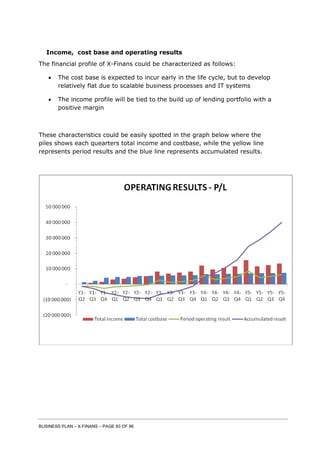

This document provides a business plan for X-Finans, a proposed new financial lending and leasing institution in Norway. The plan outlines X-Finans' vision, products, operations, management team, market analysis, financial projections, and risks. Key points include: X-Finans will focus on car loan and lease products, pursue large dealerships, and use automated processes. The founder has significant experience growing car finance sales. Projected costs are stable while income grows annually, reaching break-even by year 4. The market is dominated by two large players, leaving opportunity for an innovative new competitor.