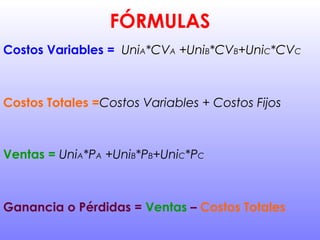

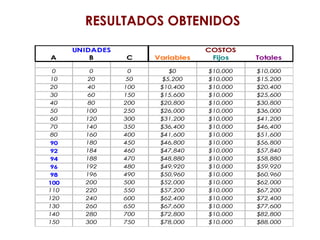

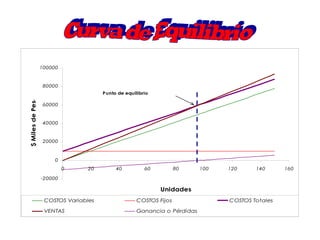

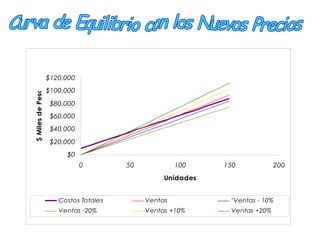

The document analyzes the costs, sales, and break-even point of a company that produces three products (A, B, C) under different production quantities and pricing scenarios. It provides the formulas used to calculate variable costs, total costs, sales, and profits. Tables of results show the costs, sales, profits/losses, and break-even point across different production levels. The conclusion states that increasing prices raises sales volumes needed to reach the break-even point, while decreasing prices lowers sales and requires higher production to break even.