Download to read offline

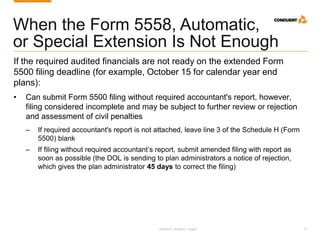

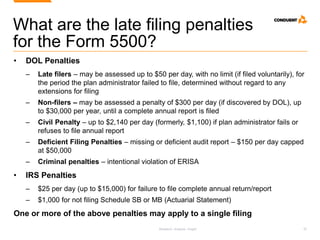

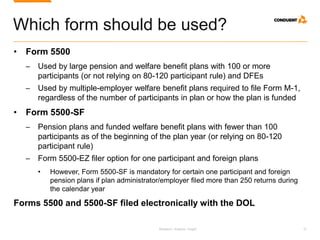

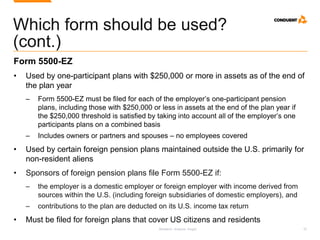

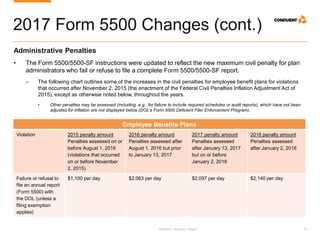

The document provides an overview and update on Form 5500 filing requirements for the 2017 filing season. Key points include: - Form 5500 is the annual report filed for employee benefit plans and certain entities to report financial and compliance information to DOL, IRS, and PBGC. - The deadline for plans and GIAs is the last day of the 7th month after the plan year end, or may be extended to 9.5 months. DFEs other than GIAs have a deadline of 9.5 months after year end with no extensions. - Late or non-filers may face penalties from DOL of up to $50 per day for late filers or $300 per day for