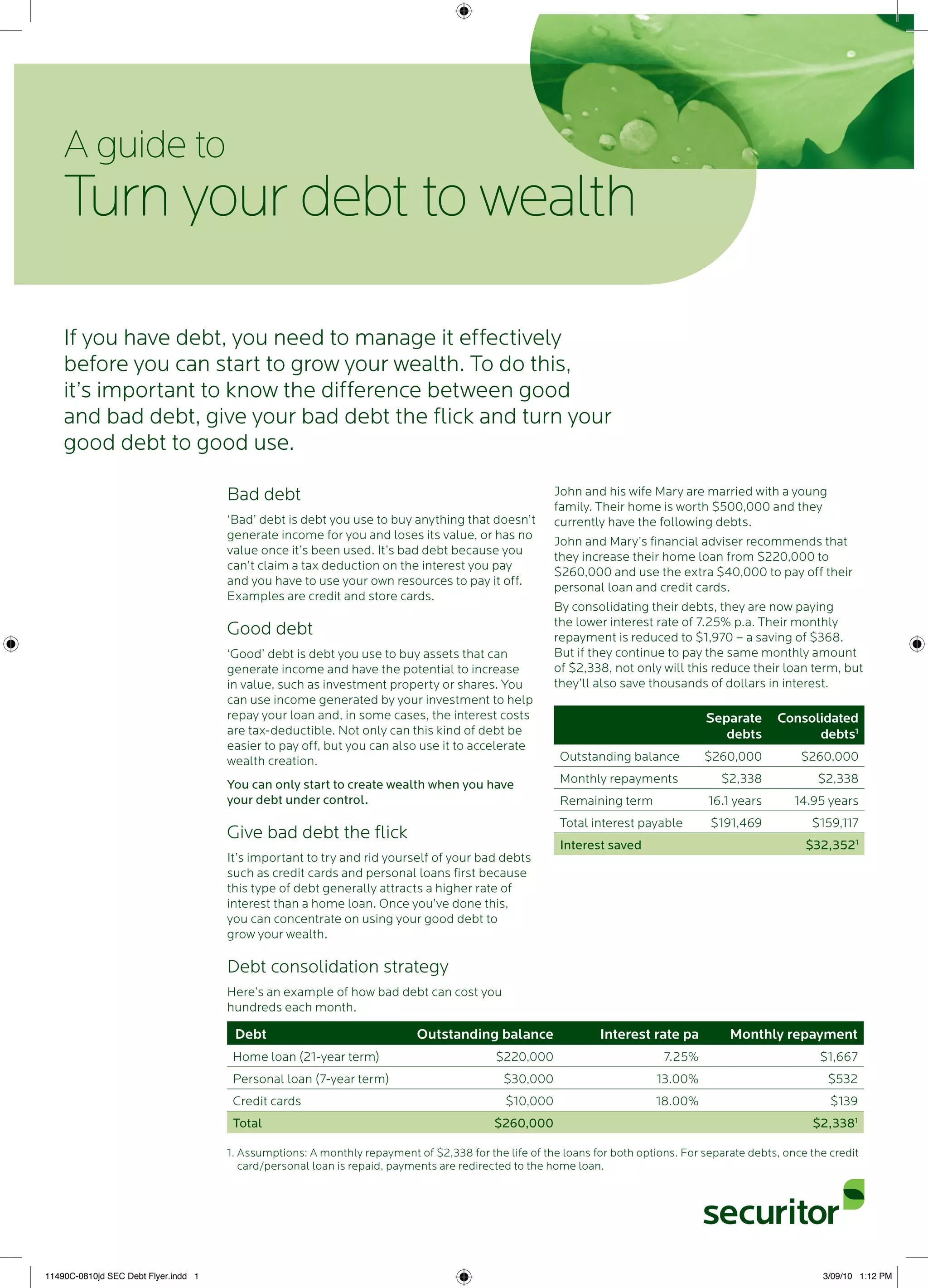

Download to read offline

The document explains the distinction between 'bad debt', which incurs high interest and does not generate income, and 'good debt', which is used for investment purposes and can lead to wealth creation. It emphasizes the importance of eliminating bad debts first and managing debts effectively through strategies like debt consolidation and debt recycling to accelerate wealth growth. Additionally, it outlines the benefits of using a mortgage offset account versus a conventional bank account for savings and the concept of gearing for investment purposes.

![Banking Strategies 8 09[1]](https://cdn.slidesharecdn.com/ss_thumbnails/bankingstrategies8091-12530535974621-phpapp03-thumbnail.jpg?width=640&height=640&fit=bounds)