Download as PDF, PPTX

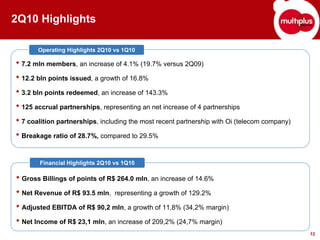

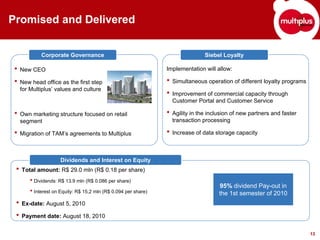

This investor presentation by Multiplus S.A. provides an overview of the company and its recent financial results. Multiplus is the leading loyalty coalition network in Brazil with over 7 million members and 125 partnerships. In Q2 2010, Multiplus saw increases in members, points issued and redeemed, and partnerships. Financial highlights included a 14.6% increase in gross billings and a 209.2% increase in net income. The presentation also outlines Multiplus' strategy for growth, margins, members, and branding as well as its relationship with major partner TAM Airlines.