Download to read offline

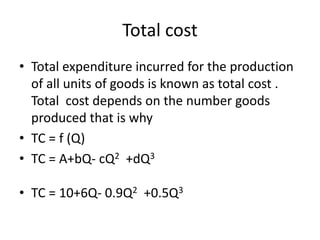

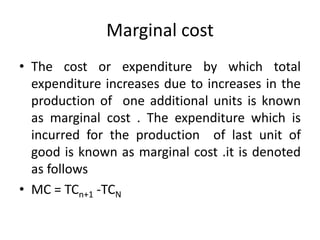

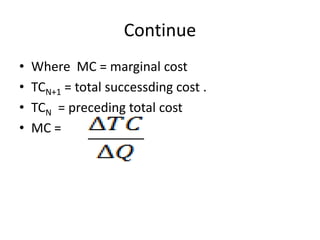

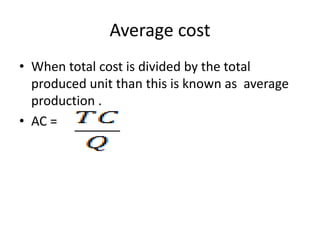

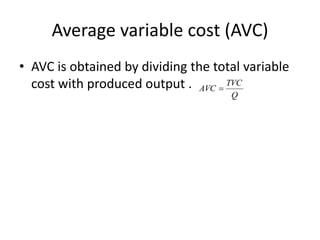

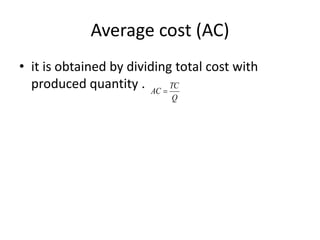

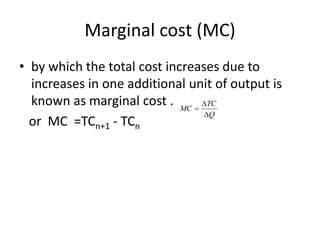

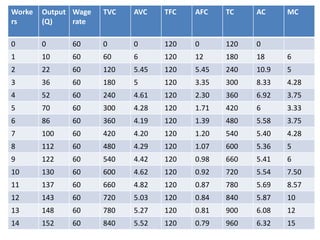

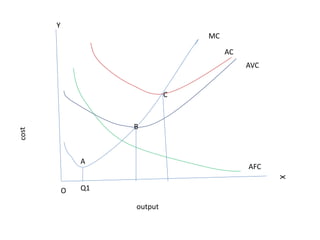

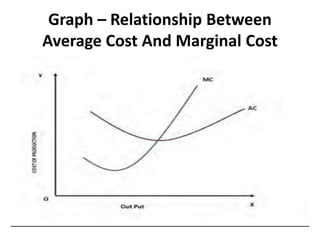

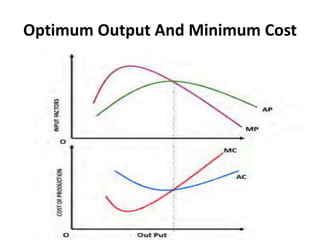

The document discusses various cost concepts including: - Total cost, average cost, and marginal cost. Total cost depends on quantity produced, average cost is total cost divided by quantity, and marginal cost is the change in total cost from producing one additional unit. - Fixed and variable costs. Fixed costs do not change with quantity while variable costs do. Short-run costs include both. - Other concepts like opportunity cost, sunk costs, accounting costs, and more. Cost curves are also discussed showing the relationships between costs and quantity.