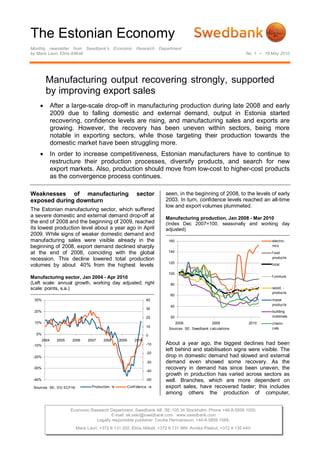

Download to read offline

The Estonian economy is experiencing a recovery in manufacturing output, supported by rising exports, though the recovery is uneven across sectors. Companies must restructure and diversify to enhance competitiveness, especially in the face of increasing production costs and external market pressures. Despite challenges, overall manufacturing confidence is improving, with expectations of further growth if global demand stabilizes.