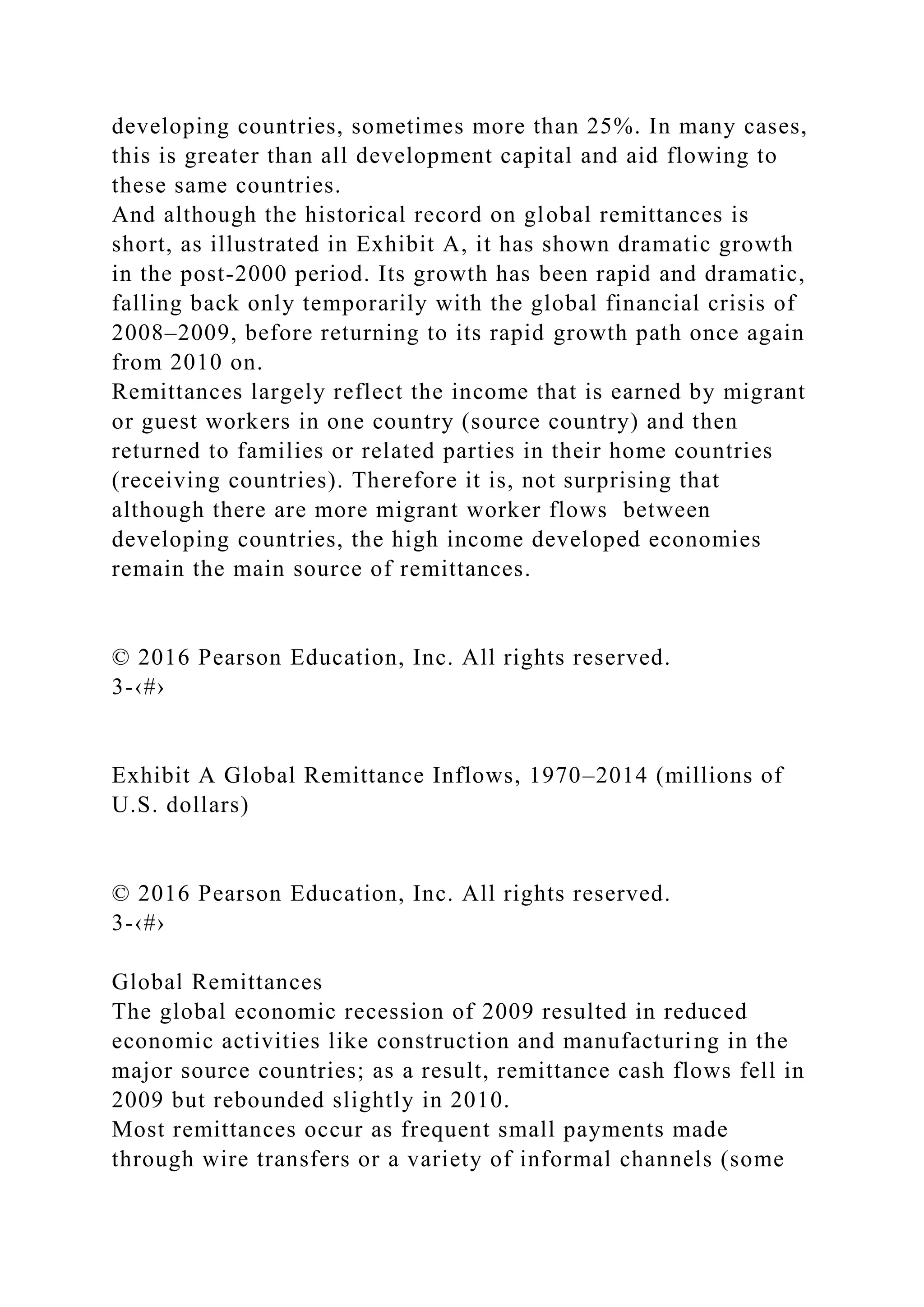

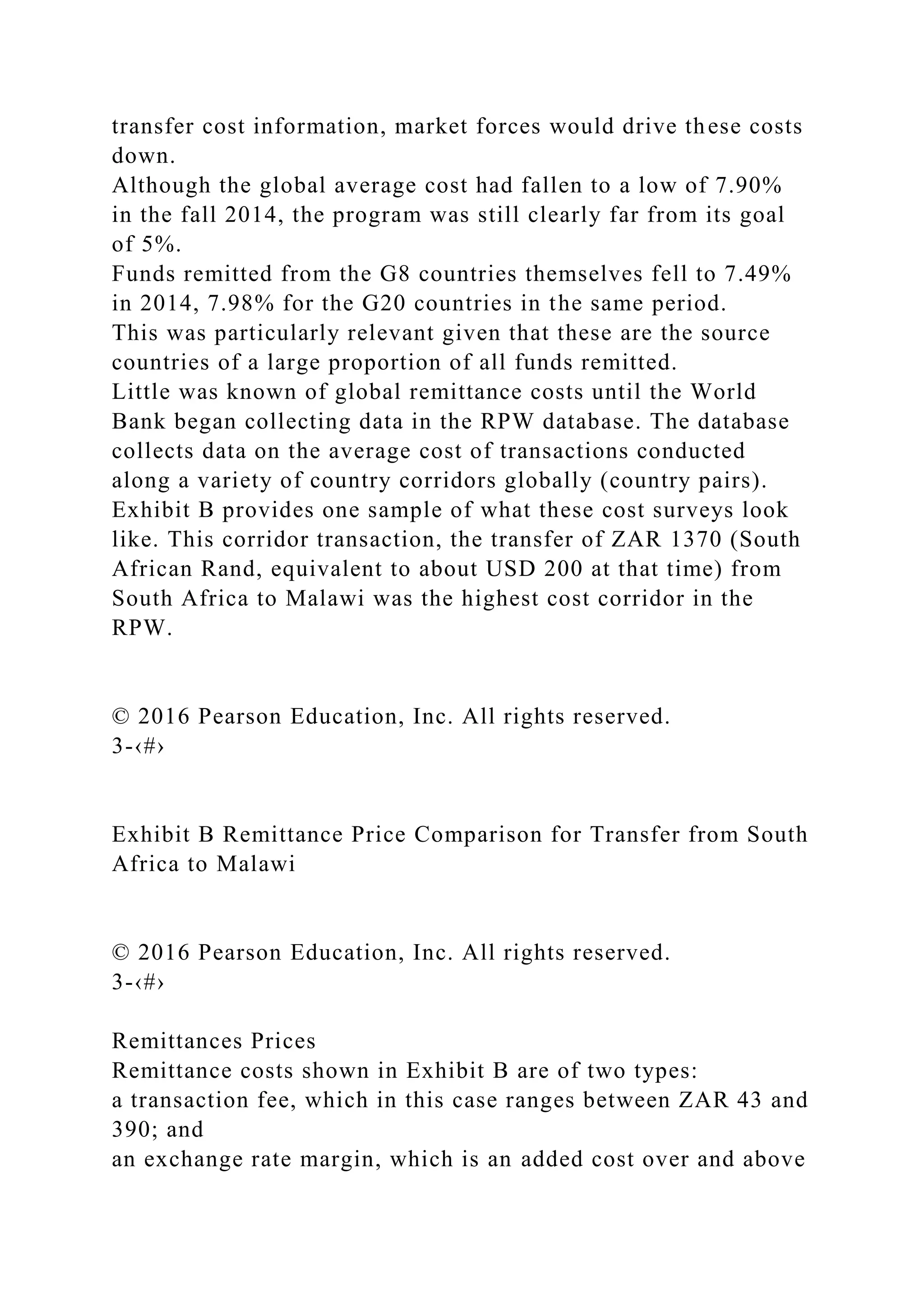

The document discusses global remittances, defining them as international money transfers made by migrant workers to their home countries. It highlights the significant economic impact of remittances, particularly in developing nations where they can constitute over 25% of GDP. The text also addresses the high costs associated with these transfers and the ongoing debates regarding their role in economic development and balance of payments.

![act, in effect, prevented the company from sourc-

ing from farmers directly. Metro also faced much

stronger local opposition, particularly from local

retailers, than it had expected. Overall, regulatory

uncertainty was the major reason a multinational

like Metro struggled in India.

In a similar spirit, more than 300 multinational

executives from diverse firms, industries, and host

* Allison F. Kingsley ([email protected]) is Assistant Professor

of Management at the University of Vermont School of

Business

Administration.

Richard G. Vanden Bergh ([email protected]) is Associate

Professor of Management at the University of Vermont School

of

Business Administration.

Jean-Philippe Bonardi ([email protected]) is Professor at the

Faculty of Business and Economics of the University of

Lausanne.

Copyright of the Academy of Manogement, all rights reserved.

lontents may not be copied, emoiled, posted to a listserv, or

otherwise tronsmitted without the copyright holder's express

written permission.

Users may print, downlood, or email articles for individuol use

only. http://dx.doi.org/10.5465/amp.2012.0042

2012 Kingsley, Vanden Bergh, and Banardi 53

countries were asked in July 2011 to assess the

salience of political risks in their emerging market

investments (World Bank, 2011). Among the re-](https://image.slidesharecdn.com/chapter3minicaseglobalremittances2016pearsone-230110080032-cc39f55e/75/Chapter-3Mini-CaseGlobal-Remittances-2016-Pearson-E-docx-36-2048.jpg)

![J. Account. Public Policy 32 (2013) 1–25

Contents lists available at SciVerse ScienceDirect

J. Account. Public Policy

j o u r n a l h o m e p a g e : w w w . e l s e v i e r . c o m / l o c

a t e / j a c c p u b p o l

Analyst coverage, earnings management and financial

development: An international study

François Degeorge a, Yuan Ding b,⇑ , Thomas Jeanjean c, Hervé

Stolowy d

a Swiss Finance Institute, University of Lugano, Switzerland

b China Europe International Business School (CEIBS),

Shanghai, China

c ESSEC Business School, France

d HEC Paris, France

a b s t r a c t

0278-4254/$ - see front matter � 2012 Elsevier In

http://dx.doi.org/10.1016/j.jaccpubpol.2012. 10.003

⇑ Corresponding author. Address: Department

(CEIBS), 699, Hongfeng Road, Pudong, Shanghai 20

E-mail addresses: [email protected]

s[email protected] (H. Stolowy).

Using data from 21 countries, this paper analyzes the relation

among analyst coverage, earnings management and financial

development in an international context. We document that the

effectiveness of financial analysts as monitors increases with a

country’s financial development (FD). We find that in high-FD

countries, increased within-firm analyst coverage results in less

earnings management. Such is not the case in low-FD countries.](https://image.slidesharecdn.com/chapter3minicaseglobalremittances2016pearsone-230110080032-cc39f55e/75/Chapter-3Mini-CaseGlobal-Remittances-2016-Pearson-E-docx-55-2048.jpg)

![Our results are economically significant and robust to reverse

cau-

sality checks. Our findings illustrate one mechanism through

which financial development mitigates the cost of monitoring

firms and curbs earnings management.

� 2012 Elsevier Inc. All rights reserved.

1. Introduction

A large body of research explores the differences between

financial systems worldwide and docu-

ments the positive effects of financial development: It boosts

industry growth, the formation of new

establishments, and capital allocation (Beck and Levine, 2002).

It predicts capital accumulation and

productivity improvements (Levine and Zervos, 1998). It is

especially important for firms that depend

on external financing (Demirgüç-Kunt and Maksimovic, 1998;

Rajan and Zingales, 1998).

While the benefits of financial development appear to be well

established, the detailed mecha-

nisms through which these benefits are brought to bear are still

largely unknown. Levine (1997) lists

c. All rights reserved.

of Finance and Accounting, China Europe International

Business School

1206, China. Tel.: +86 21 2890 5606; fax: +86 21 2890 5620.

(F. Degeorge), [email protected] (Y. Ding), [email protected]

(T. Jeanjean),

http://dx.doi.org/10.1016/j.jaccpubpol.2012. 10.003

mailto:[email protected]

mailto:[email protected]

mailto:[email protected]](https://image.slidesharecdn.com/chapter3minicaseglobalremittances2016pearsone-230110080032-cc39f55e/75/Chapter-3Mini-CaseGlobal-Remittances-2016-Pearson-E-docx-56-2048.jpg)

![mailto:[email protected]

http://dx.doi.org/10.1016/j.jaccpubpol.2012. 10.003

http://www.sciencedirect.com/science/journal/02784254

http://www.elsevier.com/locate/jaccpubpol

2 F. Degeorge et al. / J. Account. Public Policy 32 (2013) 1–25

five basic functions of a financial system: (1) to facilitate risk

sharing; (2) to allocate resources; (3) to

monitor managers; (4) to mobilize savings; and (5) to facilitate

the exchange of goods and services.

Our paper’s contribution is to focus on the monitoring function;

specifically, on financial analysts as

monitors of firms. We find that higher financial development is

associated with a greater effectiveness

of monitoring by financial analysts. Using a sample of 21

countries from 1994 to 2002, we find that in

countries with highly developed financial systems (hereafter

‘‘high-FD countries’’), increased within-

firm coverage results in less earnings management. Such is not

the case in countries with less well-

developed financial systems (hereafter ‘‘low-FD countries’’).

There is evidence, both systematic and anecdotal, that financial

analysts perform an important

monitoring role, at least in the United States. Dyck et al. (2010)

document that, in the US, financial

analysts are among the quickest detectors of fraud. For example,

in the mid-1990s Sunbeam, an appli-

ance manufacturer, engaged in ‘‘bill-and-hold’’ deals with

retailers: The retailers bought Sunbeam

products at large discounts, but the products were then stored by

the manufacturer at third-party

warehouses for later delivery. In effect, Sunbeam was shifting

revenue from the future to the present.](https://image.slidesharecdn.com/chapter3minicaseglobalremittances2016pearsone-230110080032-cc39f55e/75/Chapter-3Mini-CaseGlobal-Remittances-2016-Pearson-E-docx-57-2048.jpg)

![We would expect monitoring activities to become specialized to

those institutions and individuals

who possess comparative advantages in these activities. One of

the groups who seem to play a large

role in these activities is composed of the security analysts

employed by institutional investors, bro-

kers, and investment advisory services [. . .] To the extent that

security analysts’ activities reduce the

agency costs associated with the separation of ownership and

control they are indeed socially produc-

tive. (Jensen and Meckling, 1976, p. 354).

Analysts have the means to be monitors. Unlike most investors,

they are trained to analyze the

numbers produced by companies and they enjoy privileged

access to company management. Analysts

also have a motive to be monitors. They could look foolish and

see their reputations suffer if their re-

search reports and recommendations were based on manipulated

numbers. Anecdotal evidence, such

as the Sunbeam example given above, suggests that financial

analysts do sometimes perform an

important monitoring role. Dyck et al. (2010) document that in

the United States analysts are among

the quickest monitors of fraud. Yu (2008) finds that US firms

followed by more analysts manage their

earnings less.

Our goal is to assess empirically whether analyst coverage also

functions as a curb on earnings

management in countries that are less financially developed

than the United States. Beck and Levine

(2002) define financial development as ‘‘the degree to which

national financial systems assess firms,

monitor managers, facilitate risk management, and mobilize

savings’’ (p. 160).1 Analysts are more](https://image.slidesharecdn.com/chapter3minicaseglobalremittances2016pearsone-230110080032-cc39f55e/75/Chapter-3Mini-CaseGlobal-Remittances-2016-Pearson-E-docx-62-2048.jpg)