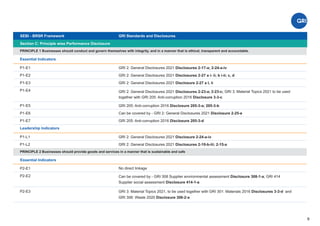

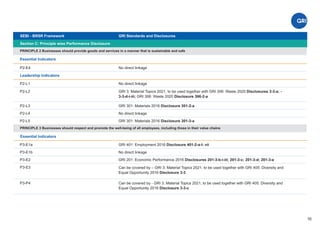

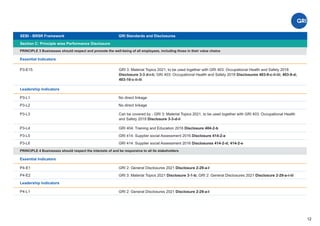

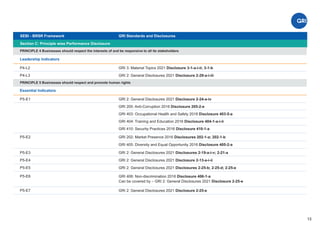

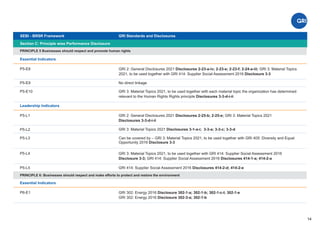

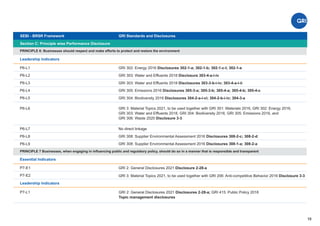

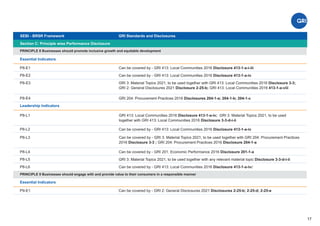

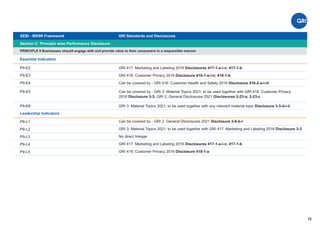

Download as PDF, PPTX

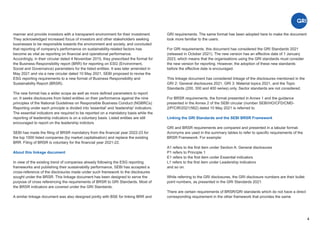

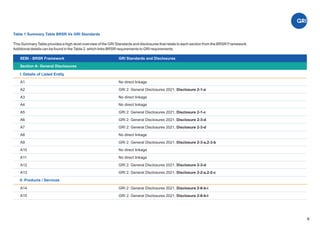

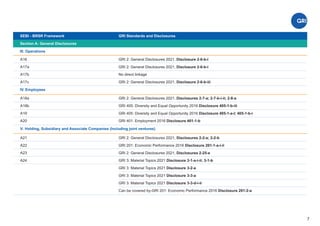

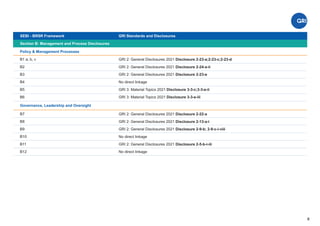

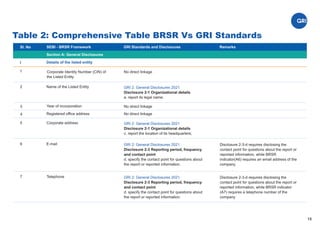

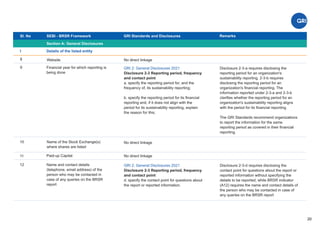

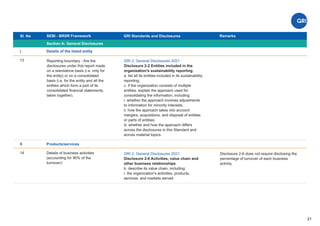

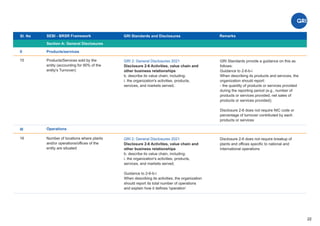

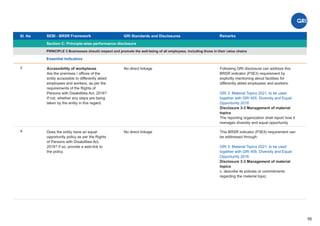

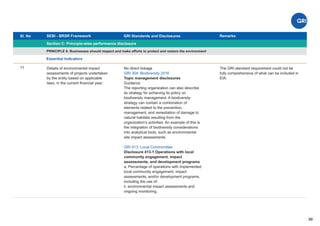

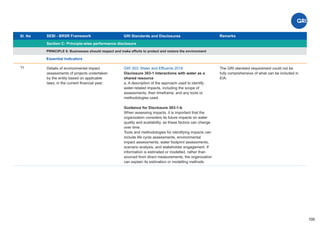

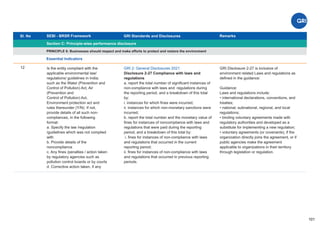

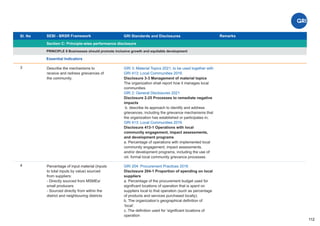

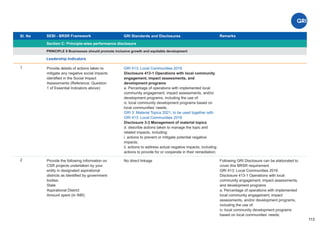

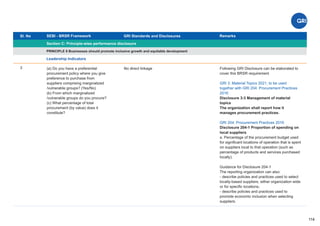

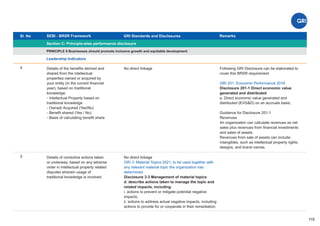

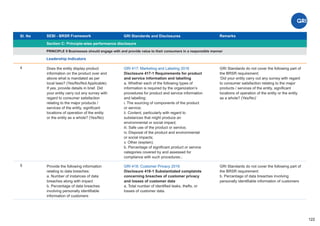

The document provides a linkage between the requirements of the Business Responsibility and Sustainability Report (BRSR) framework introduced by the Securities and Exchange Board of India (SEBI) and the Global Reporting Initiative (GRI) Standards. It compares each disclosure requirement of the BRSR with relevant disclosures from the GRI Standards and presents them in tabular format for ease of reference. The purpose is to help companies comply with BRSR requirements by cross-referencing disclosures already made under the GRI Standards. The summary table lists each section of the BRSR and maps them to the applicable GRI disclosures at a high level, while the comprehensive table provides more details on the specific linkages.