Download to read offline

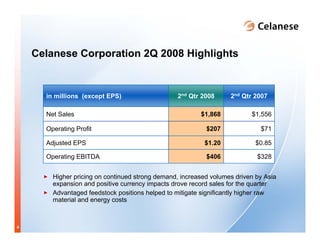

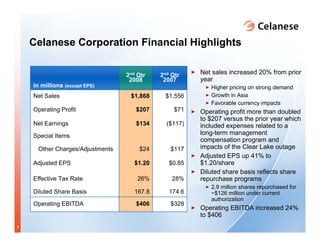

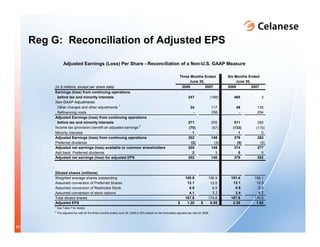

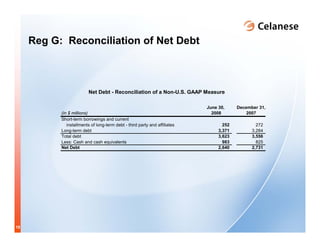

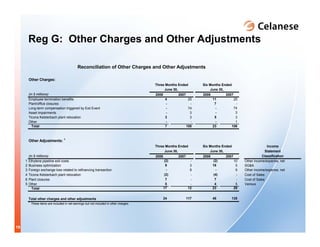

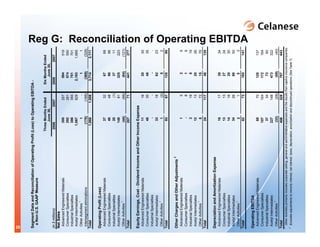

The document summarizes Celanese's 2Q 2008 earnings conference call. It includes an agenda with the Chairman and CEO and SVP and CFO scheduled to speak. It also provides forward-looking statements, non-GAAP reconciliations, and describes results as unaudited. Key highlights are record net sales for the quarter driven by higher pricing and volumes in Asia, though operating profit and EPS declined from significantly higher raw material costs. The company also reaffirms its path to achieving operating EBITDA growth objectives by 2010 through volume growth in advanced materials and further acetate tow penetration.