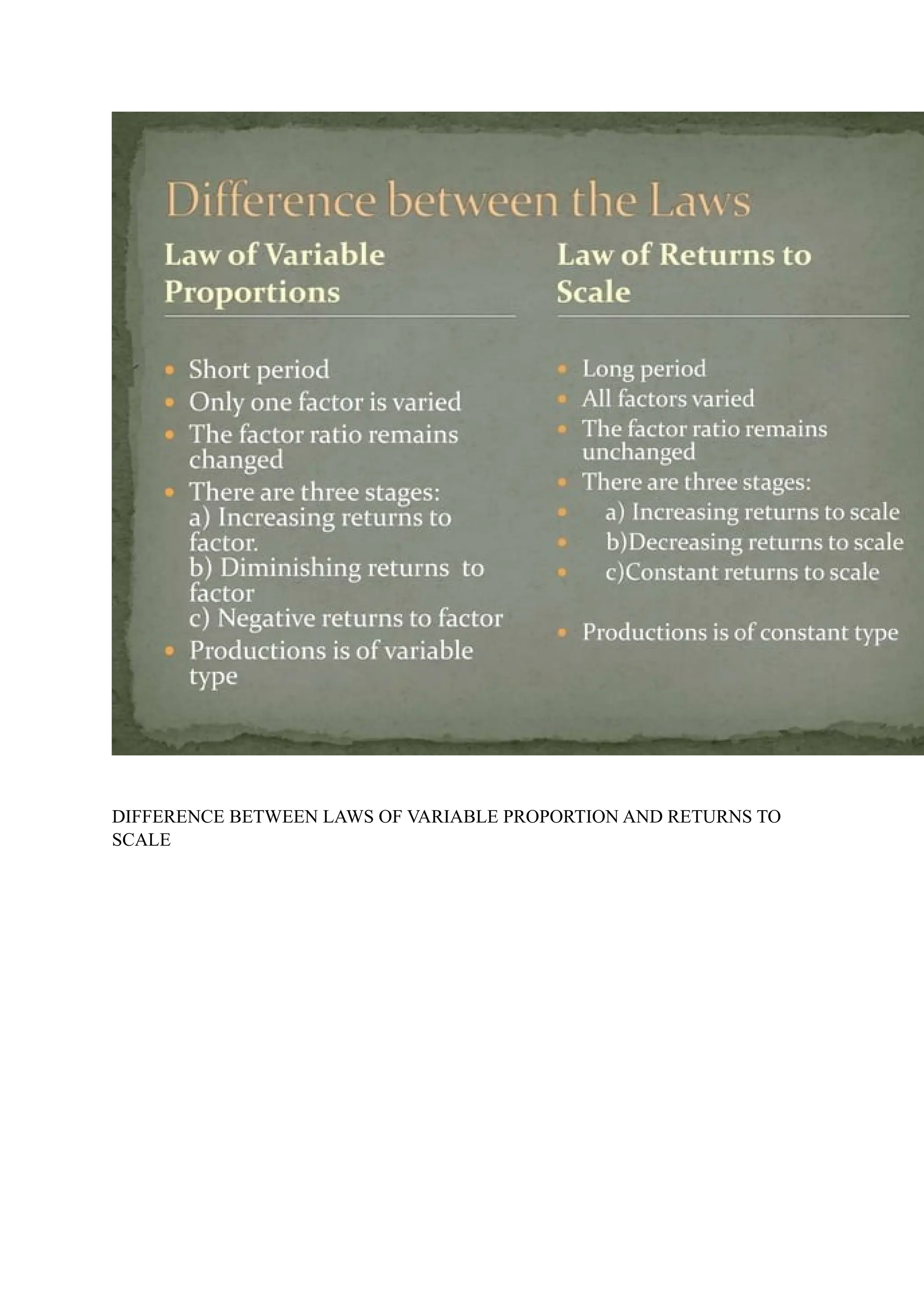

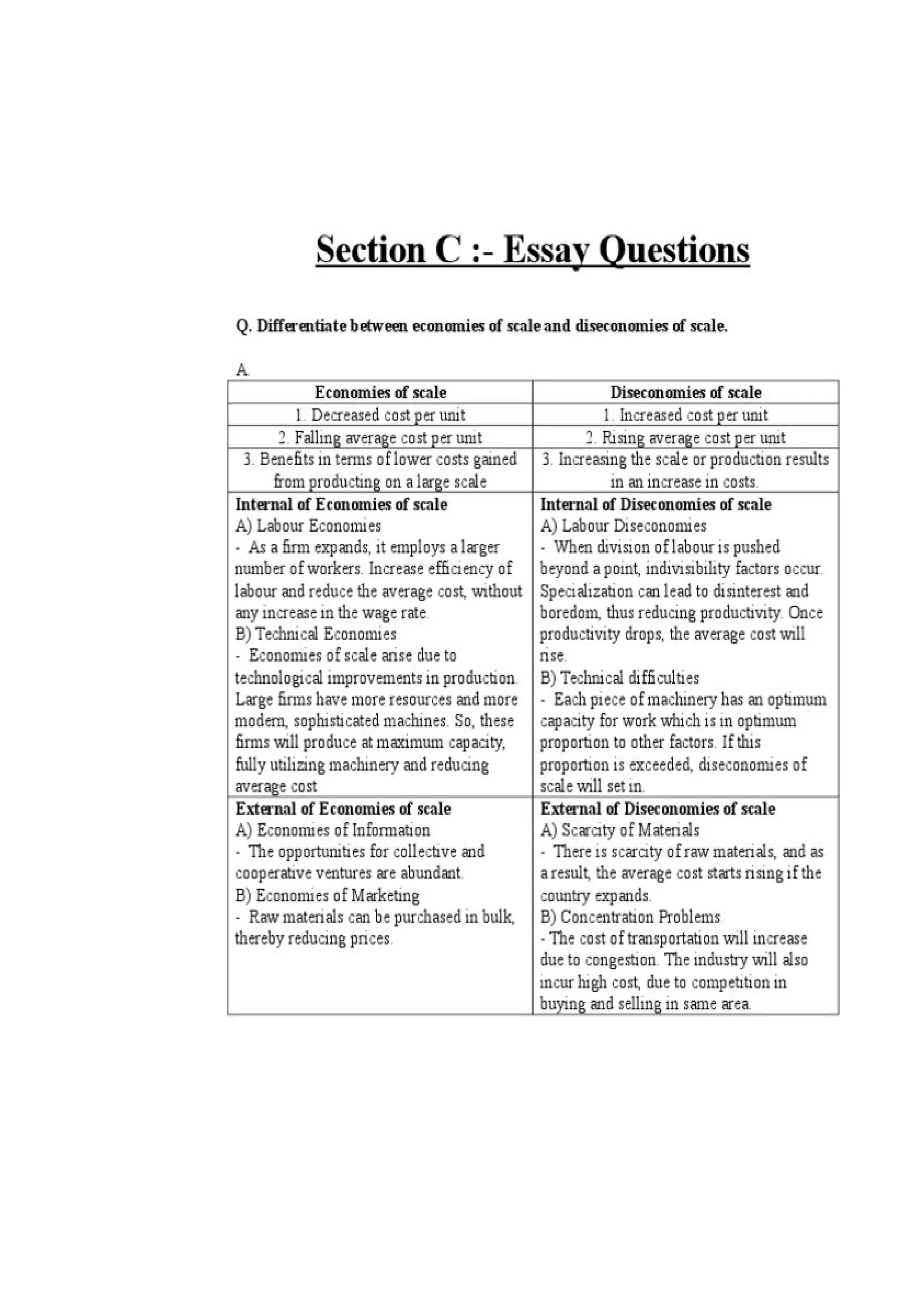

The document discusses the theory of production, emphasizing the concept of production functions, which can be categorized into linear and non-linear forms. It outlines the types of production processes (primary, secondary, and tertiary), the importance of factors of production, and introduces the production function as a mathematical representation that optimally combines inputs. Additionally, it covers concepts such as economies of scale, the law of variable proportions, and the differentiation between short-run and long-run production functions.

![Production function [ management ]](https://cdn.slidesharecdn.com/ss_thumbnails/productionfunctionmanagement-140115104149-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)