Download to read offline

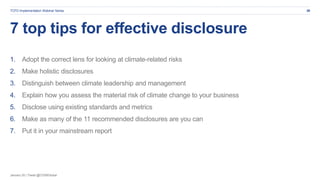

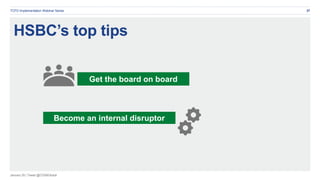

The document outlines a TCFD implementation webinar led by executives from HSBC and CDSB, focusing on improving climate-related risk management disclosures. Key themes include the necessity for clearer reporting on climate-related financial implications and effective strategies for integrating climate risks into mainstream reporting. Recommendations highlight the importance of governance, metrics, and the identification of various risks, emphasizing that greater stakeholder engagement is essential for enhanced transparency and sustainability in corporate practices.