WHAT IS BLOCKCHAINTECHNOLOGY?

Blockchain technology is a decentralized , distributed ledger system

that records transactions across multiple computers in a way that

ensures security, transparency and immutability . Each transactions is

grouped into a block , which is linked to the previous one , forming a

continuous chain . This structure prevents tampering and allows for

trustless , peer-to-peer interactions without the need of central

authority

4.

FUNDAMENTALS OF BLOCKCHAIN

1.Public Distributed Ledgers:

A block chain is a decentralized public distributed ledger that is used to record transactions

across many computers.

A distributed ledger is a database that is shared among the users of the blockchain network

The transactions are accessed and verified by users associated with the bitcoin

network ,thereby making it less prone to cyber attack

2 . Encryption:

Blockchain eliminates unauthorized access by using the cryptographic algorithm to ensure the

blocks are kept secure

Each user in block has their key

5.

3. Proof OfWork:

Proof of work (PoW) is a method to validate transactions in a blockchain network by solving a

complex mathematical puzzle called mining

Note: users trying to solve the puzzle is called miners

4. Mining:

In blockchain, miners use their resources (time , money, elelctricity , etc) to validate a new

transaction and record them on the public ledger , they are given a reward

Note: As reward , the miner gets 12.5 BTC(bitcoins)

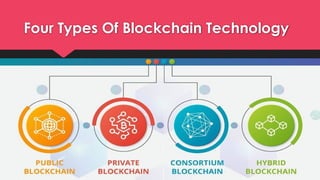

1. Public Blockchain:

Theseblockchain are completely open to following the idea of decentralization. They are non-

restrictive, anyone having a computer and internet can participate in the network

2. Private Blockchain:

These blockchains are not as decentralized as the public block chains only selected

nodes can participate in the process, making it more secure than others

3. Consortium Blockchain:

It is a creative approach that solves the need of an organization. This blockchain

validates the transactions or receives transactions It is also known as federated blockchain

4. Hybrid Blockchain:

It is the mixed content of private and public blockchain , where some part is controlled

by some organization and other makes are made visible as public blockchain

9.

How Does BlockchainWorks?

Blockchain technology works by recording transactions, creating blocks, and linking them together to

form a chain:

1.Record the transaction: An authorized participant inputs a transaction, which is authenticated by the

technology.

2.Create a block: The transaction is represented in a block, which is sent to every computer node in the

network.

3.Validate the transaction: Authorized nodes validate the transaction and add the block to the

blockchain.

4.Update the network: The update is distributed across the network, finalizing the transaction.

5.Link the blocks: Each block includes a digital summary of all the transactions in that block and all

previous transactions. This digital summary connects the blocks together in a chain.

6.Share the ledger: The ledger is shared among all the nodes.

Blockchain uses cryptographic hashing to ensure the security of each block. This method converts transaction

data into a unique hexadecimal transaction ID hash, which acts as a digital fingerprint.

Blockchain is used in many industries, including real estate, where it can revolutionize property transactions

and ownership records.

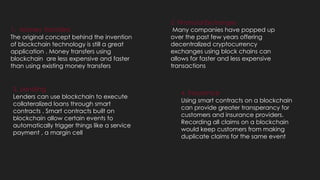

1. Money transfers

Theoriginal concept behind the invention

of blockchain technology is still a great

application . Money transfers using

blockchain are less expensive and faster

than using existing money transfers

2. Financial Exchanges

Many companies have popped up

over the past few years offering

decentralized cryptocurrency

exchanges using block chains can

allows for faster and less expensive

transactions

3. Lending

Lenders can use blockchain to execute

collateralized loans through smart

contracts . Smart contracts built on

blockchain allow certain events to

automatically trigger things like a service

payment , a margin cell

4. Insurance

Using smart contracts on a blockchain

can provide greater transperancy for

customers and insurance providers.

Recording all claims on a blockchain

would keep customers from making

duplicate claims for the same event

12.

5. Secure PersonalInformation

Blockchain technology can be used for

secure access to identifying information

while improving access for those who

need it in industries such as travel, health

care , finance, and education

6. Voting

If personal identity information held on a

blockchain, from also being able to vote.

Using blockchain technology can make

sure that nobody votes twice

7. Real Estate

Using blockchain technology to record

real estate transactions can provide a

more secure and accessible means of

verifying and transferring ownership.

That can speed up transactions ,reduce

paper work and save money

8. Health care

Keeping medical records on a blockchain

can allow doctors and medical professional

to obtain accurate and up-to-date

information on their patients . That can

ensure that patients seeing multiple doctors

get the best care possible

13.

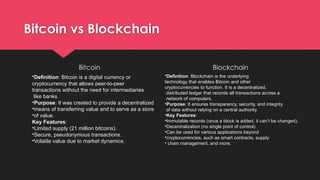

Bitcoin vs Blockchain

BitcoinBlockchain

•Definition: Bitcoin is a digital currency or

cryptocurrency that allows peer-to-peer

transactions without the need for intermediaries

like banks.

•Purpose: It was created to provide a decentralized

•means of transferring value and to serve as a store

•of value.

Key Features:

•Limited supply (21 million bitcoins).

•Secure, pseudonymous transactions.

•Volatile value due to market dynamics.

•Definition: Blockchain is the underlying

technology that enables Bitcoin and other

cryptocurrencies to function. It is a decentralized,

distributed ledger that records all transactions across a

network of computers.

•Purpose: It ensures transparency, security, and integrity

of data without relying on a central authority.

•Key Features:

•Immutable records (once a block is added, it can’t be changed).

•Decentralization (no single point of control).

•Can be used for various applications beyond

•cryptocurrencies, such as smart contracts, supply

• chain management, and more.

14.

Advantages Of Blockchain

1.Decentralization

Reducesreliance on a single authority, which minimizes the risk of corruption or failure.

• Distributes data across a network of nodes, enhancing resilience.

2. Transparency

• Transactions are recorded on a public ledger, making them visible to all participants.

• Enhances trust among users, as data can be independently verified.

3. Security

• Cryptographic techniques secure the data, making it difficult to alter past records.

• Each block is linked to the previous one, creating a secure chain that is hard to tamper with.

4. Immutability

• Once a transaction is recorded on the blockchain, it cannot be changed or deleted.

• This ensures a reliable and permanent record of all transactions.

15.

o 5. Traceability

oTransactions can be traced back through the blockchain, making it easier to audit

and verify.

o Particularly useful in supply chains to track the origin and journey of products.

o 6. Efficiency

o Reduces the need for intermediaries (like banks), streamlining processes and reducing

costs.

o Automated smart contracts can execute transactions instantly once conditions are

met.

o 7. Cost-Effectiveness

o Reduces costs associated with intermediaries, fraud, and manual processes.

o Lowers transaction fees, especially in cross-border payments.

8. Data Integrity

•Protects data from unauthorized access and ensures that it remains accurate and

reliable.

16.

Disadvantages Of Blockchain

1. Scalability Issues

• Many blockchains struggle to process large volumes of transactions quickly.

• As the network grows, the time and resources required to validate transactions can increase significantly.

2. Energy Consumption

• Some consensus mechanisms (like Proof of Work) require significant computational power, leading to high energy consumption.

• This raises environmental concerns, particularly with large-scale mining operations.

3. Complexity

• Understanding blockchain technology can be challenging for non-technical users.

• Implementing and maintaining blockchain systems may require specialized knowledge and skills.

4. Regulatory Uncertainty

• Many countries have unclear regulations regarding cryptocurrencies and blockchain technology.

• This uncertainty can hinder adoption and lead to legal complications.

17.

FUTURE OF BLOCKCHAIN

The future of blockchain technology holds significant promise across various sectors. Here are some key

trends and potential developments:

1.Decentralized Finance (DeFi): DeFi platforms are likely to continue growing, offering users greater access to

financial services without traditional intermediaries.

2.Tokenization of Assets: Real-world assets, like real estate and art, may become tokenized, making

transactions more accessible and liquid.

3. Interoperability: Improved interoperability between different blockchain networks could facilitate more

seamless transactions and data sharing.

4. Supply Chain Transparency: Blockchain can enhance traceability and transparency in supply chains,

helping to combat fraud and improve accountability.

18.

5.Identity Verification: Decentralizedidentity solutions may become more common, allowing

individuals to control their own identity data securely.

6.Regulatory Developments: As blockchain technology matures, we can expect clearer

regulatory frameworks that address compliance while fostering innovation.

7.Sustainability Initiatives: There may be a push for greener blockchain solutions that focus on

reducing energy consumption, particularly in mining operations.

8.Integration with IoT: Blockchain can enhance the security and efficiency of IoT devices,

enabling smarter and more secure networks.

19.

Conclusion

In conclusion, blockchaintechnology stands as a transformative force across various sectors, offering

enhanced security, transparency, and efficiency. Its decentralized nature fosters trust and reduces the

need for intermediaries, making it particularly valuable in industries like finance, supply chain, and

healthcare. However, challenges such as scalability, regulatory concerns, and energy consumption

must be addressed to fully realize its potential. As research and development continue, blockchain

could reshape not only business models but also the fundamental way we interact and transact in the

digital age, paving the way for a more secure and equitable future.