Chp 16. capital reduction (patr ii)

•

2 likes•455 views

The document contains journal entries for capital reduction transactions for 9 questions. Some key details: 1) Question 1 shows journal entries to reduce share capital from Rs. 10 to Rs. 4 per share and adjust various asset accounts. 2) Question 2 contains entries to reduce share capital and debentures and transfer amounts to profit/loss, stock, etc. 3) Question 3 includes reducing share capital and debentures, transferring funds to adjust goodwill and various asset accounts. The document provides detailed journal entries for several capital reduction scenarios involving the adjustment of share capital, debentures, and asset and liability accounts.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Chp 16. capital reduction (patr ii)

Similar to Chp 16. capital reduction (patr ii) (20)

More from Arshad Islam

More from Arshad Islam (20)

Recently uploaded

Recently uploaded (20)

Chp 16. capital reduction (patr ii)

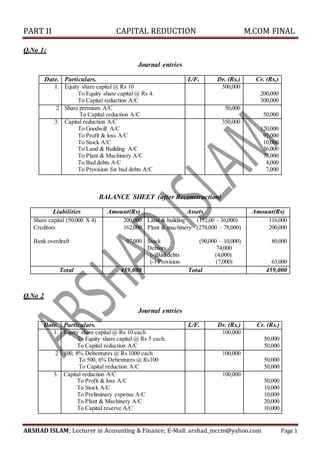

- 1. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 1 Q.No 1: Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Equity share capital @ Rs 10 To Equity share capital @ Rs 4. To Capital reduction A/C 500,000 200,000 300,000 2 Share premium A/C To Capital reduction A/C 50,000 50,000 3. Capital reduction A/C To Goodwill A/C To Profit & loss A/C To Stock A/C To Land & Building A/C To Plant & Machinery A/C To Bad debts A/C To Provision for bad debts A/C 350,000 120,000 95,000 10,000 36,000 78,000 4,000 7,000 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Share capital (50,000 X 4) 200,000 Land & building (152,00 - 36,000) 116,000 Creditors 162,000 Plant & machinery (278,000 – 78,000) 200,000 Bank overdraft 97,000 Stock (90,000 – 10,000) 80,000 Debtors 74,000 (-)Bad debts (4,000) (-) Provision (7,000) 63,000 Total 459,000 Total 459,000 Q.No 2 Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Equity share capital @ Rs 10 each To Equity share capital @ Rs 5 each. To Capital reduction A/C 100,000 50,000 50,000 2 100, 8% Debentures @ Rs 1000 each To 500, 6% Debentures @ Rs100 To Capital reduction A/C 100,000 50,000 50,000 3. Capital reduction A/C To Profit & loss A/C To Stock A/C To Preliminary expense A/C To Plant & Machinery A/C To Capital reserve A/C 100,000 50,000 10,000 10,000 20,000 10,000

- 2. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 2 Q.No 3 Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Equity share capital (20,000 X 10) To Equity share capital @ (20,000.X 5) To Capital reduction A/C 200,000 100,000 100,000 2 5% Debentures @ Rs 100 To 6% Debentures @ Rs 75 To Capital reduction A/C 100,000 75,000 25,000 3. Capital reduction A/C To Goodwill A/C To Profit & loss A/C To Plant & machinery A/C To Furniture A/C To Stock A/C To Provision for bad debts A/C 125,000 20,000 80,000 13,000 2,000 6,000 4,000 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Share capital (50,000X4) 100,000 Land & building 70,000 6% Debentures 75,000 Plant & machinery (85,000 – 13,000) 72,000 Creditors 30,000 Stock (35,000 – 6,000) 29,000 Bills payable 10,000 Furniture (8,000 – 2,000) 6,000 Debtor (40,000 – 4000) 36,000 Cash 2,000 Total 215,000 Total 215,000 Q.No4 Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Preference share capital@ Rs 20 each To Preference share capital@ Rs 15 each To Capital reduction A/C 1,000,000 750,000 250,000 2 Equity share capital @ Rs 20, Rs 15 Paid up To Equity share capital @ Rs 10 Fully paid To Capital reduction A/C 750,000 500,000 250,000 3. Capital reduction A/C To Goodwill A/C To Profit & loss A/C To Plant & machinery A/C To Investment A/C To Capital reserve A/C 500,000 40,000 210,000 90,000 80,000 80,000

- 3. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 3 Q.No 5 Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Preference share capital@ Rs 100 each To Preference share capital@ Rs 50 each To Capital reduction A/C 750,000 375,000 375,000 2 Equity shares @ Rs 100 each To equity shares @ Rs 50 each To Capital reduction A/C 500,000 125,000 375,000 3. Capital reduction A/C To Leasehold Premises A/C To Stock A/C To Plant & machinery A/C To Provision for bad debts A/C To Profit & loss A/C To Preliminary expense A/C To Discount on issue of shares A/C To Patents A/C (Balance figure) 750,000 30,800 15,000 8,400 15,040 115,000 10,000 20,000 535,760 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Equity Share capital 125,000 Patents 314,240 Preference share Capital 375,000 Leasehold Premises 100,000 Creditors 30,000 Plant & machinery 33,600 Bank old 20,000 Debtors 60,010 Stock 41,500 Cash 500 Total 550,000 Total 550,000 Q.No 6: Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Equity share capital @ Rs 50 each To Equity share capital @ Rs 30 each To Capital reduction A/C 400,000 240,000 160,000 2 Preference shares @ RS 50 each To Preference shares @ Rs30 each To Capital reduction A/C 400,000 240,000 160,000 3. Capital reduction A/C To Profit & loss A/C To Stock A/C To Preliminary expenses A/C To Provision for bad debts A/C To Lease hold premises A/C To Plant A/C 320,000 124,000 20,000 50,000 30,000 66,000 30,000

- 4. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 4 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Equity Share capital 240,000 Leasehold Premises 384,000 Preference shares Capital 240,000 Plant 50,000 Creditors 40,000 Debtors 70,000 Bank old 35,000 Stock 50,000 Cash 1,000 Total 550,000 Total 550,000 Q.No 7 Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Equity share capital @ Rs 100 each To Equity share capital @ Rs 50 each To Capital reduction A/C 800,000 400,000 400,000 2 5% Preference shares@ Rs 100 each To 7% Preference shares @ Rs 70 each To Capital reduction A/C 300,000 210,000 90,000 3. Cash & Bank A/C (500 @ Rs 50) To Equity Share capital A/C 250,000 250,000 4. Sundry creditors A/C To Capital reduction A/C To Cash & Bank A/C 125,000 25,000 100,000 5. Capital reduction A/C To Cash & Bank A/C 7,500 7,500 6. Capital reduction A/C To Goodwill A/C To Profit & loss A/C To Patents A/C To Preliminary expenses A/C To Plant & machinery A/C To Stock A/C To Provision for bad debts A/C To Capital reserve A/C 507,500 150,000 210,000 45,000 20,000 45,000 20,000 4,500 13,000 BALANCE SHEET (after Reconstruction) Liabilities Amount (Rs) Assets Amount (Rs) Equity Share capital 650,000 Land & building 450,000 Preference share Capital 210,000 Plant& machinery (250,000 – 40,000) 205,000 Capital reserve 13,000 Debtors (90,000 – 4,500) 85,500 Bank over draft 105,000 Stock (135,000 – 20,000) 115,000 Secured loan 50,000 Cash (30,000 + 250,000 – 10,000 – 7,500) 172,000 Total 1,028,000 Total 1,028,000

- 5. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 5 Q.No 8: Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Equity share capital @ Rs 10 each To Call in arrear @ (3000 X 7) To Capital reduction A/C 30,000 9,000 21,000 2 Equity share Capital (9,000 X 3) To Capital reduction A/C 27,000 27,000 3. Bank A/C (3,000 X 5) Share forfeited A/C To Equity Share capital A/C 15,000 6,000 21,000 4. Share forfeited A/C Provision for tax A/C To Capital reduction A/C 15,000 300 15,300 5. Capital reduction A/C To Machinery A/C To Profit & loss A/C To Preliminary expense A/C To Goodwill A/C 42,300 10,000 20,800 1,500 10,000 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Share capital 85,000 Building 20,500 Provision for tax 3,700 Machinery (50,850 – 10,000) 40,850 Sundry creditors 15,425 Sundry Debtors 15,000 Stock 10,275 Cash (1,500 + 15,000) 16,500 Total 103,125 Total 103,125

- 6. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 6 Q.No 9: BALANCE SHEET (before Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Share capital (60% paid) 6,000,000 Fixed assets 700,000 10%, 1st debenture 200,000 Investments 10,000 12%, 2nd debenture 50,000 Stock 850,000 Trade creditors 1,150,000 Preliminary expense 20,000 Bank over draft 50,000 Profit & loss (Balancing figure) 1,000,000 Outstanding interest on Debentures 80,000 Total 2,580,000 Total 2,580,000 Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Share final call A/C To Equity share Capital A/C 400,000 400,000 2 Bank A/C To Share final call A/C 400,000 400,000 3. Equity share Capital Of Rs 100 each To Equity share Capital of Rs 20 each To Capital reduction A/C 1,000,000 200,000 800,000 4. 10% 1st debentures A/C To 13.5% debentures A/C 200,000 200,000 5. 12% 2nd debentures A/C To 15% debentures A/C To capital reduction A/C 500,000 400,000 100,000 6. Sundry creditors A/C (Y) To Bank A/C To Capital reduction A/C 850,000 300,000 550,000 7. Sundry creditors A/C (1,150,000 – 850,000) To Equity share Capital A/C (15,000 shares @ Rs 20 each) 300,000 300,000 8. Investments A/C To capital reduction A/C 10,000 10,000 9. Outstanding interest on Debentures A/C To Capital reduction A/C 80,000 80,000 10. Capital reduction A/C To Profit & loss A/C To Preliminary expense A/C To Fixed assets A/C 1,540,000 1,000,000 20,000 520,000

- 7. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 7 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Equity share capital 500,000 Fixed assets 180,000 13.5% debentures 200,000 Investments 20,000 15% debentures 400,000 Stock 850,000 Bank 50,000 Total 1,100,000 Total 1,100,000 Q.No 10: Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. 6% Preference share Capital@ Rs 100 each To 7.5% Preference share capital@ Rs 30 To Capital reduction A/C 200,000 60,000 140,000 2 Equity share Capital @ Rs 100 each To Equity share Capital @ Rs 5 each To Capital reduction A/C 300,000 15,000 285,000 3. Bank A/C (17,000 X 5) To Equity share capital A/C 85,000 85,000 4. Sundry creditors A/C To Equity share Capital A/C (150000 X1/3) To Bank A/C To Capital reduction A/C 150,000 50,000 50,000 50,000 5. Land & building A/C Plant & Machinery A/C To capital reduction A/C 20,000 22,000 42,000 6. Interest due on Debentures A/C To Capital reduction A/C 10,000 10,000 7. Capital reduction A/C To Profit & loss A/C To Preliminary expenses A/C To Goodwill A/C To Patents A/C To Stock A/C To Debtors A/C 527,000 390,000 20,000 80,000 15,000 15,000 7,000 8. 7.5% Preference share capital@ Rs 30 each To Equity share capital @ Rs 10 each 60,000 60,000 9. Equity share capital @ Rs 5 To Equity share capital @ Rs 10 150,000 150,000

- 8. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 8 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Equity Capital (21,000 @ Rs 10) 210,000 Plant & machinery Land & building 112,000 95,000 5% debentures 100,000 Patents 5,000 Stock 25,000 Debtors 32,000 Cash 41,000 Total 310,000 Total 310,000 Q.No 12: Journal entries Date. Particulars L/F. Dr. (Rs.) Cr. (Rs.) 1. 6% Preference share capitalA/C To 8% Preference share capitalA/C To Capital reduction A/C 300,000 225,000 75,000 2 Equity share capital @ Rs 10 each To Equity share capital @ Rs8 each To Capital reduction A/C 450,000 360,000 90,000 3. Capital reduction A/C To Goodwill A/C To Land & building A/C To Plant & machinery A/C To Sundry debtors A/C To Profit & loss A/C To Patents A/C 165,000 42,300 40,500 48,000 7,200 15,000 12,000 4. Cash & Bank A/C To 12% Mortgage loan A/C 240,000 240,000 BALANCE SHEET (after Reconstruction) Liabilities Amount(Rs) Assets Amount(Rs) Capital 45,000 @ 8 360,000 Patent 6,000 Preference share 225,000 Land & building 229,500 12% S. loan 240,000 Plant & machinery 192,000 Sundry creditor 60,000 Stock 88,800 Bills payable 50,000 Debtor 143,700 Cash 140,000 Profit & loss 135,000 Total 935,000 Total 310,000

- 9. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 9 Q.No 15: Journal entries Date Particulars L/F. Dr. (Rs.) Cr. (Rs.) 1. 6% Preference share capital@ Rs 10 each To 6% Preference share capital@ Rs 2 each To Capital reduction A/C 300,000 60,000 240,000 2 Equity share capital @ Re 1 each To Equity share capital @ Rs 0.25 each To Capital reduction A/C 600,000 150,000 450,000 3. 6% Preference share capital@ Rs 2 each To 6% Preference share capital@ Rs 10 each 240,000 240,000 4. Equity share capital @ Rs 0.25 each To Equity share capital @ Re 1 each 150,000 150,000 5. Capital reduction A/C To Equity share capital A/C 180,000 180,000 6. Cash & Bank A/C To shares in Subsidiary Company A/C To Capital reduction A/C 150,000 75,000 75,000 7. 8% Debentures A/C To Land & building A/C To Capital reduction A/C 60,000 54,000 6,000 8. Cash & Bank A/C To 8% Debentures A/C 45,000 45,000 9. Interest A/C To cash Bank A/C 6,000 6,000 10. Directors loan A/C Capital reduction A/C To Cash & Bank A/C 15,000 15,000 30,000 11. Director Loan A/C To Cash Bank A/C 9,000 9,000 12. Director loan A/C To Equity share capital A/C 51,000 51,000 13. Capital reduction A/C To Profit & loss A/C To Goodwill A/C To Advertisement A/C To Debtors A/C To Stock A/C To Capital reserve A/C 558,000 264,000 120,000 60,000 12,000 30,000 72,000

- 10. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 10 BALANCE SHEET (After Reconstruction) Liability Amount(Rs ) Assets Amount(Rs ) 6% Preference share 240,000 Land & building 213,000 Equity shares 219,000 Plant 155,000 Capital reserve 72,000 Stock 195,000 8% Debentures 105,000 Debtor 258,000 Bank old 165,000 Cash 150,000 Creditors 270,000 Total 1,071,000 Total 1,071,000 Q.No 16 SOLUTION:- Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1 Equity share 100 To Equity shares 400,000 400,000 2. Equity share capital To Share surrender 85,000 85,000 3. Share surrender To Equity share capital Being debenture holder claim 115,000 115,000 4. Share surrender To Equity share capital Being creditor claim settled 45,000 45,000 5. Share surrender Debenture A/C Debenture interest Sundry creditor To Capital reduction 220,000 670,000 20,000 225,000 1,135,000 6. Capital reduction To Profit & loss To Land & building 1,135,000 535,000 600,000 7. Income tax To Cash 5,000 5,000 BALANCE SHEET AFTER Liability Amount(Rs ) Assets Amount(Rs ) Equity share capital 180,000 Land & building 115,000 Stock 40,000 Debtor 15,000 Investment 8,500 Cash 1,500 Total 180,000 Total 180,000

- 11. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 11 Q.No17 SOLUTION:- Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1 Equity share 100 To Equity shares 3,000,000 3,000,000 2. Equity share capital To Share surrender 2,100,000 2,100,000 3. Share surrender To Equity share capital 500,000 500,000 4. Share surrender To Equity share capital Being debenture claim settled 700,000 700,000 5. Share surrender To Equity share capital Being creditor 50% claim settled 200,000 200,000 6. Share surrender To capital reduction 700,000 700,000 7. 11% Preference shares 15% Debentures Debenture interest Creditor To Capital reduction 1,000,000 1,000,000 300,000 420,000 2,720,000 8. Capital reduction To Profit & loss To Goodwill To Fixed assets To Capital reserve 3,420,000 1,550,000 500,000 1,000,000 370,000 BALANCE SHEET AFTER Liability Amount(Rs ) Assets Amount(Rs ) Capital 2,300,000 Fixed assets 2,000,000 Sundry creditor 420,000 Current assets 1,090,000 Capital reserve 370,000 Total 3,090,000 Total 3,090,000 Q.No 18 SOLUTION:- Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1 Equity share 100 To Capital reduction Being paid up capital reduced 80,750 80,750 2. Bank To Equity share capital Being again called 80,750 80,750

- 12. PART II CAPITAL REDUCTION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 12 3. Bank loan To Equity share capital To Bank 60,000 15,000 45,000 4. Bank To Equity share capital 50,000 50,000 5. Bank To C.R.A To 12% Debentures To Bank 64,500 16,125 48,300 75 6. Bank overdraft To capital reduction To Bank 56,5000 6,500 50,000 7. Share Premium To Capital reduction 15,000 15,000 8. Capital reduction To Profit & loss To Goodwill To Share association 118,375 68,300 22,600 27,475 BALANCE SHEET AFTER Liability Amount(Rs ) Assets Amount(Rs ) Capital 2,300,000 Free hold 41,500 12% Debentures 420,000 Plant 60,000 370,000 Investment 2,525 Other investment 16,000 Stock 23,000 Debtor 19,600 Cash 35,675 Total 198,300 Total 198,300 ****************************************************************************** **********