The document summarizes the thesis that China's level of infrastructure investment is unsustainable and will lead to lower investment and profits for short positions. It provides evidence that infrastructure investment accounts for an unprecedented 49% of China's GDP and has exceeded 40% since 2003. It also notes widespread evidence of excess investment through metrics like housing affordability and cement usage far exceeding historical bubbles. While the Chinese government recognizes the issues and is trying to reform, there are doubts about the success of their efforts given resistance from powerful interests. The thesis is that infrastructure investment will ultimately be forced to slow due to debt constraints, leading to profits for short positions, regardless of government actions.

Namrata choudhry bank lending and capital formationPrashant Kulkarni

The role of public investment in agricultural capital formation has declined even sharper. The fall would have been sharper but for the private investment which has filled the gap. This raises the question about the complementarities between private and public investment. Even more important is the determinants of the capital formation. Traditionally banks have played a role in capital formation. Interestingly the capital formation has alos happened through informal channels for which very little data is available. The paper examines the impact of bank lending on capital formation and consequent impact on the production. The correlation between the direct and indirect bank credit on the capital formation is 93% and coefficient of determination is 88%. Our studies show that there is an influence on bank lending on capital formation both public and private which consequently impacts the production patterns. Capital formation does lead to increase in production. There is a strong correlation between the public and private capital formation and agricultural production. The impact as measured by the coefficient of determination is less than 50%.

Namrata choudhry bank lending and capital formationPrashant Kulkarni

The role of public investment in agricultural capital formation has declined even sharper. The fall would have been sharper but for the private investment which has filled the gap. This raises the question about the complementarities between private and public investment. Even more important is the determinants of the capital formation. Traditionally banks have played a role in capital formation. Interestingly the capital formation has alos happened through informal channels for which very little data is available. The paper examines the impact of bank lending on capital formation and consequent impact on the production. The correlation between the direct and indirect bank credit on the capital formation is 93% and coefficient of determination is 88%. Our studies show that there is an influence on bank lending on capital formation both public and private which consequently impacts the production patterns. Capital formation does lead to increase in production. There is a strong correlation between the public and private capital formation and agricultural production. The impact as measured by the coefficient of determination is less than 50%.

FINANCIAL ANALYSIS - BOOK REVIEW - FAULT LINES - HOW HIDDEN FRACTURES STILL T...Mufaddal Nullwala

Contents:

Background

Challenges faced by U.S

Let Them Eat Credit

Exporting to Grow

Flighty foreign financing

Weak Safety Net

From Bubble to bubble

When money is the measure of all worth

Betting the bank

Reforming Finance

Broad Principles Of Reform

Eliminating “Too Systemic to Fail”

Resilience

Improving access to opportunity in America.

Multilateral institutions & their influence

Obtaining global influence

China and The World

Persuading China

What lies Ahead for INDIA

Passing a budget is just one step in financing the federal government. Specific decisions about government spending are made through an annual process called appropriations. Here are answers to key questions to better understand the process.

Foreign Aid and Domestic Tax: Multiple Sources, One Conclusion -Presentation by Paul Clist (U. East Anglia).

The relation between taxes and foreign aid in developing countries has been vastly investigated in the literature. Indeed, in the short term, aid inflows may be seen as a substitute for tax revenues in the eyes of recipient countries, thus lowering the incentive of the latter at increasing their revenues from taxation. However, in the long run, relying on foreign aid with no or marginal taxing of the people might affect governance of the countries, as it breaks the social contract between the citizen and the state. One common finding in the literature is the negative impact of grant type of aid on recipients’ government revenues. This paper therefore sought to replicate existing studies, adding new inputs in order to see whether this assertion would remain true.

The paper by Paul Clist failed at replicating Benedek et al. (2012), which concluded that there is a negative association between domestic tax mobilization and grants, though this relationship appears to have weakened as the original dataset exhibits some discrepancies. Clist and Morrissey (2009) extended Gupta et al. (2004) study over the period 1970-2005 (against 1970-2000). Although they found a significant negative impact of grant aid on government revenue, this effect happened to be driven by the period 1970-1985, when the IMF data was at its worst. When focusing on the period 1986-2005, results are reversed with a robust positive relationship between grant aid and tax revenues.

In terms of limitation, one of the main issues stem from the fact that most of the previous studies were conducted using data from different sources, where key variables had different definitions. Endogeneity is also a major concern as poor tax collection performance and increased aid grant can simultaneously respond to the same shock such as natural disasters.

Four strategies to cope with those problems are established in the paper, including one year and two year lagged aid variables, multiple indicators with multiple causes (MIMIC) models and the use of the new ICTD GRD. In most of the cases, the statement that aid grant has a negative impact on tax revenue is rejected and, as the new data shows, there is no negative effect of aid grants on tax revenue at all.

The conclusion that can be drawn from this is that the negative relationship between tax revenue and grants is driven by bad quality data, making the ICTD GRD not only better, but also much needed.

FINANCIAL ANALYSIS - BOOK REVIEW - FAULT LINES - HOW HIDDEN FRACTURES STILL T...Mufaddal Nullwala

Contents:

Background

Challenges faced by U.S

Let Them Eat Credit

Exporting to Grow

Flighty foreign financing

Weak Safety Net

From Bubble to bubble

When money is the measure of all worth

Betting the bank

Reforming Finance

Broad Principles Of Reform

Eliminating “Too Systemic to Fail”

Resilience

Improving access to opportunity in America.

Multilateral institutions & their influence

Obtaining global influence

China and The World

Persuading China

What lies Ahead for INDIA

Passing a budget is just one step in financing the federal government. Specific decisions about government spending are made through an annual process called appropriations. Here are answers to key questions to better understand the process.

Foreign Aid and Domestic Tax: Multiple Sources, One Conclusion -Presentation by Paul Clist (U. East Anglia).

The relation between taxes and foreign aid in developing countries has been vastly investigated in the literature. Indeed, in the short term, aid inflows may be seen as a substitute for tax revenues in the eyes of recipient countries, thus lowering the incentive of the latter at increasing their revenues from taxation. However, in the long run, relying on foreign aid with no or marginal taxing of the people might affect governance of the countries, as it breaks the social contract between the citizen and the state. One common finding in the literature is the negative impact of grant type of aid on recipients’ government revenues. This paper therefore sought to replicate existing studies, adding new inputs in order to see whether this assertion would remain true.

The paper by Paul Clist failed at replicating Benedek et al. (2012), which concluded that there is a negative association between domestic tax mobilization and grants, though this relationship appears to have weakened as the original dataset exhibits some discrepancies. Clist and Morrissey (2009) extended Gupta et al. (2004) study over the period 1970-2005 (against 1970-2000). Although they found a significant negative impact of grant aid on government revenue, this effect happened to be driven by the period 1970-1985, when the IMF data was at its worst. When focusing on the period 1986-2005, results are reversed with a robust positive relationship between grant aid and tax revenues.

In terms of limitation, one of the main issues stem from the fact that most of the previous studies were conducted using data from different sources, where key variables had different definitions. Endogeneity is also a major concern as poor tax collection performance and increased aid grant can simultaneously respond to the same shock such as natural disasters.

Four strategies to cope with those problems are established in the paper, including one year and two year lagged aid variables, multiple indicators with multiple causes (MIMIC) models and the use of the new ICTD GRD. In most of the cases, the statement that aid grant has a negative impact on tax revenue is rejected and, as the new data shows, there is no negative effect of aid grants on tax revenue at all.

The conclusion that can be drawn from this is that the negative relationship between tax revenue and grants is driven by bad quality data, making the ICTD GRD not only better, but also much needed.

What will be the likely impact of the growing economic power of China and India on individuals, national and multinational firms in the 21st century?

Implications of their population size, economic growth and export rates, increased purchasing power and foreign investment, predicted economic power compared with US and EU, barriers to market entry, trade opportunities for UK firms, differences between China and India, for example state ownership of firms.

Presentation by Toshiya Tsugami, President of Tsugami Workshop, Ltd., at the IAI conference "Xi Jinping’s China: Are Japan and Europe on the same page?" organised in cooperation with the Japanese Embassy in Rome

• The true picture of China’s outbound investment is quite different from many people’s impression.

• Investments in Africa are also in their early stages.

• Investments in Belt & Road countries remained small and slowed in the past year.

• Mining is no longer a primary target of China’s acquisition.

• The reduced foreign exchange reserve is not hard constraint to the outbound investment.

Getting more bang for your public investment buck - Richard Hugues, IMFOECD Governance

This presentation was made by Richard Hugues, IMF, at the 8th Meeting of Senior Public-Private Partnerships and Infrastructure Officials held in Paris on 23-24 March 2015.

The Perfect Storm with Chinese Characteristics: A downside Scenario for China...Team Finland Future Watch

A Downside Scenario for China’s Economy.

- Scenario analysis is not use to generate predictions, but rather to generate plausible futures in order to understand how they might come about in order to support planning and strategy formulation. An economic collapse scenario for China’s economy is not the consensus view.

- The scenario described in this document is not a prediction, but rather one plausible future given the current state of China and the world.

A presentation given by ISS Director Anthony Holmes at our Doha launch. Over fifty senior officials from government, business and academic circles in the Gulf and the UK joined the Mayor of London and the Qatar Financial Center Authority (QFC) at the event. Chaired by the British Ambassador to Qatar, Michael O’Neill, it featured lively contributions from the Mayor, Boris Johnson, the CEO of the QFC, Shashank Srivastava, and ISS Director Ian Kennedy.

Similar to Chinese infrastructure short thesis (20)

Attending a job Interview for B1 and B2 Englsih learnersErika906060

It is a sample of an interview for a business english class for pre-intermediate and intermediate english students with emphasis on the speking ability.

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

Putting the SPARK into Virtual Training.pptxCynthia Clay

This 60-minute webinar, sponsored by Adobe, was delivered for the Training Mag Network. It explored the five elements of SPARK: Storytelling, Purpose, Action, Relationships, and Kudos. Knowing how to tell a well-structured story is key to building long-term memory. Stating a clear purpose that doesn't take away from the discovery learning process is critical. Ensuring that people move from theory to practical application is imperative. Creating strong social learning is the key to commitment and engagement. Validating and affirming participants' comments is the way to create a positive learning environment.

What are the main advantages of using HR recruiter services.pdfHumanResourceDimensi1

HR recruiter services offer top talents to companies according to their specific needs. They handle all recruitment tasks from job posting to onboarding and help companies concentrate on their business growth. With their expertise and years of experience, they streamline the hiring process and save time and resources for the company.

Business Valuation Principles for EntrepreneursBen Wann

This insightful presentation is designed to equip entrepreneurs with the essential knowledge and tools needed to accurately value their businesses. Understanding business valuation is crucial for making informed decisions, whether you're seeking investment, planning to sell, or simply want to gauge your company's worth.

The world of search engine optimization (SEO) is buzzing with discussions after Google confirmed that around 2,500 leaked internal documents related to its Search feature are indeed authentic. The revelation has sparked significant concerns within the SEO community. The leaked documents were initially reported by SEO experts Rand Fishkin and Mike King, igniting widespread analysis and discourse. For More Info:- https://news.arihantwebtech.com/search-disrupted-googles-leaked-documents-rock-the-seo-world/

What is the TDS Return Filing Due Date for FY 2024-25.pdfseoforlegalpillers

It is crucial for the taxpayers to understand about the TDS Return Filing Due Date, so that they can fulfill your TDS obligations efficiently. Taxpayers can avoid penalties by sticking to the deadlines and by accurate filing of TDS. Timely filing of TDS will make sure about the availability of tax credits. You can also seek the professional guidance of experts like Legal Pillers for timely filing of the TDS Return.

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

VAT Registration Outlined In UAE: Benefits and Requirementsuae taxgpt

Vat Registration is a legal obligation for businesses meeting the threshold requirement, helping companies avoid fines and ramifications. Contact now!

https://viralsocialtrends.com/vat-registration-outlined-in-uae/

Implicitly or explicitly all competing businesses employ a strategy to select a mix

of marketing resources. Formulating such competitive strategies fundamentally

involves recognizing relationships between elements of the marketing mix (e.g.,

price and product quality), as well as assessing competitive and market conditions

(i.e., industry structure in the language of economics).

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

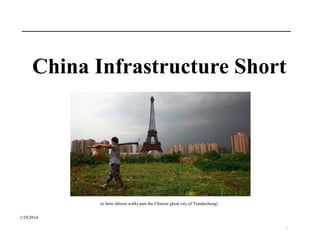

2. China Infrastructure Short – Thesis outline

1) The level of infrastructure investment in China is clearly unsustainable

2) The Chinese government (and every serious economist) explicitly recognizes this fact

and is undertaking efforts to lower the economy’s dependence on infrastructure

3) If these efforts are successful, infrastructure investment will be lower and our short

position will be profitable

4) If these efforts are unsuccessful, China will eventually be unable to support the debt

created by unprofitable infrastructure. This will result in lower credit availability and

less infrastructure build

5) In ether scenario our short positions will profit

2

3. China’s Infrastructure Investment is Clearly Unsustainable

• Infrastructure investment now accounts for 49% of China’s GDP and has exceeded 40% since 2003

• This level of investment is without historical precedent

• Past instances where investment exceeded 40% of GDP for a meaningful period resulted in credit crisis and

recessions

Historical Context of China’s Investment Level

3

4. Evidence of Excess Investment

There is widespread evidence of excess investment in China. A few areas of note are:

- Affordability: As shown below, globally Chinese real estate is now the least affordable by a wide margin

- Investment-to-GDP ratios: Not only is China’s total investment well in excess of historical bubbles, but

residential housing investment is also reaching a level only seen during previous bubbles

- ‘Common Sense’ evidence: Failed projects such as ‘ghost cities’ and empty malls have been widely reported.

This excess appears degrees of magnitude worse than even the largest infrastructure bubbles to date

4

5. Evidence of Excess Investment

• Cement is a key component of virtually all infrastructure and as such, cement usage tends to closely track

infrastructure investment

• Cumulatively since 1900, China has consumed 19mt of cement per person vs. 18mt in the United States. This is

despite having a per capita GDP only 12% of the US and an urbanization rate of 52% vs. 83% in the US

• China now accounts for 56% of global cement demand

• As shown below, China’s per capita cement usage well exceeds historical infrastructure bubbles

China’s per capita

cement usage is far

above prior bubbles

despite being a much

poorer country

5

6. Debt is the Result Excess Investment

• Excess investment invariably leads to excess debt as projects are funded that do not earn their cost of capital

• This is exactly what happened with Japan in the 1990’s, the US and Europe in 2007/2008 and is happening today in

China

6

7. China 2014 vs. US 2007

• By almost any metric, China today appears significantly worse off than the US on the eve of the 2007 financial crisis

USA 2007

vs.

China 2014

Residential construction % of GDP

6%

12%

Total investment % of GDP

23%

49%

Prior 5 year debt growth (% of GDP)

25%

55%

Home ownership (% of population)

71%

80%

6x

22x

Affordability of largest city

(multiple of avg wage)

GDP Per Capita

$

49,956

$

6,091

Empty housing developments, empty

strip malls

Empty cities, office towers and large

retail developments

Institutions

Robust, transparent legal and

financial institutions

Opaque system with limited history

and questionable rule of law

Government

World's oldest democracy with

independent central bank

Volatile 60 year history of one-party

rule

Evidence of over-capacity

7

8. The Chinese Government is Fully Aware of This

• The Chinese government is acutely aware of these issues and is taking steps to change the country’s growth model to

become less dependent on infrastructure investment

“China's leaders have said they want to remake the

economy so it relies less on heavy investment in real

estate, infrastructure and capital-intensive industries

and exports abroad. They have outlined proposals to

boost domestic consumption by giving peasants more

rights to land and liberalizing the financial sector so

more lending is directed to small businesses. There

has been little movement so far on those fronts.”

- Wall Street Journal, 1/20/2014

“China’s government recently announced ambitious

plans that could make the Chinese economy more

market driven, consumer driven, transparent, and

prone to profitable investing. Implementation remains

a significant challenge, but it is crucial to rectifying

the country’s currently unbalanced system”

- Deloitte Global Economic Outlook, 1/14/2014

► If these efforts are successful, then infrastructure investment will fall and our shorts will work

8

9. The Chinese Government is Fully Aware of This

There are several reasons to doubt that the government’s efforts will be successful:

• The current growth model has benefited many members of China’s elite and thus efforts to change are

likely to encounter resistance from powerful interests

• The transition to a consumer-focused growth model could be painful for certain sectors of the

economy and thus could be unpopular

• The historical record for similar situations gives little reason for optimism

With or without government action, unprofitable investment cannot continue forever as there is a limit to amount of

bad debt an economy can absorb. Thus infrastructure build will ultimately be forced to stop due to debt constraints

“What prevents China from pursuing these reforms is a combination of opposition from powerful

entrenched interest groups – state-owned enterprises, local governments, the economic-policy

bureaucracy, and family members of political elites and well-connected businessmen – and flawed

political institutions. Unless Xi and his colleagues demonstrate their resolve to overcome such opposition

and launch comprehensive reforms, their chances of success are not high”

-Minxin Pei, 11/7/2013

► If the party’s efforts are unsuccessful, then infrastructure investment will eventually fall due

to a lack of available credit and our shorts will work

9

10. Risks / Considerations

The main risks to this position are:

1) Extreme rebalancing: It is theoretically possible that China is able to grow consumption rapidly enough such

that the economy rebalances even if infrastructure grows in absolute terms (albeit much more slowly than

consumption). In this case infrastructure investment would only slow, not contract.

→ However, the stocks we are short appear to be pricing in some growth, so its not clear this would cause

a loss.

→ Given how high the absolute level of infrastructure build is currently, I view scenario this as highly

unlikely...

2) Company / industry specific risks: Even if our thesis plays out, it is possible that it the impact of lower

infrastructure spending is outweighed by positive company-specific events such as successful development

projects, cost rationalizations, etc.

→ Given the likely magnitude of the downside if our thesis plays out, I believe its unlikely that any

company-specific news would be enough to offset the impact of lower infrastructure spending

3) Cost of carry: Between dividends / borrow the cost to carry this position is about 4% per year

► Some combination of 1+2+3 could cause a loss. However as noted above, I believe this is unlikely

10