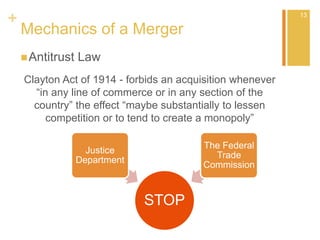

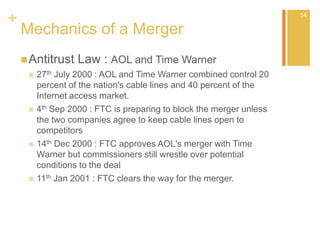

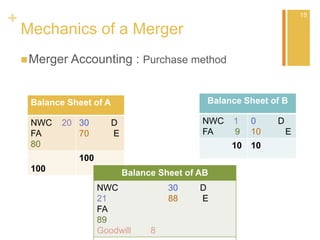

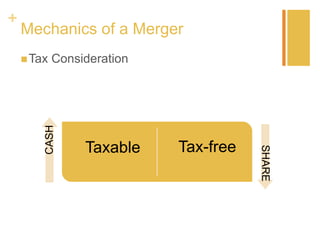

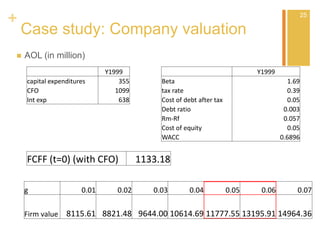

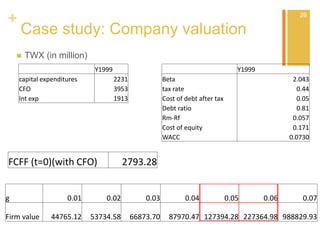

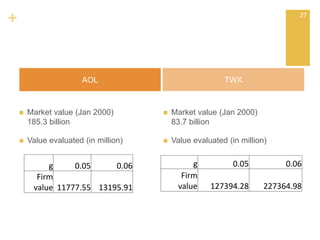

This document provides an overview of the principles of valuation for mergers and acquisitions. It discusses key terms like mergers, acquisitions, and types of M&A deals. It also outlines common motives for M&A like strategic gains, financial benefits, and managerial motives. The mechanics of an M&A deal including antitrust laws and accounting treatment are summarized. The document uses the AOL-Time Warner merger as a case study, outlining the motives and valuation of the two companies at the time of the announced deal.

![+

Reference

Website

Hewlett-Packard (2001) Hewlett-Packard and Compaq agree to merge, creating $87 billion global technology leader,

Available from http://www8.hp.com/us/en/hp-news/press-release.html?id=230610#.U3-QKFiSxy8 [Accessed 21 May

2014]

Investopedia (2009) The wonderful world of Mergers , Available from

http://www.investopedia.com/articles/stocks/09/merger-acquisitions-types.asp [Accessed 15 May 2014]

Washingtonpost (2005) Timeline: AOL and Time Warner, Available from http://www.washingtonpost.com/wp-

dyn/content/article/2005/10/28/AR2005102800747_pf.html [Accessed 20 May 2014]

Federal Communications Commission (2014) America Online-Time Warner Merger Page, Available from

http://www.fcc.gov/encyclopedia/america-online-time-warner-merger-page [Accessed 20 May 2014]

Boston College (2005) Valuation Techniques, Available from

http://www.bc.edu/clubs/bcfa/docs/vault/Valuation%20Techniques.pdf [Accessed 23 May 2014]

CFA Institute (2010) Free Cash Flow Valuation, Available from

http://www.cfainstitute.org/learning/products/publications/inv/Documents/equity_chapter4.pptx [Accessed 21 May 2015]

Business Insider (2009) Chart of the day: AOL Time Warner’s Marriage Made in Hell, Available from

http://www.businessinsider.com/chart-of-the-day-time-warner-aol-2009-5 , [Accessed 19 May 2014]](https://image.slidesharecdn.com/hsrwcorporatefinance156591571415838-150401190343-conversion-gate01/85/corporate-finance-Valuation-of-M-A-AOL-Time-Warner-34-320.jpg)

![+

The Newyork times (2009) 10th Anniversary of AOL-Time Warner Merger, Available from

http://www.nytimes.com/interactive/2010/01/11/business/20100111-merger-timeline.html?_r=0 [Accessed 19 May

2014]

McGraw Hill (2007) Behavioral Corporate Finance, Available from http://highered.mcgraw-

hill.com/sites/dl/free/0072848650/315497/Chap10.ppt [Accessed 18 May 2014]

Imaa Institute (?) Statistics Merger and Acquisition, Available from http://www.imaa-institute.org/statistics-mergers-

acquisitions.html#TopMergersAcquisitions_Worldwide [Accessed 18 May 2014]

CNN (2000) That’s AOL folks, Available from http://money.cnn.com/2000/01/10/deals/aol_warner/ [Accessed 20

May 2014]](https://image.slidesharecdn.com/hsrwcorporatefinance156591571415838-150401190343-conversion-gate01/85/corporate-finance-Valuation-of-M-A-AOL-Time-Warner-35-320.jpg)

![Pcf (2) 4_mergers_and_acquisitions[2] ms](https://cdn.slidesharecdn.com/ss_thumbnails/pcf24mergersandacquisitions2ms-120403071025-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Mergers-and-Acquisitions-A-Financial-Analysis_(1)[1][1][1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/mergers-and-acquisitions-a-financial-analysis1111-251224145013-b5338ba6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Fsa] GSK fianacial statement analysis](https://cdn.slidesharecdn.com/ss_thumbnails/fsaworkingpapergroup6gsk-150108165315-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)