More Related Content

Similar to Daily livestock report july 26 2012

Similar to Daily livestock report july 26 2012 (18)

More from joseleorcasita

More from joseleorcasita (20)

Daily livestock report july 26 2012

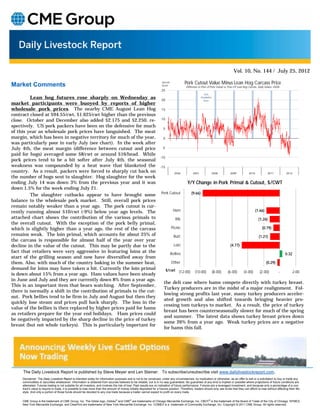

- 1. Vol. 10, No. 144 / July 25, 2012 Market Comments s pread $/cwt Pork Cutout Value Minus Lean Hog Carcass Price Difference in Price of Pork Cutout vs. Price Of Lean Hog Carcass, Daily Values, USDA 25 Jul y Lean hog futures rose sharply on Wednesday as 20 s ha ded in bl ue market participants were buoyed by reports of higher wholesale pork prices. The nearby CME August Lean Hog 15 contract closed at $94.55/cwt, $1.625/cwt higher than the previous close. October and December also added $2.175 and $2.250, re- 10 spectively. US pork packers have been on the defensive for much 5 of this year as wholesale pork prices have languished. The meat margin, which has been in negative territory for much of the year, 0 was particularly poor in early July (see chart). In the week after July 4th, the meat margin (difference between cutout and price -5 paid for hogs) averaged some $8/cwt or around $16/head. While -10 pork prices tend to be a bit softer after July 4th, the seasonal weakness was compounded by a heat wave that blanketed the -15 country. As a result, packers were forced to sharply cut back on 2006 2007 2008 2009 2010 2011 2012 the number of hogs sent to slaughter. Hog slaughter for the week ending July 14 was down 3% from the previous year and it was Y/Y Change in Pork Primal & Cutout, $/CWT down 1.5% for the week ending July 21. Pork Cutout (9.66) The slaughter cutbacks appear to have brought some balance to the wholesale pork market. Still, overall pork prices remain notably weaker than a year ago. The pork cutout is cur- rently running almost $10/cwt (-9%) below year ago levels. The Ham (1.66) attached chart shows the contribution of the various primals to Rib (1.26) the overall cutout. With the exception of the pork belly primal, which is slightly higher than a year ago, the rest of the carcass Picnic (0.79) remains weak. The loin primal, which accounts for about 25% of Butt (1.21) the carcass is responsible for almost half of the year over year decline in the value of the cutout. This may be partly due to the Loin (4.77) fact that retailers were very aggressive in featuring loins at the Bellies 0.32 start of the grilling season and now have diversified away from them. Also, with much of the country baking in the summer heat, Other (0.29) demand for loins may have taken a hit. Currently the loin primal $/cwt (12.00) (10.00) (8.00) (6.00) (4.00) (2.00) - 2.00 is down about 15% from a year ago. Ham values have been steady in June and July and they are currently down 8% from a year ago. the deli case where hams compete directly with turkey breast. This is an important item that bears watching. After September, Turkey producers are in the midst of a major realignment. Fol- there is normally a shift in the contribution of primals to the cut- lowing strong profits last year, many turkey producers acceler- out. Pork bellies tend to be firm in July and August but then they ated growth and also shifted towards bringing heavier pro- quickly lose steam and prices pull back sharply. The loss in the cessing tom turkeys to market. As a result, the price of turkey value of the bellies is then replaced by higher prices paid for hams breast has been counterseasonally slower for much of the spring as retailers prepare for the year end holidays. Ham prices could and summer. The latest data shows turkey breast prices down be negatively impacted by the sharp decline in the price of turkey some 26% from a year ago. Weak turkey prices are a negative breast (but not whole turkeys). This is particularly important for for hams this fall. The Daily Livestock Report is published by Steve Meyer and Len Steiner. To subscribe/unsubscribe visit www.dailylivestockreport.com. Disclaimer: The Daily Livestock Report is intended solely for information purposes and is not to be construed, under any circumstances, by implication or otherwise, as an offer to sell or a solicitation to buy or trade any commodities or securities whatsoever. Information is obtained from sources believed to be reliable, but is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. Futures trading is not suitable for all investors, and involves the risk of loss. Past results are no indication of future performance. Futures are a leveraged investment, and because only a percentage of a con- tract’s value is require to trade, it is possible to lose more than the amount of money initially deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their life- style. And only a portion of those funds should be devoted to any one trade because a trader cannot expect to profit on every trade. CME Group is the trademark of CME Group, Inc. The Globe logo, Globex® and CME® are trademarks of Chicago Mercantile Exchange, Inc. CBOT® is the trademark of the Board of Trade of the City of Chicago. NYMEX, New York Mercantile Exchange, and ClearPort are trademarks of New York Mercantile Exchange. Inc. COMEX is a trademark of Commodity Exchange, Inc. Copyright © 2011 CME Group. All rights reserved.