Download to read offline

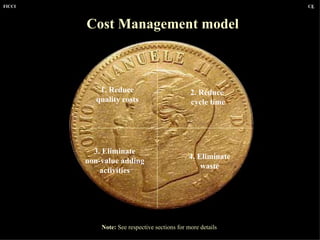

The document discusses the differences between cost management and cost cutting. It presents a 4-point cost management model focusing on reducing quality costs, cycle time, and non-value adding activities and eliminating waste. The document emphasizes that organizations should practice efficient cost management, not cost cutting, as the latter can lead to quality problems. Cost management aims to improve efficiency rather than simply reduce costs.