Budget project

•

0 likes•3,113 views

This document provides instructions for creating a realistic monthly budget. It explains that a budget accounts for income versus expenses, with the goal of expenses being less than income. Common expenses are listed like housing, utilities, transportation, food, and savings, which should be at least 5% of income. Students will be assigned an occupation with a set income and must choose housing, a car, and estimate other expenses to track in a monthly budget worksheet. If expenses exceed income or savings is less than 5%, spending habits must be adjusted.

Recommended

More Related Content

Similar to Budget project

Similar to Budget project (20)

More from Cinnaminson Public Schools

More from Cinnaminson Public Schools (20)

Recently uploaded

Recently uploaded (20)

Budget project

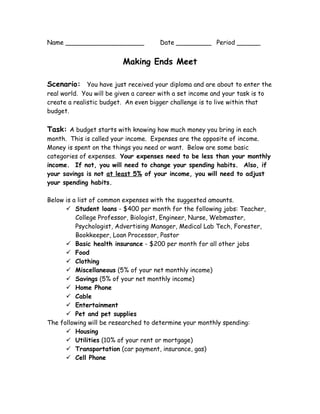

- 1. Name ____________________ Date _________ Period ______ Making Ends Meet Scenario: You have just received your diploma and are about to enter the real world. You will be given a career with a set income and your task is to create a realistic budget. An even bigger challenge is to live within that budget. Task: A budget starts with knowing how much money you bring in each month. This is called your income. Expenses are the opposite of income. Money is spent on the things you need or want. Below are some basic categories of expenses. Your expenses need to be less than your monthly income. If not, you will need to change your spending habits. Also, if your savings is not at least 5% of your income, you will need to adjust your spending habits. Below is a list of common expenses with the suggested amounts. Student loans - $400 per month for the following jobs: Teacher, College Professor, Biologist, Engineer, Nurse, Webmaster, Psychologist, Advertising Manager, Medical Lab Tech, Forester, Bookkeeper, Loan Processor, Pastor Basic health insurance - $200 per month for all other jobs Food Clothing Miscellaneous (5% of your net monthly income) Savings (5% of your net monthly income) Home Phone Cable Entertainment Pet and pet supplies The following will be researched to determine your monthly spending: Housing Utilities (10% of your rent or mortgage) Transportation (car payment, insurance, gas) Cell Phone

- 2. Part One Occupation: You will be assigned an occupation by luck of the draw. Fill in the sections below using the information on the occupation cards given to you by your teacher. Occupation _______________________ Annual Gross Income ___________ Gross Monthly Income ___________ (income divided by 12) Net monthly income ___________ (gross monthly income multiplied by 0.80) *This is your take home pay after taxes.

- 3. Part Two Housing: Choose a housing preference using the information provided. Housing should be no more than 30% of your monthly net income. (0.30 multiplied by net monthly income) How much money can you afford for housing? _______________ Which housing option did you choose? ______________________ What is your housing cost? ____________ What percent is this of your net monthly income? ____________ Utilities are 10% of your monthly housing costs. This includes gas, water, electric, and garbage collection. What is your utility cost? ____________ Type of housing Mortgage payment Rent Apartment X $450 Condo $1,000 $750 Townhome $1,300 $850 House $1,500 $950

- 4. Part Three Transportation: Use the car magazines provided to choose a car you would consider owning. You will have no money available for a down payment. Car Monthly Payment (5 years at 3.0% APR) Total cost for Transportation Gas + Insurance + Payment If you find you cannot afford a car, you may pay $100 per month for use of public transportation. Car Payment Calculation The bank has granted each of you a 5 year loan at a 3.0% interest rate. What is the cost of the car you chose? _____________ To find the cost per month, divide by 60. (Because 5 years x 12 months = 60) + + Now find the cost including interest: Multiply the monthly payment by 0.03. = Add the monthly car payment and the interest together. What is your total monthly car payment? You must also add the cost of basic car insurance ($100) and the cost of gas ($20-100) $100 + _________ + __________ = $ ____________ (insurance) (gas) (car payment) TOTAL TRANSPORTATION COST

- 5. Part Four Flexible Estimated Expenses: Determine on your own the possible monthly cost of the following items. Category Monthly Cost Food Clothing Home Phone Cable & Internet Entertainment (movies, restaurants, events) Pet and Pet Supplies Miscellaneous (2%) *Cell Phone *Research the provided cell phone plans to determine which plan best fits your budget and meets your needs. Total Estimated Expenses ___________________

- 6. Part Five Data Entry: During class enter the information you have collected about your monthly expenses into the “Monthly Budget Record” (from student loan down to savings). Make adjustments to your spending if necessary in order to meet project goals. * Save 5% of your income * Don’t spend more than you earn Part Six Make a Circle Graph: Use the data from your Excel worksheet to make a circle graph. (Directions will be on zmath.edublogs.org). We will use an online website to help us build our graphs

- 7. MONTHLY BUDGET RECORD OCCUPATION: ______________________ INCOME EXPENSES PERCENT OF INCOME NET MONTHLY INCOME X X CLOTHING X HOUSING X UTILITIES X TRANSPORTATION X ENTERTAINMENT X MISCELLANEOUS X FOOD X PHONE X CELL PHONE X STUDENT LAON X HEALTH INSURANCE X PETS X CABLE X TOTAL X My 5% goal to save ______________ ACTUAL SAVINGS ______________ = ________% (Total income minus total expenses)