Download as PDF, PPTX

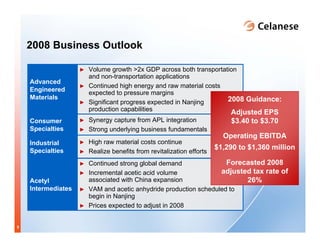

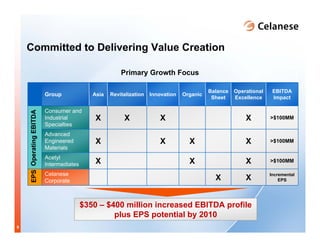

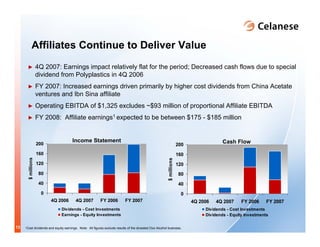

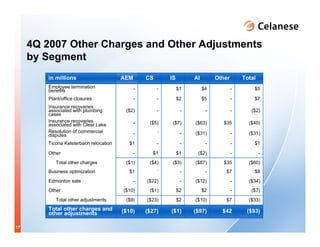

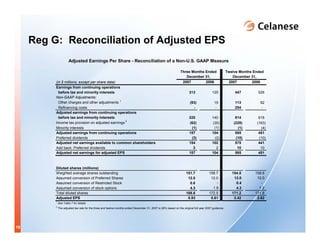

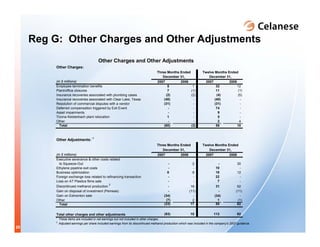

The document summarizes Celanese Corporation's 4Q 2007 earnings conference call. It includes highlights such as a 23% increase in 4Q net sales and a 52% increase in adjusted EPS compared to the same period last year. Celanese also provides guidance for 2008, forecasting adjusted EPS between $3.40-$3.70 and operating EBITDA of $1,290-$1,360 million. Segment results and details on continued strong cash generation are also presented. Key executives Dave Weidman and Steven Sterin will discuss 4Q performance and business outlook further on the earnings call.