TABLE OF CONTENTS:

•DEFINITION OF RISK

• METHODS OF HANDLING RISK

• INSURANCE AS A DEVICE FOR HANDLING RISK

• BUSINESS AND THE USE OF LIFE INSURANCE

• FIRE INSURANCE

• MOTOR CAR INSURANCE

• MARINE INSURANCE

• GENERAL LIABILITY INSURANCE

• SURETY BONDS

• MISCELLANEOUS INSURANCE LINES

3.

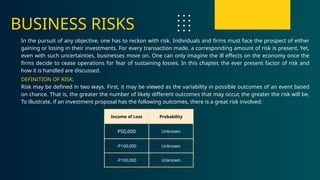

Income of LossProbability

P50,000 Unknown

-P100,000 Unknown

-P100,000 Unknown

BUSINESS RISKS

In the pursuit of any objective, one has to reckon with risk. Individuals and firms must face the prospect of either

gaining or losing in their investments. For every transaction made, a corresponding amount of risk is present. Yet,

even with such uncertainties, businesses move on. One can only imagine the ill effects on the economy once the

firms decide to cease operations for fear of sustaining losses. In this chapter, the ever present factor of risk and

how it is handled are discussed.

DEFINITION OF RISK:

Risk may be defined in two ways. First, it may be viewed as the variability in possible outcomes of an event based

on chance. That is, the greater the number of likely different outcomes that may occur, the greater the risk will be.

To illustrate, if an investment proposal has the following outcomes, there is a great risk involved:

4.

METHODS OF

HANDLING RISK

Experienceshave led mankind to adopt ways of

handling risk. The methods are more pronounced when

applied to business finance. These methods are the

following:

1.risk may be avoided;

2.risk may be retained;

3. hazard may be reduced;

4. loss may be reduced;

5. risk may be shifted; and

6. risk may be reduced.

5.

A businessman whowants to avoid the risk of losing his building to fire, may do so by

simply avoiding the ownership of one. In fact, there are ways of avoiding risk. One of

them is through leasing.

There are instances when risk cannot be avoided. They are simply retained. As not all

properties are good objects of lease agreements, the ownership of some cannot be

avoided. The risks inherent to ownership are, then, retained. An example is the

unavoidable ownership of small items like ballpens and pencils.

Hazards are those conditions that create or increase the chance of loss. An unlighted

stairway is a hazard that may cause accidents in a factory. Potential losses may be

reduced by providing suitable lighting along the stairway.

When losses happen, some actions may be done to minimize such losses. When car

accidents happen, injuries to the driver and passengers may be reduced with the use

of seatbelts. When buildings are physically separated, the chance of losing all the

buildings in the event of a fire is minimized. Big corporations prohibit their key

employees from traveling in one group and boarding the same plane. The reason for

this is obvious. The firms do not want to lose their key personnel in one unfortunate

event. Hedging, subcontracting, the use of surety bonds, incorporation, and

insurance are examples of shifting risks to another party.

6.

fire

marine

motor car

liability

crime

glass

boiler and

machinery

credit

Effectivemanagerial control tends to reduce risk. Examples are materials control

systems, audits and other accounting controls, and process and product

inspection plans.

Figure 21. Methods of Handling Risk

The most common device used in handling risk is insurance. Most risks that are related to

business operations may be covered by insurance policies currently sold in the market. In

spite of this however, the Filipino businessman is not very keen in availing of the services

provided by insurance firms.

INSURANCE AS A DEVICE FOR HANDLING RISK

7.

INSURANCE DEFINED

Insurance maybe defined in various ways. From the legal viewpoint, a contract of insurance is an

agreement whereby one undertakes for a consideration, to indemnify another against loss,

damage, or liability arising from an unknown or contingent event. From the viewpoint of business

economics, insurance is an economic device used to reducing risk by combining a sufficient

number of exposure units to make their individual losses collectively predictable.

THE INSURANCE POLICY

The insurance policy is the written instrument in which a contract of insurance is set

forth. It contains the following:

Declarations. The nature of the risk is described in the "declarations" which are usually found on

the first page of an insurance policy. Information related to the following are included

1. declarations;

2. insuring

agreements;

3. exclusions; and

4. conditions

1. subjects covered, such as machinery and installations in a fire policy;

2. person or persons insured, such as Mr. Roberto Montevirgen or Mr. and Mrs. Rodolfo Padua;

3. the premium to be paid, which includes all or some of the following:

a the rate of premium expressed in percentage;

b. the amount of premium;

c. the amount of documentary stamps payable;

d. the amount of premium tax payable; and

e. the amount of fire service tax payable (applicable to fire policies).

8.

4. the periodof coverage, such as 12:00 noon, June 7, 2005 to 12:00 noon, June 7, 2006;

5. policy limits or amounts of insurance, such as ONE MILLION PESOS (P1,000,000.00) PHILIPPINE CURRENCY;

and

6. warranties or promises made by the insured with respect to the nature and control of the hazard, such as

Non-Hazardous Chemists and Druggists Warranty.

Insuring Agreements. The insuring agreements is that part of the policy which states what the insurer agrees

to do and the major conditions under which it agrees. The insurer promises to compensate the insured if a loss

under the insured peril occurs and if the insured meets the conditions of the contract. The insurer has no

obligation to pay if the conditions are not met.

The insuring agreements in a personal accident policy, for instance, usually include the table of benefits,

provisos, and general conditions.

Conditions. Conditions may be general or specific. The general conditions usually cover the following:

1. conditions or payment of premium;

2. notices required;

3. evidence of loss;

4. cancellation;

5. short-period rate scale;

6. arbitration clause;

Exclusions. An exclusion is a provision or part of the insurance contract limiting the scope of Death and

disablement due to war and invasion, for example, are excluded in the risks covered by a personal accident

policy.coverage. Exclusions comprise certain causes and conditions listed in the policy which are not covered.

7. agreement on the effect of legal provision on extra-ordinary inflation;

8. omnibus clause;

9. important notice;

10. action or suit clause; and

11. settlement clause.

9.

TYPES OF INSURANCE

COVERAGES

Insurancecontracts may be classified as either life or non-life.

LIFE COVERAGES

Insurance contracts may be classified as either life or non-life. Life coverages are those relating directly to the

individual. The risk covered is the possibility that some peril may interrupt the income that is earned by an

individual. The perils relating to life coverages consist of the following:

1. death;

2. accidents and sickness;

3. unemployment; and

4. old age.

Insurance is written on each of the four perils.

NON-LIFE COVERAGES

A non-life coverage refers to insurance other than life. Included in non-life coverages are:

1. Fire and allied risks;

2. Marine;

3. Casualty;

4. Surety; and

5. Liability.

Non-life insurance is distinguished from life insurance in that life insurance covers perils that may prevent one

from earning money with which to accumulate property in the future, while non-life insurance covers property

that is already accumulated. Non-life insurance is also referred to as general insurance.

10.

BASIC TYPES OFLIFE INSURANCE CONTRACTS

There are quite a number of life insurance policies which are offered for sale in the market to meet the varying needs of individuals and

business firms. All are either whole life, term, or endowment, or a combination of one or more of these. Such combinations include

annuities, since they form part of the life insurance business. This condition makes life insurance contracts into four basic types:

1.whole life;

2.term;

3.endowment; and

4.annuities.

Whole life insurance is a kind of life insurance which is kept in force until death so long as premiums are paid, regardless of age and the time

period. It is a permanent form of insurance and covers the insured for life. The phrase covers the insured for his whole life is the basis for

naming this particular kind of insurance contract.

Classes of Whole Life Insurance Policies. Based on the method of premium payment, there are three classes of whole life insurance

policies:

(1) single-premium;

(2) continuous-premium; and

(3) limited payment policies.

• Single-premium whole life policies are those for which, in exchange for one premium, the insurer promises to pay the claim whenever

death occurs.

• Continuous-premium whole life policies are those for which the insured pays the same premium amount continuously as long as he is

alive.

• Limited-payment whole life policies belong to the type of insurance plan under which the premiums are paid for a limited period of years,

after which no further premium payments need to be made.

WHOLE LIFE INSURANCE

11.

TEAM INSURANCE

A terminsurance policy is a contract between the insured and insurer whereby the insurer

promises to pay the face amount of the policy to a third party (the beneficiary) if the insured

dies within a specified time period.

Term insurance, as its name implies, is insurance for a term, or temporary period. Whole life

insurance, in contrast, is permanent insurance and covers as long as the insured lives. Term

insurance, when written for a year, provides protection equal to the face value of the policy for

only one year. When written for five years, the coverage is only for five years. At the end of the

specified period, whether for one year or five years, the coverage is terminated, and the policy

no longer has value.

TYPES OF TERM POLICIES

Term insurance policies are classified as follows:

1.Straight term policies which are written for a specific number of years and then automatically

terminated;

2.Long-term policies written to terminate at some specified age of the insured, commonly 65;

3.Renewable term insurance which may be renewed by the insured before expiry date, without again

proving insurability;

4.Convertible term policies which may be converted into whole life or endowment insurance within

specified period, without evidence of insurability;

5.Increasing term insurance, the policy amount of which increases monthly or yearly; and

6.Decreasing term insurance, the face value of which reduces periodically, either monthly or yearly.

12.

ENDOWMENT INSURANCE

Endowment insuranceis a contract under which the insurer promises to pay the beneficiary a stated sum if

the insured dies during the policy term, or to the insured if the policy term is survived. The policy term is also

referred to as the “endowment period”.

Types of Endowment Insurance.

Endowment insurance may be classified according to the following:

1.The term for which they are written may vary from 5 to 40 years;

2.The designated age of maturity to which they are written, such as 60 to 65 years; and

3.The period of premium payment, such as the limited payment endowment, where the endowment is

payable at death or at the end of the endowment period.

An annuity is a series of payments made at certain specified intervals. Annuities are written either (1) as

separate contracts, or an individual or group basis; or (2) as supplementary contracts, using the proceeds of a

life insurance contract to purchase an annuity benefit.

ANNUITIES

BUSINESS AND THE USE OF LIFE INSURANCE

The employees of a firm constitute a very important investment. Possible liabilities of the company may arise

when employees are injured or killed in work-related accidents. The moral obligation of the employer is to

provide for such type of needs. If these are not provided for through insurance, the funds of the firm which are

earmarked for other uses, may be jeopardized. The various types of life insurance contracts available provide

solution to such possible difficulties.

13.

FIRE INSURANCE

Fire isone of the most destructive perils known to man. It kills people and it destroys properties. As people

and properties are important business resources, some device must be used to protect both. News reports

abound about properties and lives lost due to fire.

A fire insurance contract covers all direct losses and damages by fire or lightning and by removal from premises

endangered by fire. In the attempt to rescue property, losses due to theft may occur. Such losses are also covered by a

fire policy.

Other allied perils may be covered in a fire insurance contract, provided they are specifically named in the policy. The

allied perils refer to the following:

1.earthquake fire;

2.earthquake shock;

3.windstorm, typhoons, and flood;

4.riot and strike damage and riot fire; and

5.explosions.

Perils Covered

Fire insurance contracts are designed to cover any of the following:

1.building;

2. contents of the building like machinery, appliances, furniture and fixtures, stock-in-trade, and others; or

3. both building and contents.

What May Be Insured

14.

MOTOR CAR INSURANCE

Mostbusiness firms cannot avoid the ownership of motor vehicles. Conveyances are needed by the firm for

transporting goods and persons. Its executives will need cars in the performance of their assigned jobs.

Products need to be delivered to customers. Supplies need to be fetched from where they were bought.

Employees need to be transported from their homes to their place of work and vice versa. All these needs will

require the firm to own motor vehicles. Owning a vehicle, however, entails some risks inherent to such

undertaking. These risks include possible irtjuries to persons or damage to properties. Fortunately, insurance

policies may be bought to cover such risks.

The types of insurance coverages applicable to motor car are the following:

1. Compulsory Third Party Liability (CTPL);

2. Third Party Property Damage (TPPD);

3. Passenger Liability (PL);

4. Own Damage (OD) and theft, and

5. Personal accident coverage for drivers and passengers of private and commercial vehicles.

Compulsory Third Party Liability. The compulsory third party liability (CTPL) insurance covers loss or damage

inflicted upon third parties owing to the use of a motor car. Loss or damage refers to pedestrians or passengers of other

vehicles who may be injured or killed by a vehicle driven by a person.

CTPL provides for death benefits, burial, and hospitalization expenses amounting to a maximum of 50,000 depending on

the classification of the vehicle. The maximum amount of coverage could be raised provided additional premiums are paid to

the insurer.

MOTOR VEHICLE INSURANCE COVERAGES

15.

Third Party PropertyDamage. The use of motor vehicles may also cause damage to

property of third parties. This type of loss may be covered by a third party property

damage agreement. Depending on the insurer, maximum coverage for TPPD could

reach more than a hundred thousand pesos.

Passenger Liability. Operators of public utility vehicles may be held liable for death or

injuries inflicted upon passengers. Losses under this type of liability may be covered by

passenger liability (PL) insurance. Maximum coverages differ depending on the type of

vehicle.

Own Damage and Theft. The motor vehicle itself may also be the subject of loss or

damage. A brand new delivery truck, for example, may be damaged by typhoon. The

firm needs protection from such unwanted physical destruction of their vehicles. Such

protection is available through the purchase of own damage (OD) policies. Losses due

to theft are oftentimes available in conjunction with the OD cover.

Personal Accident. The driver and passengers of private and commercial vehicles are

oftentimes left without protection against accidents. Policies may be bought to cover

them against such risks.

Business firms involved in transporting commodities from one seaport to another require protection from possible

losses of such commodities. The type of insurance coverage applicable is called marine insurance.

MARINE INSURANCE

16.

Section 99 ofthe Insurance Code of the Philippines indicates what is included in marine

insurance. These are the following:

1. Insurance against loss or damage to:

a. Vessels, craft, aircraft, vehicles, goods, freights, merchandise, effects, disbursements,

profits, moneys, securities, choses in action, evidence of debt, valuable papers, bottomry, and

respondentia interest and all other kinds of property and interests therein, in respect to,

appertaining to or in connection with any and all risks or perils of navigation, transit or

transportation, or while being assembled, packed. crated, baled, compressed or similarly

prepared for shipment, or while awaiting shipment or reshipment incident thereto, including

war risks, marine builder's risks, and all personal property floater risks.

b. Person or property in connection with or appertaining to a marine, inland marine, including

liability for loss of or damage arising out of or in connection with the construction or repair,

operation, maintenance, or use of the subject matter of such insurance

C. Precious stones, jewels, jewelry, precious metals, whether in course of transportation or

otherwise.

d. Bridges, tunnels, and or other instrumentalities of transportation and communication,

piers, wharves, docks and ships, and other aids to navigation and transportation, including dry

docks and marine railways, dams and appurtenant facilities for the control of waterways.

2. Marine protection and indemnity insurance meaning insurance against, or against legal liability of the insured for

loss, damage, or expense incident to ownership, operation, chartering, maintenance, use, repair, or construction of

any vessel, craft or instrumentality in use in ocean or inland waterways including liability of the insured for personal

injury, illness or death or for loss of or damage to the property of another person.

17.

GENERAL LIABILITY INSURANCE

Businessfirms may at times be subjected to liability claims by other parties. Damages paid to claimants are

sometimes enough to cause bankruptcy to the firm. To protect the firm from such adverse financial difficulties,

some sort of insurance cover is required. Such need is covered by liability insurance policies.

General liability exposures may be classified into three broad areas: (1) business liability; (2) professional liability; and

(3) personal liability. The first class concerns business and it may be covered by business liability forms. These forms

consist of the following:

1. Owners', landlords', and tenants' form:

2 Manufacturers' and contractors' form;

3. Comprehensive general liability form;

4. Contractual liability form;

5. Owners' and contractors' protective liability insurance;

6. Products and completed-operations liability form;

7 Products recall insurance;

8. Personal injury liability policy;

9. Storekeeper liability policy; and

10. Dramshop liability policy.

BUSINESS LIABILITY FORMS

The firm may also be exposed to possible losses involving the following:

1. The mishandling or misappropriation of goods or funds by employees; and

2. The non-performance of a party who has entered into an agreement with the firm.

The first type of exposure to loss may be covered by fidelity bonds, while the second type may be covered by surety bonds.

SURETY BONDS

18.

FIDELITY BOND

A fidelitybond is one that covers an employee or employees in position/s of probate trust and it guarantees the

employer against loss up to the penalty of the bond should the employee or employees bonded be proven

dishonest.

A surety bond guarantees to the obligee that the principal named in the bond will perform a certain obligation and if

he fails to do so, the surety will perform the obligation or pay the damages up to the amount of the bond.

Surety Bond

There are other types of insurance coverages which may protect the firm from possible financial losses. These are the

following:

1. Crime insurance;

2. Glass insurance;

3. Boiler and machinery insurance; and

4. Credit insurance

MISCELLANEOUS INSURANCE LINES

Crime insurance protects owners of property against losses due to its being wrongfully taken by someone else. Crime

coverages include possible losses from burglary, robbery, larceny, theft, forgery, embezzlement, and other dishonest acts.

Crime Insurance

19.

BOILER AND MACHINERYINSURANCE

The boiler and machinery insurance is a type of insurance contract which provides protection against loss resulting

from the accidental bursting or breaking of a great variety of apparatus.

Credit Insurance

Credit insurance is a contract whereby the insurer promises, in consideration of a premium paid, and subject to

specified conditions as to the persons to whom credit is to be extended, indemnify the insured, wholly or in part,

against loss that may result from the insolvency of persons to whom he may extend credit within the term of

insurance.

Credit insurance may be classified into five types, namely:

1. credit life and credit accident and sickness insurance;

2. accounts receivable insurance;

3. domestic merchandise credit insurance;

4. governmental credit insurance; and

5. export credit insurance.

20.

SUMMARY

Business firms arealways confronted with risks. However, there are several ways of handling

risks: (1) risk avoidance; (2) risk retention; (3) hazard reduction; (4) loss reduction; (5) risk

shifting: and (5) risk reduction. Insurance is the most common device used in handling risks,

The written instrument in which a contract of insurance is set forth is the insurance policy.

Insurance contracts may be classified as either life or non-life. Life insurance contracts consist

of four basic types: (1) whole life; (2) term; (3) endowment; and (4) annuities. Non-life

insurance contracts may be classified as either: (1) fire and allied risks; (2) marine; (3) casualty;

(4) surety; or (5) liability.