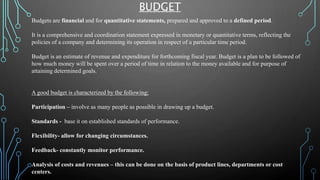

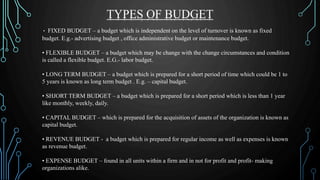

Budgets are financial plans that quantify expected revenue and expenses over a defined period of time. They reflect a company's policies and allow it to determine operations for a particular time period. A good budget involves participation from many people, is based on established standards, allows flexibility, and provides constant monitoring and analysis of costs and revenues. There are different types of budgets including fixed, flexible, long-term, short-term, capital, revenue, expense, cash, operating, and zero-based budgets.

![[rokonz.com] Glossary of Semantic SEO Part-1.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rokonz-260123200456-440e4060-thumbnail.jpg?width=640&height=640&fit=bounds)