Download to read offline

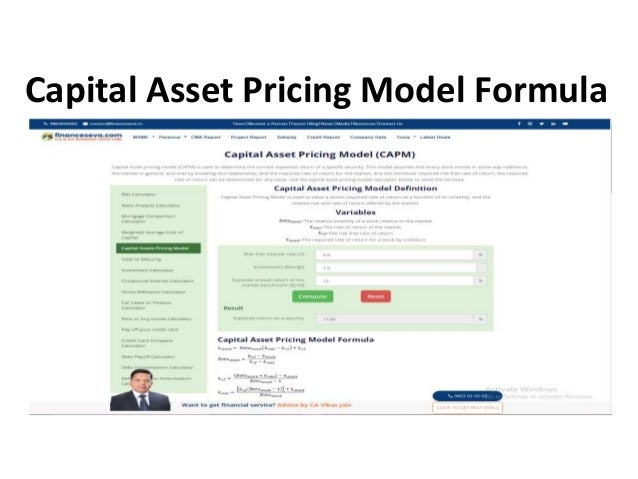

![CAPM Formula and Calculation

CAPM is calculated according to the following formula:

Ra = Rrf + [Ba * (Rm –Rrf)]

Where:

Ra = Expected return on a security

Rrf = Risk-free rate

Ba = Beta of the security

Rm = Expected return of the market

Note: “Risk Premium” = (Rm – Rrf)

The CAPM formula is used for calculating the expected returns of an asset. It

is based on the idea of systematic risk (otherwise known as non-diversifiable

risk) that investors need to be compensated for in the form of a risk premium.

A risk premium is a rate of return greater than the risk-free rate. When

investing, investors desire a higher risk premium when taking on more risky

investments.](https://image.slidesharecdn.com/capitalassetpricingmodelformula-220613070813-d5cdc52c/95/Capital-Asset-Pricing-Model-Formula-3-638.jpg)

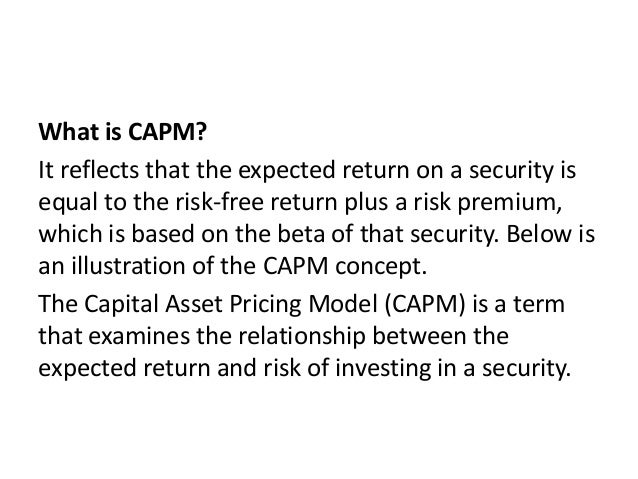

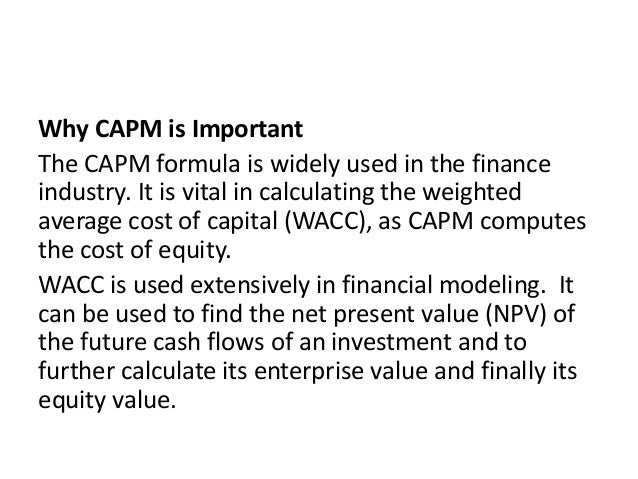

The Capital Asset Pricing Model (CAPM) illustrates the relationship between expected return and risk of a security, calculated using the formula ra = rrf + [ba * (rm – rrf)]. It emphasizes the need for a risk premium, compensating investors for systematic risk, and is crucial in determining the weighted average cost of capital (WACC) in financial modeling. CAPM is essential for evaluating investment returns, net present value, enterprise value, and equity value.