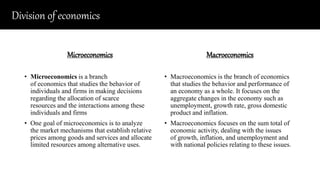

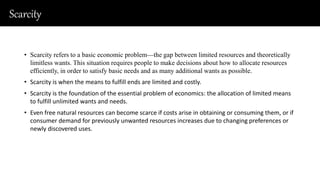

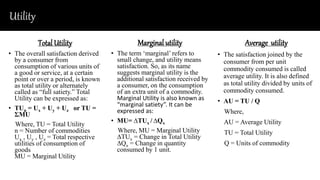

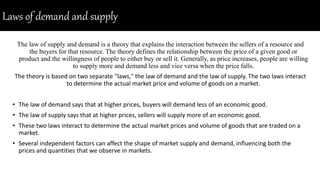

This document provides an overview of basic economic concepts. It discusses that economics is concerned with production, distribution, and consumption of goods and services. It focuses on how individuals, businesses, governments, and nations make choices to allocate scarce resources. Economics can be broken down into microeconomics, which focuses on individual agents, and macroeconomics, which looks at the economy as a whole. Building economics applies general economic principles to the construction industry. The document also introduces concepts like needs and wants, scarcity, utility, and the laws of supply and demand.