Download to read offline

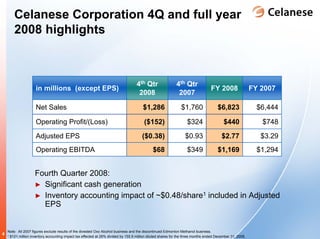

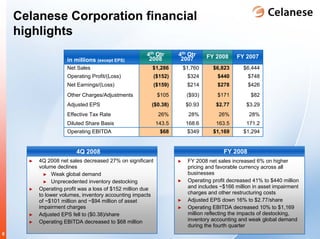

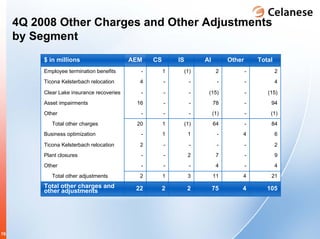

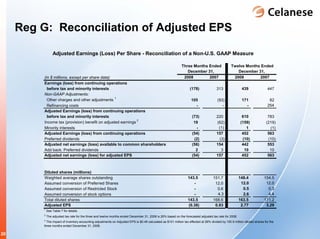

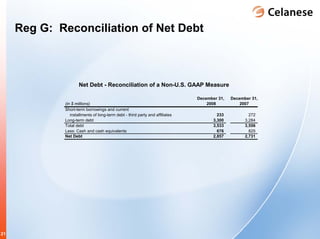

The document summarizes Celanese's 4Q 2008 earnings conference call. It discusses Celanese's 4Q 2008 financial results including a net loss of $152 million compared to an operating profit in 4Q 2007, and an adjusted EPS of ($0.38) compared to $2.77 in 4Q 2007. It also provides highlights for each of Celanese's business segments and discusses the outlook for 2009 including expected continued volume declines.