- An imperfectly competitive industry is one where single firms have some control over the price of their output through market power. Market power is a firm's ability to raise prices without losing all demand.

- A pure monopoly is a single firm industry where there are no close substitutes for the product and significant barriers prevent other firms from entering to compete for profits. Barriers to entry include government franchises, patents, large economies of scale, and ownership of scarce resources.

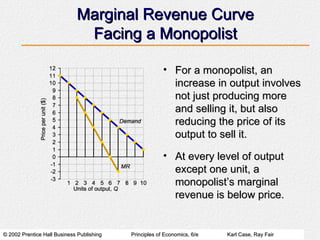

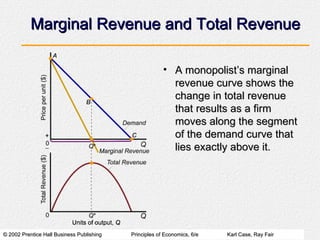

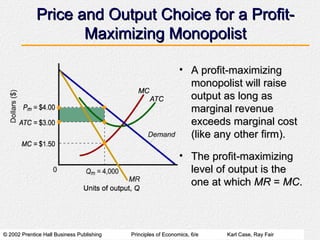

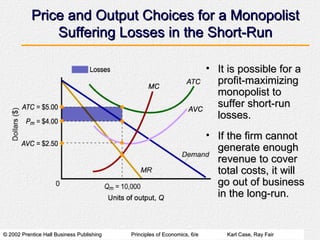

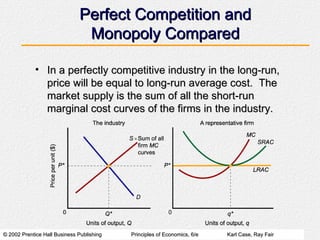

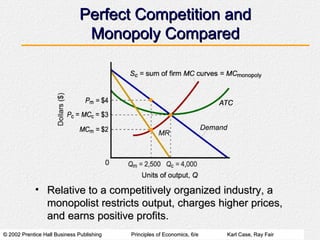

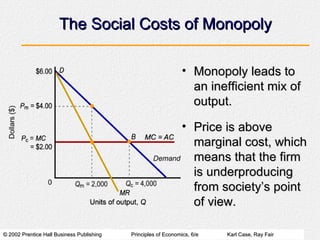

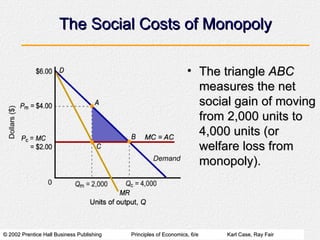

- A profit-maximizing monopolist will produce at the quantity where marginal revenue equals marginal cost to maximize profits. The monopolist restricts output and charges higher prices than under perfect competition, leading to inefficiencies.

![Market structure[1]](https://cdn.slidesharecdn.com/ss_thumbnails/marketstructure1-220223133421-thumbnail.jpg?width=640&height=640&fit=bounds)