We come toyou in prayer this afternoon. We pray that

you guide us and lead us in your way. We thank you for

being our protector and our provider. We ask for your

strength and wisdom to get through the day.

We pray for those who are sick, or hurting, or lonely, that

they may feel your love through the prayers of others.

We pray for those who are lost and searching that they may

find their way home.

We pray for those who are grieving that they may find

peace in knowing their loved one is happy with you now.

And we pray that we can show love to each other

today, even if it is difficult at times.

In Jesus name we pray, Amen

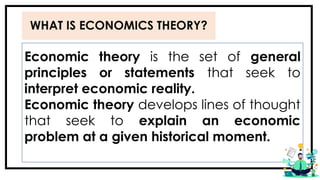

WHAT IS ECONOMICSTHEORY?

Economic theory is the set of general

principles or statements that seek to

interpret economic reality.

Economic theory develops lines of thought

that seek to explain an economic

problem at a given historical moment.

8.

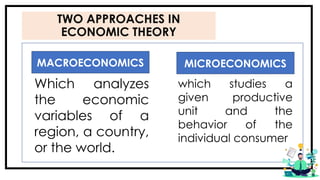

TWO APPROACHES IN

ECONOMICTHEORY

MACROECONOMICS MICROECONOMICS

Which analyzes

the economic

variables of a

region, a country,

or the world.

which studies a

given productive

unit and the

behavior of the

individual consumer

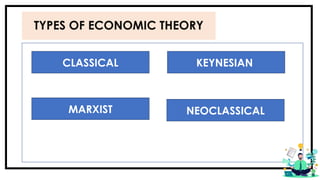

WHAT IS CLASSICALTHEORY?

• Classical economic theory tends to favor a free market

system.

• This theory-based its positions on the empirical study of

reality, formulating conceptual models through which

they enunciated natural laws.

• The areas of interest of this theory were the groups or

classes of individuals, the study of the wages received by

workers, and the wealth of nations through the generation

of value not paid to the worker that the employer or

capitalist received ( surplus value ).

11.

WHAT IS CLASSICALTHEORY?

• Classical economists believe that individuals

allowed to act in their self-interests will present a

strong group of consumers.

• Terms like capitalism and supply-

side economics also describe this theory.

• The protection of personal property through courts

of law is often a major component of free-market

economics.

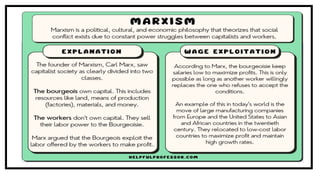

WHAT IS MARXISTTHEORY?

• Created by the philosopher,

sociologist, and economist Karl

Marx this theory was based on

the search for equality of

social classes, where the

proletariat should have the

same benefits and rights as the

rest of society.

14.

WHAT IS MARXISTTHEORY?

• a set of ideas and beliefs that are dominant in society and are

used to justify the power and privilege of the ruling class.

15.

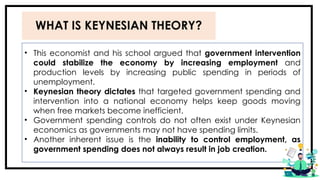

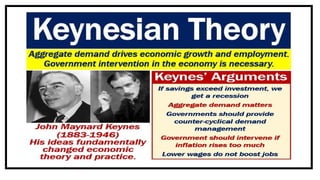

WHAT IS KEYNESIANTHEORY?

• This economist and his school argued that government intervention

could stabilize the economy by increasing employment and

production levels by increasing public spending in periods of

unemployment.

• Keynesian theory dictates that targeted government spending and

intervention into a national economy helps keep goods moving

when free markets become inefficient.

• Government spending controls do not often exist under Keynesian

economics as governments may not have spending limits.

• Another inherent issue is the inability to control employment, as

government spending does not always result in job creation.

17.

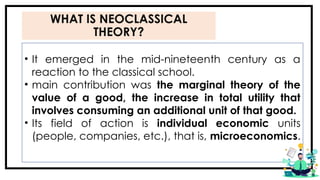

WHAT IS NEOCLASSICAL

THEORY?

•It emerged in the mid-nineteenth century as a

reaction to the classical school.

• main contribution was the marginal theory of the

value of a good, the increase in total utility that

involves consuming an additional unit of that good.

• Its field of action is individual economic units

(people, companies, etc.), that is, microeconomics.

18.

WHAT IS ECONOMICMODEL?

Economic model is a theoretical construct that

represents a process by several variables and a

set of quantitative or logical relationships

between them – to determine what might

happen in different scenarios or at a future date.

An economic model is a simplified representation

of economic processes and relationships.

ELEMENTS OF ECONOMIC

MODEL

ASSUMPTIONS

•Since a model is a simplification, to create a model, it’s

necessary to make assumptions.

• Examples of assumptions usually made by economists

are rational expectations or perfect information.

• The assumptions cannot contradict each other.

• One must be careful to choose the right model for the

right task.

21.

ELEMENTS OF ECONOMIC

MODEL

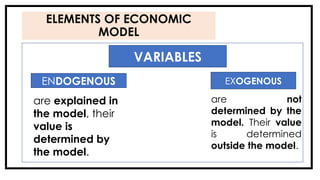

VARIABLES

ENDOGENOUSEXOGENOUS

are explained in

the model, their

value is

determined by

the model.

are not

determined by the

model. Their value

is determined

outside the model.

22.

ELEMENTS OF ECONOMIC

MODEL

RELATION

•Variables are related to each other.

• Relations are usually shown using mathematical

formulas.

• If the value of the variable changes, it usually

affects the value of other variables in the model.

24.

How does anassumption

affect the economic

status of a state? Justify

your answer.