Download to read offline

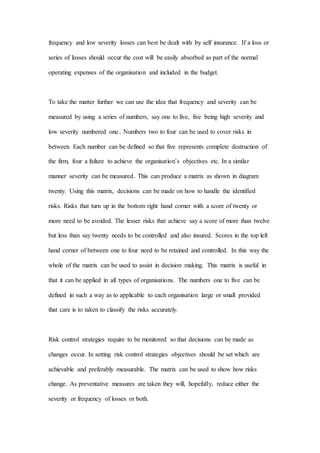

This document discusses different methods of financial risk control, including internal and external risk financing. Internal risk financing involves funding losses from regular earnings, creating a fund to cover large losses, or self-insuring. External risk financing primarily uses insurance. The document outlines different types of insurance policies, including liability insurance, employer's liability, professional indemnity, products liability, and personal accident insurance. It provides details on how each policy covers losses and exceptions to the coverage.