Guidelines

•Tips to bemore interactive in Live Session

• Maintain discipline for smooth conductance of

the interactive live session.

• Type in your Name, UID and Program name on

chat to mark your attendance.

• Raise your questions only after completion of

session and do not intervene in between.

• Avoid posting irrelevant questions. Also, don’t

start any personal conversation.

• Interaction with faculty should be constructive,

and no disruptive comment is appreciated.

• For any issues, please contact our academic

support service @+91 8530568939 or post

your queries on support@dypatiledu.com

3.

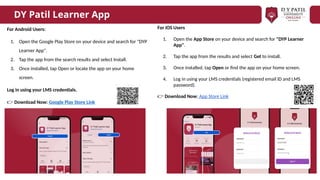

For Android Users:

1.Open the Google Play Store on your device and search for "DYP

Learner App".

2. Tap the app from the search results and select Install.

3. Once installed, tap Open or locate the app on your home

screen.

Log in using your LMS credentials.

👉 Download Now: Google Play Store Link

DY Patil Learner App

For iOS Users

1. Open the App Store on your device and search for "DYP Learner

App".

2. Tap the app from the results and select Get to install.

3. Once installed, tap Open or find the app on your home screen.

4. Log in using your LMS credentials (registered email ID and LMS

password).

👉 Download Now: App Store Link

4.

By the endof this session, you will be able to:

Learning Objectives

o Final Accounts

5.

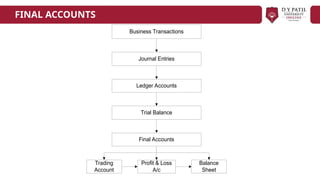

• Final Accountsis the last step in the accounting process. Trial

Balance is prepared at the end of all the accounting year to know

the balances of all the accounts & to test the arithmetic accuracy of

accounts. But the basic objective of accounting is to know about the

profit or loss during the previous year & present financial position.

This can be known only if Trading account and Profit & Loss account

and Balance Sheet are prepared at the end pf year. These are also

known as FINANCIAL STSTEMENTS which are prepared

FINAL ACCOUNTS

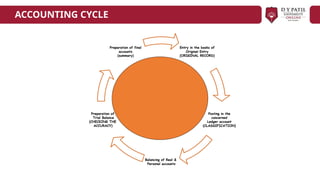

Entry in thebooks of

Original Entry

(ORIGINAL RECORD)

Posting in the

concerned

Ledger account

(CLASSIFICATION)

Balancing of Real &

Personal accounts

Preparation of

Trial Balance

(CHECKING THE

ACCURACY)

Preparation of final

accounts

(summary)

ACCOUNTING CYCLE

Key definitions

Business: Anorganization created

with the objective of making a profit

from the sale of goods or services.

Financial Transactions : Activity that

can be measure in monetary terms.

Calendar Year: An entity’s reporting

year, covering 12 months.

Revenues: Revenue is the money

that a company earns from selling

goods or services.

Expenses: Expenses are the costs that

a company incurs in order to make

that revenue.

Turnover: It means total trading

income from cash sales and credit

sales.

Key definitions

Accounting Terminology

12.

Key definitions

Net worth:It means assets minus

outside liabilities. It denotes value of

business.

Balance sheet : An itemized

statement which lists the total assets

and the total liabilities of business.

Debtor: A debtor is a person who

owes money. The amount due from

his is called debt.

Creditor: A person to whom money is

owing or payable is called a creditor.

Liquidity: The availability of cash or

ability to obtain it quickly. Also used

to determine debt repayment ability.

Trial Balance: A listing of all account

balances that control whether total

debits equals total credits.

Key definitions

Accounting Terminology

13.

Key definitions

Assets: Assetsare things that a

company owns that have Future

Economic Benefits.

Liabilities: Liabilities are things that a

company owes to others.

Profit: Profit is what's left over after a

company subtracts its expenses from

its revenue..

Depreciation: Depreciation is when

an asset loses value over time. This

happen to Fixed assets.

Cash Flow: Cash flow is the

movement of money in and out of a

company.

Capital: Amount invested by the

owners of business.

Key definitions

Accounting Terminology

14.

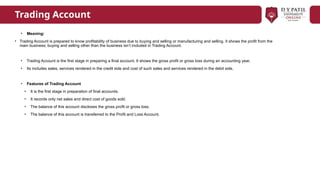

Trading Account

• Meaning:

•Trading Account is prepared to know profitability of business due to buying and selling or manufacturing and selling. It shows the profit from the

main business; buying and selling other than the business isn’t included in Trading Account.

• Trading Account is the first stage in preparing a final account. It shows the gross profit or gross loss during an accounting year.

• Its includes sales, services rendered in the credit side and cost of such sales and services rendered in the debit side.

• Features of Trading Account

• It is the first stage in preparation of final accounts.

• It records only net sales and direct cost of goods sold.

• The balance of this account discloses the gross profit or gross loss.

• The balance of this account is transferred to the Profit and Loss Account.

15.

01

Sales

Record total salesrevenue

for the accounting period.

02

Direct Costs

Include all expenses

directly related to

production.

03

Gross Profit

Calculate by subtracting direct

costs from total sales.

04

Opening Stock

Start with inventory value at

the beginning of the period.

05

Closing Stock

Determine inventory value at

the end of the period.

06

Purchases

Document all purchases made

during the accounting period.

07

Cost of Goods Sold

Identify total costs incurred

for goods sold.

Components of the Trading Account

16.

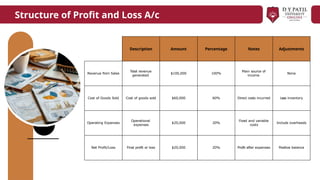

Description Amount PercentageNotes Adjustments

Revenue from Sales

Total revenue

generated

$100,000 100%

Main source of

income

None

Cost of Goods Sold Cost of goods sold $60,000 60% Direct costs incurred Less inventory

Operating Expenses

Operational

expenses

$20,000 20%

Fixed and variable

costs

Include overheads

Net Profit/Loss Final profit or loss $20,000 20% Profit after expenses Positive balance

Structure of Profit and Loss A/c

17.

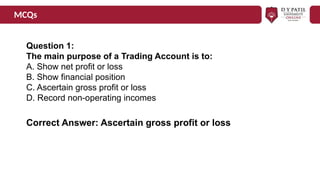

MCQs

Question 1:

The mainpurpose of a Trading Account is to:

A. Show net profit or loss

B. Show financial position

C. Ascertain gross profit or loss

D. Record non-operating incomes

Correct Answer: Ascertain gross profit or loss

18.

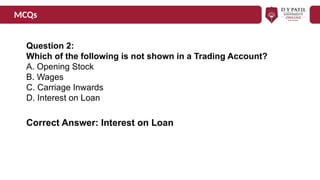

MCQs

Question 2:

Which ofthe following is not shown in a Trading Account?

A. Opening Stock

B. Wages

C. Carriage Inwards

D. Interest on Loan

Correct Answer: Interest on Loan

19.

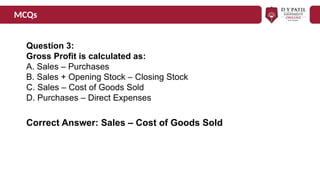

MCQs

Question 3:

Gross Profitis calculated as:

A. Sales – Purchases

B. Sales + Opening Stock – Closing Stock

C. Sales – Cost of Goods Sold

D. Purchases – Direct Expenses

Correct Answer: Sales – Cost of Goods Sold

#11 Revenue – Details about revenue. How definition of revenue changes with change in industry. Difference between revenue from operation and other revenues

Expenses: impact of expenses definition in different industries. Type of expenses (direct, indirect, operating, non operating, fixed variable etc)

#13 Assets:

Definition if Future economic benefits. Difference between assets and expenses.

Type of assets (current asset, fixed assets and investment).

Liabilities.

Type of liabilities (current and non current), accrual concept. Difference between liabilities and equity.

Profits. Type of profits (gross profit, net profit, operating profits EBITDA, EBIT, EBT etc)

Capital- what is share, concept of corporate veil, retained earnings, link of profits with capital