Downloaded 11 times

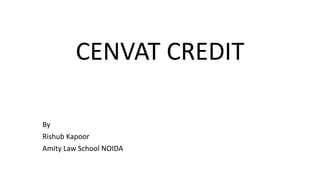

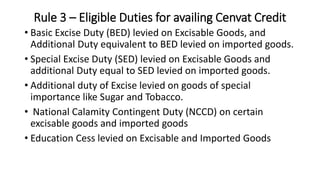

![Rule 4 – Conditions for allowing CENVAT CREDIT

• The cenvat credit in respect of inputs may be taken immediately on the

date of receipt of inputs. CENVAT Credit can be taken any time- even after

three four years- (SAIL vs. CCE 2000RLT CEGAT), (Super Cassette vs. CCE

2004 ELT 280 ( CESTAT))

• The cenvat credit in respect of capital goods to be availed within a period

of 2 years i.e.

a) 50% immediately when capital goods are received and

b) balance 50% in the next financial year.

• Credit allowed to a manufacturer even if capital goods are acquired by him

on lease, hire purchase or loan agreement.

• Credit is allowed even if any inputs or capital goods are sent to job worker

place for further processing, but goods must be received back within 180

days. ( Fiat India v. CCE 2006ELT 439[ CESTAT ])](https://image.slidesharecdn.com/cenvatcredit-171025192852/85/Cenvat-credit-7-320.jpg)

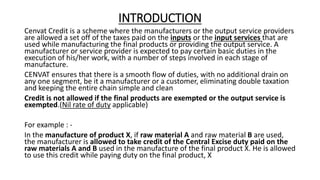

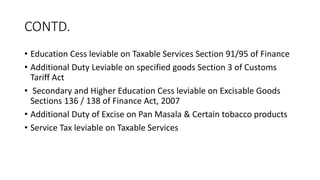

![CONTD.

• Cenvat credit is allowed even in respect of jigs, fixtures, moulds and

dies. (Pricol Ltd vs. CCE [2010] 251 ELT 289[ CESTAT])

• Cenvat credit is not allowed on the goods used for office use.

• Cenvat credit will not be allowed on that part of capital goods that

represents depreciation.

• CENVAT can be availed when the goods were directly delivered to job

worker (Diamond Cables V. CCE) and (Bharat Heavy Electrical v. CCE)

• The CENVAT credit in respect of input service shall be allowed, on or

after the day which payment is made of the value of input service and

the service tax paid or payable as is indicated in invoice, bill or, as the

case may be, challan referred to in rule 9.( Time limit extended from

1 year to 6 months for availment of credit with effect Notification

no. 21/2014- Central Excise dated 11.07.2014 )](https://image.slidesharecdn.com/cenvatcredit-171025192852/85/Cenvat-credit-8-320.jpg)

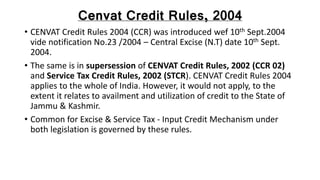

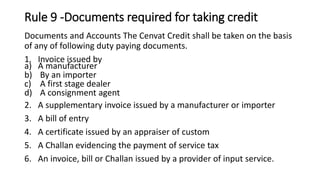

![CENVAT Availment Procedure

Main procedure for CENVAT availment is as follows :

1. Maintaining proper records of input and capital goods.

2. Maintaining records of credit received and utilized.

3. Submit proper returns in forms ER-1 to ER 8.

4. Returns by Dealers / Service Provider / Input Service Providers.

5. All to be filed online at the Icegate platform Of CBEC

Records of Input Services / Capital Goods : Records should contain

information regarding Value, duty paid, CENVAT credit taken & utilized,

person from whom input or capital goods are procured. Here, burden of

proof regarding admissibility of CENVAT Credit is on manufacturer or

provider of output service taking credit. [ Rule 9(5) of CENVAT Credit Rules]](https://image.slidesharecdn.com/cenvatcredit-171025192852/85/Cenvat-credit-10-320.jpg)

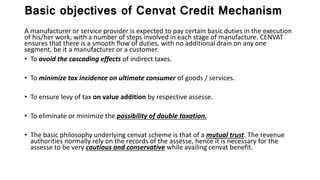

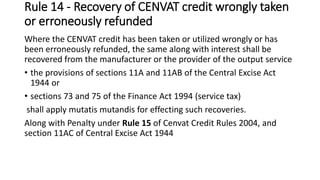

![CONTD.

• Records of Input Services : Records should contain information

regarding Value of input services, Tax Paid, CENVAT Credit taken and

utilised, person from whom input services are procured. The burden

of proof regarding admissibility of CENVAT credit lies with the

person taking credit [ Rule 9(6) of CENVAT Credit Rules]

• CENVAT Credit Record : This is just an account of Cenvat credit

received, credit utilised and credit balance. This gives details of credit

availed against each input / capital goods, Credit utilised against each

clearances of final products or removal of input as such or after

processing or removal of capital goods as such and the Balance Credit

available](https://image.slidesharecdn.com/cenvatcredit-171025192852/85/Cenvat-credit-11-320.jpg)

Cenvat credit is a scheme that allows manufacturers and service providers to claim a credit for taxes paid on inputs and input services against the tax payable on the final product or service. It aims to avoid double taxation and ensure smooth flow of duties. Under Cenvat credit rules, eligible duties include excise duty, customs duty, and service tax. Credit can be claimed by maintaining proper records and filing periodic returns. Credit wrongly taken can be recovered along with interest and penalties. Key cases discuss eligibility of capital goods and input services for credit claiming.