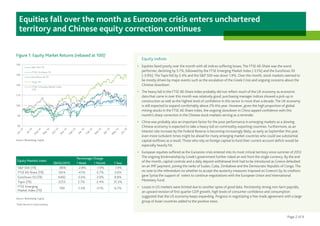

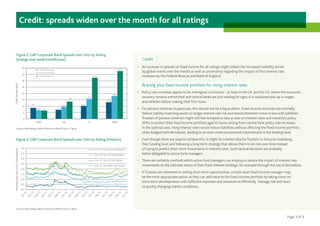

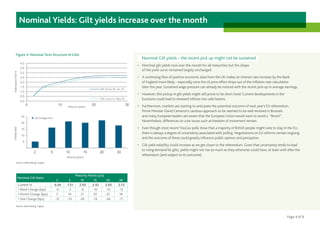

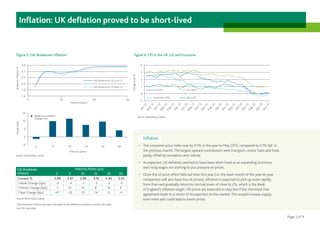

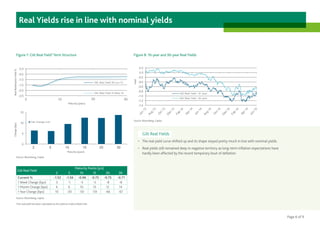

This document provides a monthly market commentary for July 2015. It summarizes performance across various asset classes for the past month and year. Equities fell globally last month due to concerns over the Greek debt crisis and Chinese stock market correction. Credit spreads widened for all ratings. Nominal gilt yields rose but the yield curve shape remained unchanged. UK inflation proved short-lived as deflation ended, while real gilt yields rose in line with nominal yields.