Content

CHAPTER 3: FINANCIALANALYSISAND PROJECTION

o Cost of project

o Means of finance (project financing)

o Estimation of sales and production

o The cost of production

o Cash flows in financial analysis

3.

Objectives

At theend of this lesson, students will be able to:

• Define and identify financial cost of a project

• Identify the different means of financing a project

• Identify the important points that should be considered in estimation of

sales and production of projects/ Businesses

• Identify the different components of cost of production of a project

• Identify the main components of cash flow and calculate related problems

4.

What is FinancialAnalysis?

What is financial Analysis?

• Financial Analysis is the assessment of the Viability, Stability and Profitability of a

project or business.

• Financial analysis is the process of evaluating businesses or projects budgets and

other finance-related transactions to determine their performance and suitability.

Typically, financial analysis is used to analyse whether an entity is stable, solvent,

liquid, or profitable enough to warrant a monetary investment

• A financial analysis will not only help to understand project’s (company’s) financial

condition, but it also helps to determine its creditworthiness, profitability and ability

to generate wealth. It will also provide a more in-depth look at how well it operates

internally.

5.

Important Aspect ofFinancial Analysis

Important Aspects which have to be considered in financial analysis are :

I. Cost of project

II. Means of financing

III. Estimates of sales and production

IV. Cost of production

V. Project Cash flows

Cost of aProject

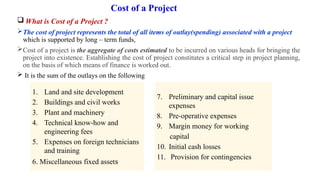

What is Cost of a Project ?

The cost of project represents the total of all items of outlay(spending) associated with a project

which is supported by long – term funds,

Cost of a project is the aggregate of costs estimated to be incurred on various heads for bringing the

project into existence. Establishing the cost of project constitutes a critical step in project planning,

on the basis of which means of finance is worked out.

It is the sum of the outlays on the following

1. Land and site development

2. Buildings and civil works

3. Plant and machinery

4. Technical know-how and

engineering fees

5. Expenses on foreign technicians

and training

6. Miscellaneous fixed assets

7. Preliminary and capital issue

expenses

8. Pre-operative expenses

9. Margin money for working

capital

10. Initial cash losses

11. Provision for contingencies

8.

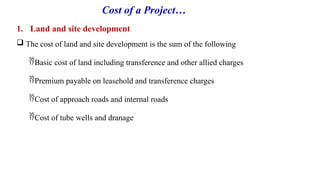

Cost of aProject…

1. Land and site development

The cost of land and site development is the sum of the following

Basic cost of land including transference and other allied charges

Premium payable on leasehold and transference charges

Cost of approach roads and internal roads

Cost of tube wells and dranage

9.

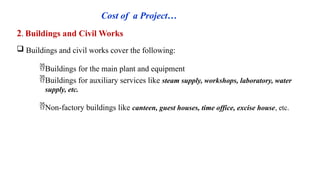

Cost of aProject…

2. Buildings and Civil Works

Buildings and civil works cover the following:

Buildings for the main plant and equipment

Buildings for auxiliary services like steam supply, workshops, laboratory, water

supply, etc.

Non-factory buildings like canteen, guest houses, time office, excise house, etc.

10.

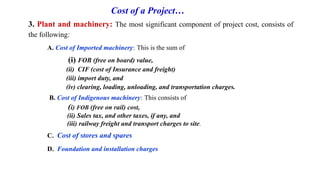

Cost of aProject…

3. Plant and machinery: The most significant component of project cost, consists of

the following:

A. Cost of Imported machinery: This is the sum of

(i) FOB (free on board) value,

(ii) CIF (cost of Insurance and freight)

(iii) import duty, and

(iv) clearing, loading, unloading, and transportation charges.

B. Cost of Indigenous machinery: This consists of

(i) FOB (free on rail) cost,

(ii) Sales tax, and other taxes, if any, and

(iii) railway freight and transport charges to site.

C. Cost of stores and spares

D. Foundation and installation charges

11.

Cost of aProject…

4. Technical know-how and engineering fees

• It is necessary to engage technical consultants for advice and help in various

technical matters like preparation of project report, choice of technology,

selection of plant and machinery, detailed engineering, and so on.

5. Expenses on foreign technicians and training :

• Services of foreign technicians may be required for setting up the project

and supervising the trial runs.

12.

Cost of aProject…

6. Miscellaneous fixed assets:

• Fixed assets and machinery which are not part of the direct manufacturing

process may be referred to as miscellaneous fixed assets.

• They include items like

• furniture,

• office machinery and equipment,

• tools, vehicles,

• laboratory equipment and so on.

• Expenses incurred for procurement or use of patents, licenses, trademarks,

copyrights, etc

13.

Cost of aProject…

7. Preliminary and capital issue expenses

• Preliminary expenses are costs to form a project or company. It include cost of

- Identifying the project,

- Conducting the market survey,

- Preparing the feasibility report,

- Example of preliminary expenses: Legal cost( gov’t & court related fees,

Professional fees(Lawyers, etc.), Stamp duty, Printing and postage fees

• Capital Expenses are:

- Underwriting commission,

- Brokerage,

- Fees to managers and registrars,

- Advertising and publicity expenses,

- Listing fees

14.

Cost of aProject…

8. Pre-operative expenses:

• Pre-operative expenses are those expenses incurred by a project before commencement/beginning/ of

commercial operations; or before starting to earn income.

• Pre-operating Expenses means the investigative fees, costs and expenses incidental to the creation of the Company

and the fees, costs and expenses incurred in connection with the commencement of operations of the project

• Note that: Pre-operative are distinct from preliminary expenses or formation expenses.

• Common examples of pre-operating expenses include:

• Recruitment and training of staff before opening

• Market research

• Site visits

• Regulatory expenses (e.g. permits, licenses)

• Administrative expenses (e.g. office rental, stationery)

• Tuition for training programs, seminars, and other educational services

• Minor, pre-opening repair work on buildings for rent

15.

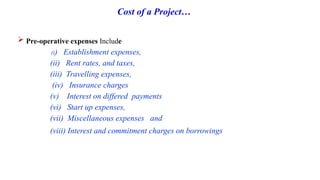

Cost of aProject…

Pre-operative expenses Include

(i) Establishment expenses,

(ii) Rent rates, and taxes,

(iii) Travelling expenses,

(iv) Insurance charges

(v) Interest on differed payments

(vi) Start up expenses,

(vii) Miscellaneous expenses and

(viii) Interest and commitment charges on borrowings

16.

Cost of aProject…

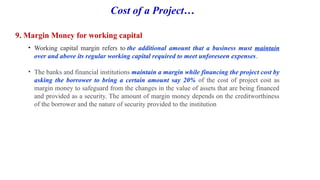

9. Margin Money for working capital

• Working capital margin refers to the additional amount that a business must maintain

over and above its regular working capital required to meet unforeseen expenses.

• The banks and financial institutions maintain a margin while financing the project cost by

asking the borrower to bring a certain amount say 20% of the cost of project cost as

margin money to safeguard from the changes in the value of assets that are being financed

and provided as a security. The amount of margin money depends on the creditworthiness

of the borrower and the nature of security provided to the institution

17.

Cost of aProject…

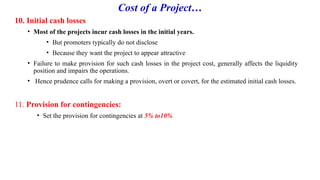

10. Initial cash losses

• Most of the projects incur cash losses in the initial years.

• But promoters typically do not disclose

• Because they want the project to appear attractive

• Failure to make provision for such cash losses in the project cost, generally affects the liquidity

position and impairs the operations.

• Hence prudence calls for making a provision, overt or covert, for the estimated initial cash losses.

11. Provision for contingencies:

• Set the provision for contingencies at 5% to10%

Means of Finance

ToMeet the Cost of Project the following are the means of

finances that available:

1. Share Capital

2. Term Loans

3. Deferred Payment

5. Incentive Sources

6. Miscellaneous Sources

20.

To Meet theCost of Project…

1. Share capital

There are two types of share capital: equity capital and preference capital.

• Equity capital: Represents the contribution made by the owners of the

business, the equity shareholders, who enjoy the rewards and bear the risks of

ownership. .

• Preference capital: represents the contribution made by preference

shareholders and the dividend paid on it is generally fixed.

21.

To Meet theCost of Project…

2. Term loans

It is provided by financial institutions and commercial banks,

Term loans represent secured borrowings which are a very important source (and

often the major source) for financing new projects as well as expansion,

moderation, and renovation schemes of existing firms.

A term loan is usually meant for equipment, machinery, real estate, or working

capital paid off between one and 25 years ( short , medium and long term loan). A

small business often uses the cash from a term loan to purchase fixed assets, such

as equipment or a new building for its production process.

22.

To Meet theCost of Project…

3. Deferred credit

• Money that has been received by a business/investment project/ but has

not yet been shown in the accounts as income,

• Payment received in advance for goods that have not yet been provided:

• Many a time the suppliers of plant and machinery offer a deferred credit

facility under which payment for the purchase of plant and machinery can

be made over a period of time.

23.

To Meet theCost of Project…

5. Incentive sources

• The government and its agencies may provide financial support as incentive to

certain types of promoters or for setting up industrial units in certain locations.

• These incentives may take the form of

• Seed capital, assistance capital, subsidy (to attract industries to certain

locations), or

• Tax exemption (particularly from sales tax) for a certain period.

24.

To Meet theCost of Project…

6. Miscellaneous sources: such as unsecured loans,

Unsecured loans

• are loans that don’t require collateral

• also referred to as signature loans because a signature is all that’s needed if

you meet the lender’s borrowing requirements

• Because lenders take on more risk when loans aren’t backed by collateral,

they might charge higher interest rates and require good or excellent credit

returning history..

• Personal loan, student loan and credit cards are example of unsecured loan

Estimates of salesand production

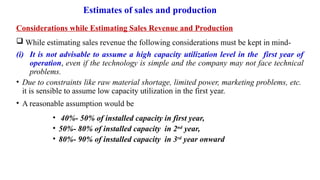

Considerations while Estimating Sales Revenue and Production

While estimating sales revenue the following considerations must be kept in mind-

(i) It is not advisable to assume a high capacity utilization level in the first year of

operation, even if the technology is simple and the company may not face technical

problems.

• Due to constraints like raw material shortage, limited power, marketing problems, etc.

it is sensible to assume low capacity utilization in the first year.

• A reasonable assumption would be

• 40%- 50% of installed capacity in first year,

• 50%- 80% of installed capacity in 2nd

year,

• 80%- 90% of installed capacity in 3rd

year onward

27.

Estimates of salesand production…

ii. It is not necessary to make adjustment for stocks of finished goods. For practical

purposes, it may be assumed that production would be equal to sales.

Sales = Production

iii. The selling price considered should be the price realizable by the company net of

excise duty. It shall, however, include dealers’ commission which is shown as an

item of expense as part of sales expenses.

iv. The selling price used may be the present selling price:

• it is generally assumed that changes in selling price will be matched by

proportionate changes in cost of production. Sales and production are closely

interred –related. Hence they may be estimated together.

28.

Estimates of salesand production…

In order to make estimates of Sales and Production the following details must be

furnished for each product and until the maximum capacity utilization of the plant:

1.Installed Capacity

2.Number of working days

3.Number of shifts

4.Estimated production per day

5.Estimated annual production

6.Estimated output as a percentage of plant capacity

7.Sales after adjusting stocks

8.Value of sales

Cost of production

The major components of cost of production are:

1.Material Cost

2. Overhead Cost

3. Utilities Cost

4. Labor cost

31.

Cost of production

1.Materials Cost

• Includes cost of raw materials, chemicals, components, and other inputs

required for production.

• These costs may be determined on the basis of

• theoretical consumption norms,

• industry experience , or

• specification provided by machinery suppliers.

32.

Cost of production

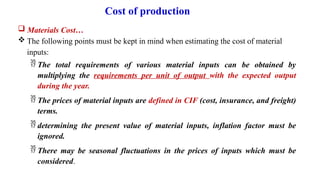

Materials Cost…

The following points must be kept in mind when estimating the cost of material

inputs:

The total requirements of various material inputs can be obtained by

multiplying the requirements per unit of output with the expected output

during the year.

The prices of material inputs are defined in CIF (cost, insurance, and freight)

terms.

determining the present value of material inputs, inflation factor must be

ignored.

There may be seasonal fluctuations in the prices of inputs which must be

considered.

33.

Cost of production

2.Overheads Cost

• Often referred to as overhead or operating expenses,

• Refer to those expenses associated with running a business that can not be linked

to creating or producing a product or service.

• are the expenses the business incurs to stay in business, regardless of its success

level.

• The expenses on repairs and maintenance, rent, taxes, insurance on factory assets,

and so on are collectively referred to as factory overheads

34.

Cost of production…

3.Utilities Cost

Includes cost of power, water, fuel , etc.

The cost of power includes bought out power estimated on the basis of charges of the

concerned electricity board.

The cost of water include chares paid to local authorities

Cost of fuel consists of cost involved in buying coal, fire, wood, bio gas, etc.

35.

Cost of production…

4.Labor cost

Includes cost of all manpower employed .

It is a function of the number of employees and the rate of remuneration.

Manpower includes the number of operators for operating various machines,

services, number supervisory and administrative staff

Introduction to FinancialAnalysis

Methods of financial analysis

• To assess financial viability of a project a range of tools and methods can be used

and various types of financial statements can be prepared. This includes:

1. Resource flow statements

2. Profit and loss statements

3. Cash flow statements and

4. Balance Sheet

38.

Statement of CashFlow

What is Statement of Cash flow or cash flow Statement?

The statement of cash flow :

• Describe how a company spends its money (cash outflows) and from where a

company receives its money (cash inflows).

• Includes all cash inflows a company receives from its (1) ongoing operations and

(2) external investment sources, as well as (3) all cash outflows that pay

for business activities and investments during a given period ( annually,semi-

annually, or quarterly).

39.

Statement of CashFlow

Cash flow statements are prepared for two reasons:

First, it is prepared for financial planning purpose: in this case, the purpose is

• to know the liquidity position of the project.

• to helps project planners to identify potential periods of cash shortages and enables them

to plan appropriate responses designed to remove such shortages or how to utilize excess

amount of fund during the life of the project.

Secondly, cash flow statement may be prepared for the purpose of Net Present Value (NPV),

Benefit Cost Ratio (BCR) and Internal Rate of Return (IRR) calculation. The purpose here is

to measure the overall profitability of the project.

40.

Cash Flow Statement

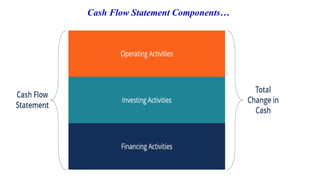

Components of Cash Flow Statement

There are three main components of a cash flow statement. These are:

1. Cash flow from operations,

2. Cash flow from investing, and

3. Cash flow from financing.

Cash Flow Statement

Components of Cash Flow Statement…

1. Cash flow from Operating Activities

• is the net amount of cash coming in or leaving from in day to day business

operations of an entity

• arise from the activities a business uses to produce net income.

• Include:

- Cash flow from sales;

- Cash used to purchase inventory;

- Cash to pay for operating expenses such as salaries and utilities;

- Cash flows from interest and dividend revenue interest expense, and

income tax

43.

Cash Flow Statement

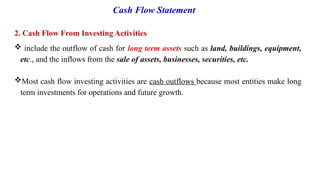

2.Cash Flow From Investing Activities

include the outflow of cash for long term assets such as land, buildings, equipment,

etc., and the inflows from the sale of assets, businesses, securities, etc.

Most cash flow investing activities are cash outflows because most entities make long

term investments for operations and future growth.

44.

Cash Flow Statement

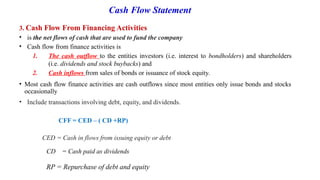

3.Cash Flow From Financing Activities

• is the net flows of cash that are used to fund the company

• Cash flow from finance activities is

1. The cash outflow to the entities investors (i.e. interest to bondholders) and shareholders

(i.e. dividends and stock buybacks) and

2. Cash inflows from sales of bonds or issuance of stock equity.

• Most cash flow finance activities are cash outflows since most entities only issue bonds and stocks

occasionally

• Include transactions involving debt, equity, and dividends.

CFF = CED – ( CD +RP)

CED = Cash in flows from issuing equity or debt

CD = Cash paid as dividends

RP = Repurchase of debt and equity

45.

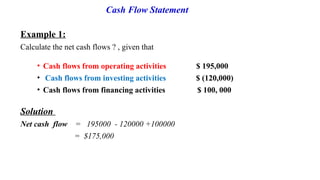

Example 1:

Calculate thenet cash flows ? , given that

• Cash flows from operating activities $ 195,000

• Cash flows from investing activities $ (120,000)

• Cash flows from financing activities $ 100, 000

Solution

Net cash flow = 195000 - 120000 +100000

= $175,000

Cash Flow Statement

46.

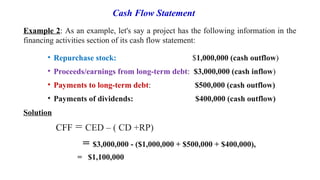

Example 2: Asan example, let's say a project has the following information in the

financing activities section of its cash flow statement:

• Repurchase stock: $1,000,000 (cash outflow)

• Proceeds/earnings from long-term debt: $3,000,000 (cash inflow)

• Payments to long-term debt: $500,000 (cash outflow)

• Payments of dividends: $400,000 (cash outflow)

Solution

CFF = CED – ( CD +RP)

= $3,000,000 - ($1,000,000 + $500,000 + $400,000),

= $1,100,000

Cash Flow Statement

47.

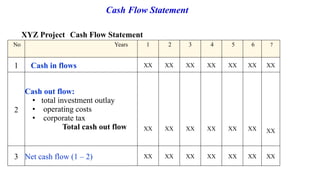

Cash Flow Statement

NoYears 1 2 3 4 5 6 7

1 Cash in flows XX XX XX XX XX XX XX

2

Cash out flow:

• total investment outlay

• operating costs

• corporate tax

Total cash out flow XX XX XX XX XX XX XX

3 Net cash flow (1 – 2) XX XX XX XX XX XX XX

XYZ Project Cash Flow Statement

48.

Example 3:

Based onthe information given in the table below ( the nest slide) of cash flow

statement, fill the shaded region by

a) Determining the cash inflow of each quarter?

b) Calculating the cash outflow of each quarter?

c) Determine the net cash flow of each quarter?

d) Calculating the cumulative net cash flow?

Cash Flow Statement

49.

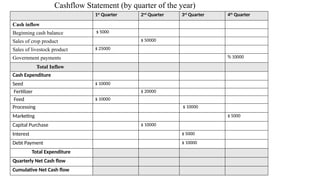

Cashflow Statement (byquarter of the year)

1st

Quarter 2nd

Quarter 3rd

Quarter 4th

Quarter

Cash inflow

Beginning cash balance $ 5000

Sales of crop product $ 50000

Sales of livestock product $ 25000

Government payments % 10000

Total Inflow

Cash Expenditure

Seed $ 10000

Fertilizer $ 20000

Feed $ 10000

Processing $ 10000

Marketing $ 5000

Capital Purchase $ 10000

Interest $ 5000

Debt Payment $ 10000

Total Expenditure

Quarterly Net Cash flow

Cumulative Net Cash flow