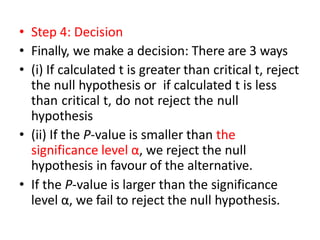

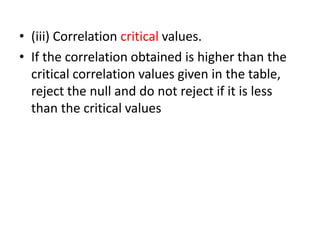

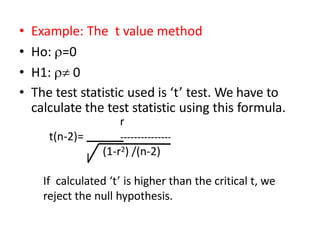

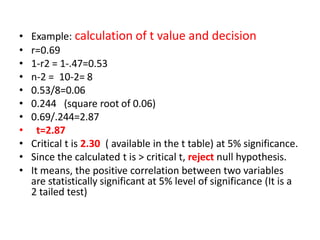

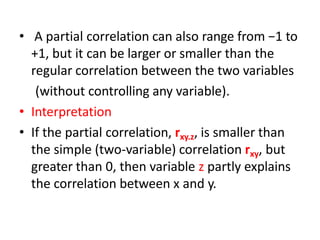

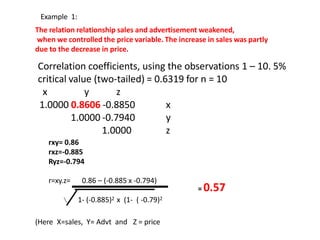

Download to read offline

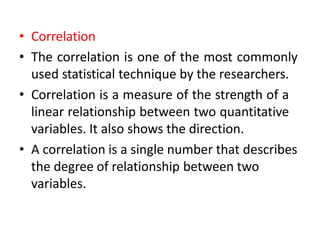

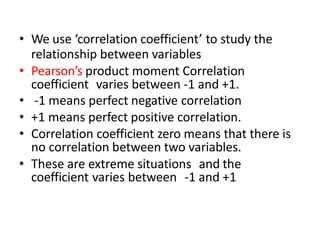

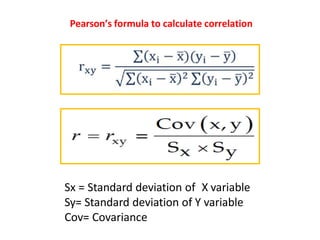

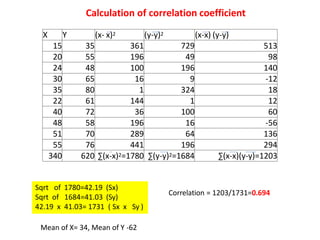

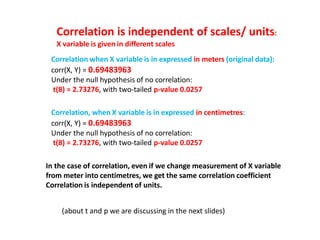

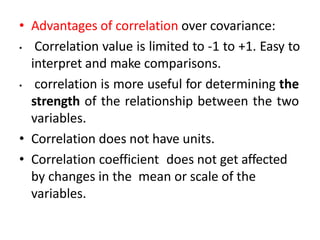

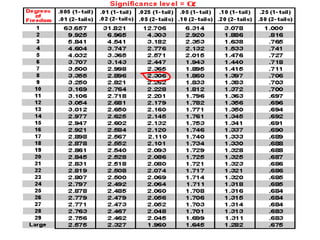

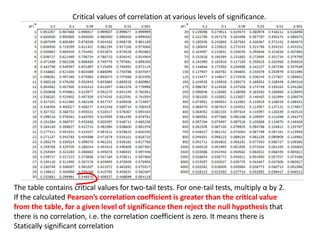

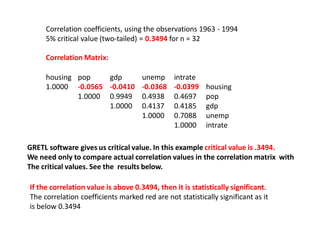

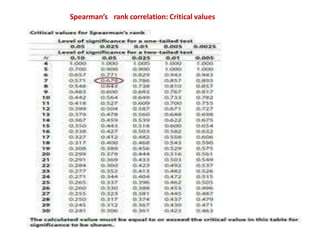

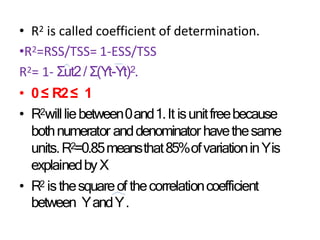

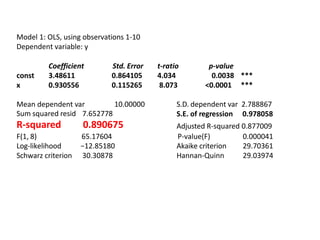

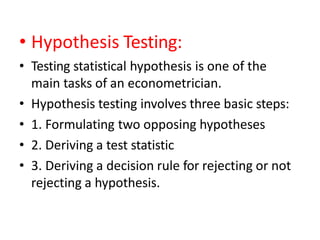

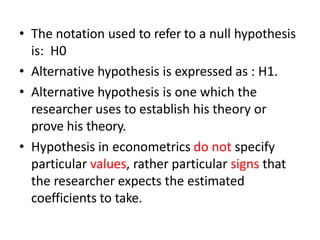

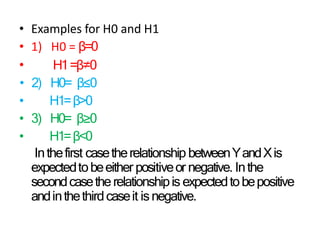

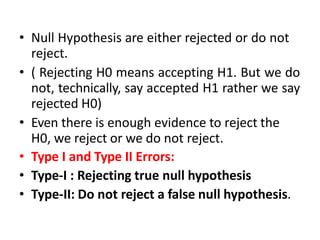

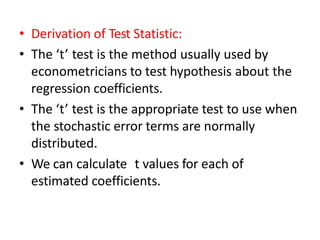

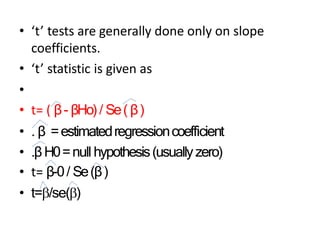

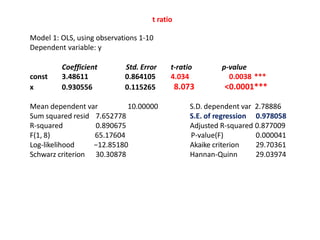

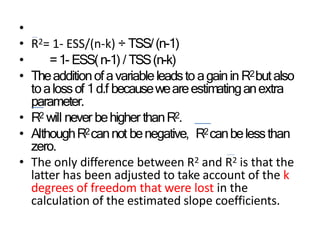

This document discusses correlation and related statistical concepts. Correlation measures the strength and direction of association between two quantitative variables. A correlation of 0 means no association, 1 means perfect positive association, and -1 means perfect negative association. Correlation is independent of measurement units and scaling of variables. Hypothesis testing is used to make inferences about the population correlation based on a sample correlation. The null hypothesis is that the population correlation is 0, and alternative hypotheses specify a non-zero correlation. The test statistic used is Student's t distribution. The null is rejected if the calculated t exceeds the critical value or if the p-value is less than the significance level.

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)