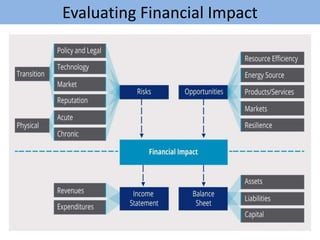

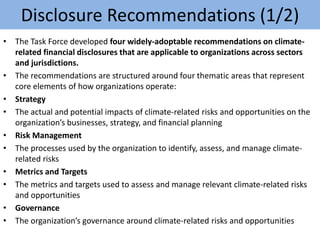

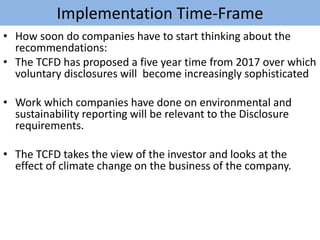

The document summarizes recommendations from the Task Force on Climate-related Financial Disclosures (TCFD) for new corporate reporting on climate change. The TCFD developed recommendations in four areas: strategy, governance, risk management, and metrics/targets. It also provides guidance for all sectors to help implement the recommended disclosures in financial filings to inform investors and other stakeholders about climate-related risks and opportunities. Implementation is expected to occur over five years to allow for increasingly sophisticated voluntary disclosures.